LEARNING TO TRUST A TRADING SYSTEM

One of the most difficult decisions to make when running a systematic trading program is  knowing when to override the system. During the early 2000’s when I was running the Caissa Capital fund, the models would regularly make predictions on volatility that I and our head Trader, Ron Henley, a former option trader from the AMEX, disagreed with. Most times, the system proved to have made the correct decision. My take-away from that experience was that, as human beings, even as traders, we are not very good at pricing risk.

knowing when to override the system. During the early 2000’s when I was running the Caissa Capital fund, the models would regularly make predictions on volatility that I and our head Trader, Ron Henley, a former option trader from the AMEX, disagreed with. Most times, the system proved to have made the correct decision. My take-away from that experience was that, as human beings, even as traders, we are not very good at pricing risk.

My second take-away was that, by and large, you are better off trusting the system, rather than second-guessing its every decision. Of course, markets can change and systems break down; but the right approach to assessing this possibility is to use statistical control procedures to determine formally whether or not the system has broken down, rather than going through a routine period of under-performance (see: is your strategy still working?)

GREEK LESSONS

So when the Greek crisis blew up in June my first instinct was not to start looking  immediately for the escape hatch. However, as time wore on I became increasingly concerned that the risk of a Grexit or default had not abated. Moreover, I realized that there was really nothing comparable in the data used in the development of the trading models that was in any way comparable to the scenario facing Greece, the EU and, by a process of contagion, US markets. Very reluctantly, therefore, I came to the decision that the smart way to play the crises was from the sidelines. So we made the decisions to go 100% to cash and waited for the crisis to subside.

immediately for the escape hatch. However, as time wore on I became increasingly concerned that the risk of a Grexit or default had not abated. Moreover, I realized that there was really nothing comparable in the data used in the development of the trading models that was in any way comparable to the scenario facing Greece, the EU and, by a process of contagion, US markets. Very reluctantly, therefore, I came to the decision that the smart way to play the crises was from the sidelines. So we made the decisions to go 100% to cash and waited for the crisis to subside.

A week went by. Then another. Of course, I had written to our investors explaining what we intended to do, and why, so there were no surprises. Nonetheless, I felt uncomfortable not making money for them. I did my best to console myself with the principal rule of money management: first, do not lose money. Of course we didn’t – but neither did we make much money, and ended June more or less flat.

COMEBACK

After the worst of the crisis was behind us, I was relieved to see that the models appeared almost as anxious as I was to make up for lost time. One of the features of the system is

that it makes aggressive use of leverage. Rather like an expert poker player, when it judges the odds to be in its favor, the system will increase its bet size considerably; at other times it will hunker down, play conservatively, or even exit altogether. Consequently, the turnover in the portfolio can be large at times. The cost of trading high volume can substantial, especially in some of the less liquid ETF products, where the bid/ask spread can amount to several cents. So we typically aim to execute passively, looking to buy on the bid and sell on the offer, using execution algos to split our orders up and randomize them. That also makes it tougher for HFT algos to pick us off as we move into and out of our positions.

that it makes aggressive use of leverage. Rather like an expert poker player, when it judges the odds to be in its favor, the system will increase its bet size considerably; at other times it will hunker down, play conservatively, or even exit altogether. Consequently, the turnover in the portfolio can be large at times. The cost of trading high volume can substantial, especially in some of the less liquid ETF products, where the bid/ask spread can amount to several cents. So we typically aim to execute passively, looking to buy on the bid and sell on the offer, using execution algos to split our orders up and randomize them. That also makes it tougher for HFT algos to pick us off as we move into and out of our positions.

So, in July, our Greek “vacation” at an end, the system came roaring back, all guns blazing. It quickly moved into some aggressive short volatility positions to take advantage of the elevated levels in the VIX, before reversing and gong long as the index collapsed to the bottom of the monthly range.

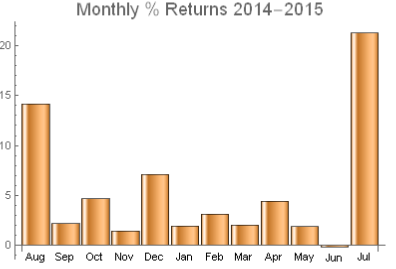

A DOUBLE-DIGIT MONTHLY RETURN: +21.28%

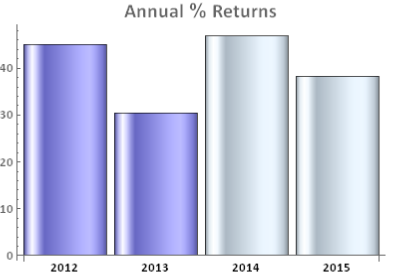

The results were rather spectacular: a return of +21.28% for the month, bringing the total return to 38.25% for 2015 YTD.

return to 38.25% for 2015 YTD.

