For many decades the principles of portfolio construction laid out by Harry Markovitz in the 1950s have been broadly accepted as one of the cornerstones of modern portfolio theory (as summarized, for example, in this Wikipedia article). The strengths and weakness of the mean-variance methodology are now widely understood and broadly accepted. But alternatives exist, one of which is the strategy portfolio approach to portfolio construction.

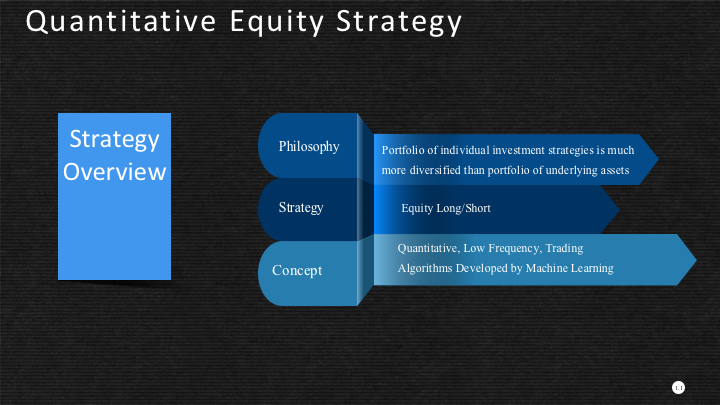

The essence of the strategy portfolio approach lies in the understanding that it is much easier to create a diversified portfolio of equity strategies than a diversified portfolio of the underlying assets. In principle, it is quite feasible to create a basket of strategies for highly correlated stocks that are uncorrelated, or even negatively correlated with one another. For example, one could combine a mean-reversion strategy on a stock like Merck & Co. (MRK) with a momentum strategy on a correlated stock such as Pfizer (PFE), that will typically counteract one another rather than moving in lockstep as the underlying equities tend to do.

In fact this approach is widely employed by hedge fund investors as well as proprietary trading firms and family offices, who seek to diversify their investments across a broad range of underlying strategies in many different asset classes, rather than by investing in the underlying assets directly.

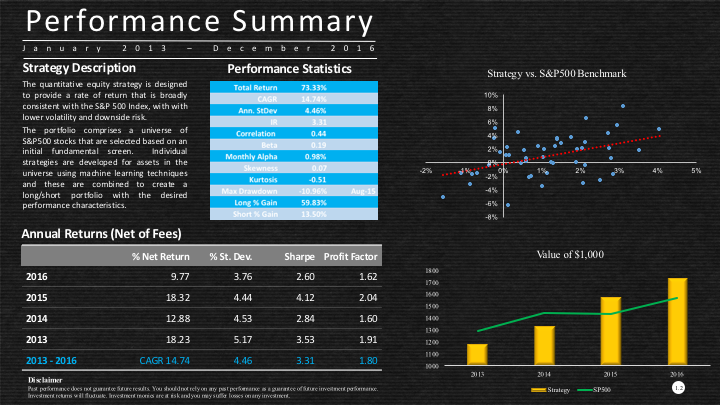

What is to be gained from such an approach to portfolio construction, compared to the typical methodology? The answer is straightforward: lower risk, which results from the lower correlation between strategies, compared to the correlation between the assets themselves. That in turn produces a more diversified portfolio, reducing strategy beta, volatility and tail risk. We see all of these characteristics in the Systematic Strategies Quantitative Equity Strategy, described below, which has an average beta of only 0.2 and a maximum realized drawdown of -2.08%.

Risk reduction is only part of the story, however. The Quantitative Equity Strategy has also yielded a combined alpha in excess of 4% per annum, outperforming the benchmark by a total of 16.35% (net of fees) since 2013. In other words, the individual equity strategies produce alphas that are conserved when combined together to create the overall portfolio. But even if the strategies produced little or no alpha, the risk-reduction benefits of the approach would likely still apply.

What are the drawbacks to this approach to portfolio construction? One major challenge is that it is much harder to create strategy portfolios than asset portfolios. The analyst is obliged to create (at least) one individual strategy for each asset in the universe, rather than a single strategy for the portfolio as a whole. This constrains the rate at which the investment universe can grow (it takes time to research and develop good strategies!), limiting the rate of growth of assets under management. So it is not an approach that I would necessarily recommend if your goal is to deploy multiple billions of dollars; but AUM up to around a billion dollars is certainly a feasible target.