In the current low rate environment, this rate of return is extraordinary, but not entirely unprecedented: the strategy has produced double-digit monthly returns several times in the past, most recently in August last year, which saw a return of +14.1%. Prior, to that, the record had been +8.90% in April 2013.

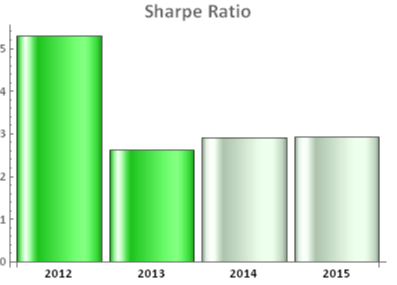

Such outsized returns come at a price – they have the effect of increasing strategy volatility and hence reducing the Sharpe Ratio. Of course, investors worry far less about upside volatility than downside volatility (or simi-variance), which is why the Sortino Ratio is in some ways a more appropriate measure of risk-adjusted performance, especially for strategies like ours which has very large kurtosis.

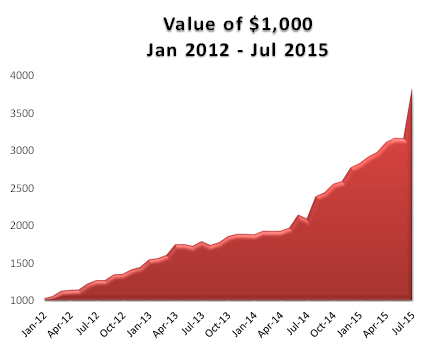

Since inception the compound annual growth rate (CAGR) of the strategy has been 45.60%, while the Sharpe Ratio has maintained a level of around 3 since that time.

Since inception the compound annual growth rate (CAGR) of the strategy has been 45.60%, while the Sharpe Ratio has maintained a level of around 3 since that time.

Most of the drawdowns we have seen in the strategy have been in single digits, both in back-test and in live trading. The only exception was in 2013, where we experienced a very short term decline of -13.40%, from which the strategy recovered with a couple of days.

In the great majority of cases, drawdowns in VIX-related strategies result from bad end-of-day “marks” in the VIX index. These can arise for legitimate reasons, but are often

caused by traders manipulating the index, especially around option expiration. Because of the methodology used to compute the VIX, it is very easy to move the index by 5bp to 10bp, or more, by quoting prices for deep OTM put options as expiration nears. This can be critically important to holders of large VIX option positions and hence the temptation to engage in such manipulation may be irresistible.

caused by traders manipulating the index, especially around option expiration. Because of the methodology used to compute the VIX, it is very easy to move the index by 5bp to 10bp, or more, by quoting prices for deep OTM put options as expiration nears. This can be critically important to holders of large VIX option positions and hence the temptation to engage in such manipulation may be irresistible.

For us, such market machinations are simply an annoyance, a cost of doing business in the VIX. Sure, they inflate drawdowns and strategy volatility, but there is not much we can do about them, other wait patiently for bad “marks” to be corrected the following day, which they almost always are.

Looking ahead over the remainder of the year, we are optimistic about the strategy’s opportunities to make money in August, but, like many traders, we are apprehensive about  the consequences if the Fed should decide to take action to raise rates in September. We are likely to want to take in smaller size through the ensuing volatility, since either a long- or short-vol positions carries considerable risk in such a situation. As and when a rate rise does occur, we anticipate a market correction of perhaps 20% or more, accompanied by surge in market volatility. We are likely to see the VIX index reach the 20’s or 30’s, before it subsides. However, under this scenario, opportunities to make money on the short side will likely prove highly attractive going into the final quarter of the year. We remain hopeful of achieving a total return in the region of 40% to 50%, or more in 2015.

the consequences if the Fed should decide to take action to raise rates in September. We are likely to want to take in smaller size through the ensuing volatility, since either a long- or short-vol positions carries considerable risk in such a situation. As and when a rate rise does occur, we anticipate a market correction of perhaps 20% or more, accompanied by surge in market volatility. We are likely to see the VIX index reach the 20’s or 30’s, before it subsides. However, under this scenario, opportunities to make money on the short side will likely prove highly attractive going into the final quarter of the year. We remain hopeful of achieving a total return in the region of 40% to 50%, or more in 2015.

STRATEGY PERFORMANCE REPORT Jan 2012 – Jul 2015