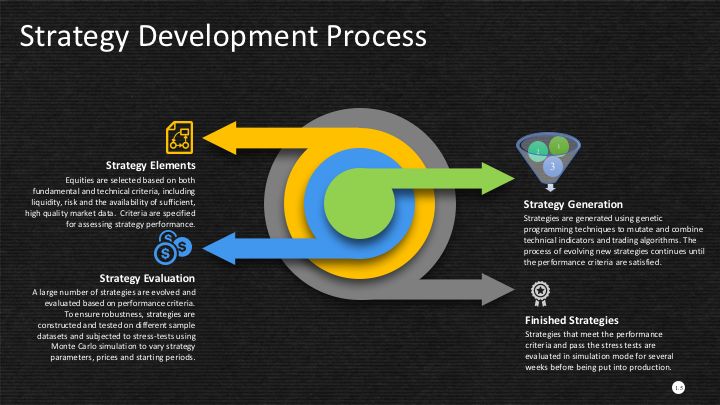

From a risk perspective, the chief limitation is that we lack the ability to control the makeup of the resulting portfolio as closely as we can with traditional approaches to portfolio construction. In a typical equity long/short strategy the portfolio is constrained to have a specified maximum beta, and overall net exposure. With the strategy portfolio approach we are unable to guarantee a specific limit on the net exposure, or the beta of the portfolio. We may be able to quantify that, historically, the portfolio has an average net long exposure, of, say, 25% and an average beta of 0.2; but there is nothing to guarantee that a situation may not arise in future in which all of the strategies align to produce a 100% net long or net short exposure and a beta of +1/-1, or greater. This is extremely unlikely, of course, and may never happen even in geological timescales, as can be demonstrated by Monte Carlo simulation. What is likely, however, is that there will be periods in which the beta and net exposure of the portfolio may fluctuate widely.

Is this a problem? Yes and no. The point about constraining the portfolio beta and net exposure in a typical long/short strategy is to manage portfolio risk. Such constraints decrease the likelihood of substantial losses – but they cannot guarantee that outcome, as has been demonstrated during prior periods of severe market stress such as 2000/01 and 2008/09. Asset correlations tend to increase significantly when markets suffer major declines, often undermining the assumptions on which the portfolio and its associated risk limits were originally based.

Similarly, the way in which we construct strategy portfolios takes a statistical approach to risk control, using stochastic process control. Just as with the traditional approach to portfolio construction, statistical analysis cannot guarantee that market conditions may not arise that give rise to substantial losses, however unlikely such circumstances may be.

Read more about stochastic process control:

http://jonathankinlay.com/2015/04/strategy-still-working/

More on genetic programming:

http://jonathankinlay.com/2014/06/a-primer-on-genetic-programming/

Is the risk of as yet unknown future market conditions greater for strategy portfolios greater than for traditional equity long/short portfolios? I would say not. In fact, during periods of market stress I would prefer to be in a portfolio of strategies, some of which at least are likely to perform well, rather than in a portfolio of equities which are now all likely to be highly correlated to the benchmark index.

The benefit of being able to check the boxes for risk controls such as limits on portfolio beta and net exposure is, I would argue, somewhat illusory. They might be characterized as just a placebo for those who are, literally, unable (or, more likely, not paid to) to think outside the box.

But if this argument is not sufficiently persuasive, it is perfectly feasible to overlay risk controls on a portfolio comprising several underlying strategies. For example one can:

- Hedge out portfolio beta and net exposure above a specified level, using index ETFs, futures or options

- Reduce the capital allocations during periods of market stress, or when portfolio beta or market exposure exceeds a threshold level

- Turn off strategies that under-performing in current market conditions

All of these measures will impact strategy performance. By and large, our preference is to let the strategy play out as it may, trusting in the robustness of the strategy portfolio to produce an acceptable outcome. We leave it to the investor to decide what additional risk controls he wishes to implement, either independently, or within a separately managed account.

The Systematic Strategies Quantitative Equity Strategy

Systematic Strategies started out in 2009 as a proprietary trading firm engaged in high frequency trading. In 2012 the firm expanded into low frequency systematic trading strategies with the launch of our VIX ETF strategy, which was superseded in 2015 by the Systematic Volatility Strategy. The firm began managing external capital in its managed account platform in 2015.

In 2012 we created a research program into quantitative equity strategies using machine learning techniques, earlier versions of which were successfully employed in Proteom Capital, a hedge fund that pioneered the approach in the early 2000’s. Proteom managed capital for Paul Tudor Jones’s Tudor Capital and several other major institutional investors until 2007.

Systematic Strategies began trading its Quantitative Equity Strategy, the result of its research program, in 2013. Having built a four year live track record, the firm is opening the strategy to external investors in 2017. The investment program will be offered in managed account format and, for the first time, as a hedge fund product. For more details about the hedge fund offering, please see this post about the Systematic Strategies Fund.

Designed to achieve returns comparable to the benchmark S&P 500 Index, but with much lower risk, the Quantitative Equity Strategy has produced annual returns at a compound rate of 14.74% (net of fees) since 2013, with an annual volatility of 4.46% and realized Sharpe Ratio of 3.31. By contrast, the benchmark S&P 500 Index yielded a compound annual rate of return of 11.93%, with annual volatility of 10.40% and Sharpe Ratio of 1.15. In other words, the strategy has outperformed the benchmark S&P 500 Index by a significant margin, but with much reduced volatility and downside risk.

For more details about the hedge fund offering, please see this post about the Systematic Strategies Fund. If you are an Accredited Investor and wish to receive a copy of the fund offering documents, please write to us at info@systematic-stratgies.com.