Winton Capital Management is a renowned quant fund and one of the world’s largest, most successful CTAs. The firm’s flagship investment strategy, the Winton Diversified Program, follows a systematic investment process that is based on statistical research to invest globally long and short, using leverage, in a diversified range of liquid instruments, including exchange traded futures, forwards, currency forwards traded over the counter, equity securities and derivatives linked to such securities.

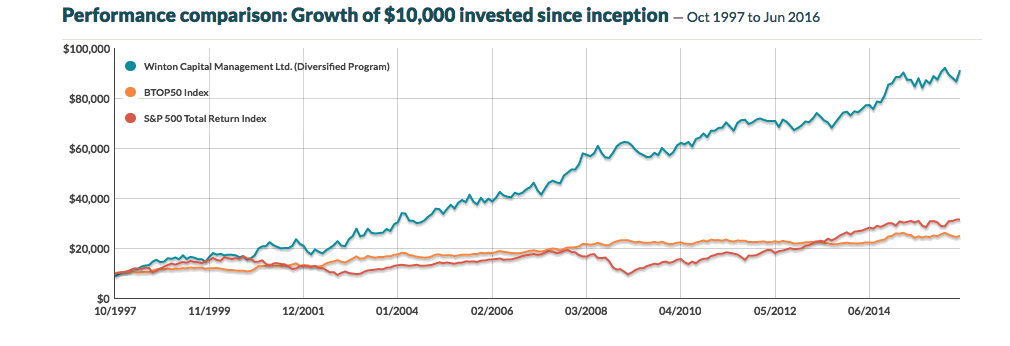

The performance of the program over the last 19 years has been impressive, especially considering its size, which now tops around $13Bn in assets.

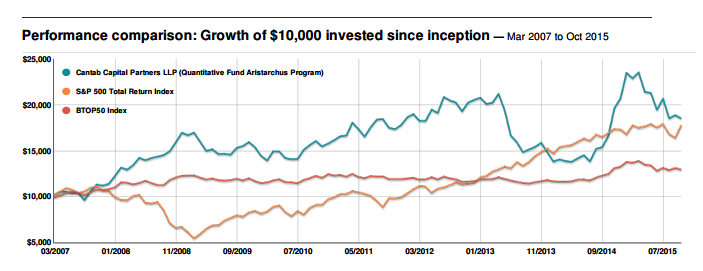

Source: CTA Performance

A Meta-Strategy to Beat Winton Capital

With that background, the idea of improving the exceptional results achieved by David Harding and his army of quants seems rather far fetched, but I will take a shot. In what follows, I am assuming that we are permitted to invest and redeem an investment in the program at no additional cost, other than the stipulated fees. This is, of course, something of a stretch, but we will make that assumption based on the further stipulation that we will make no more than two such trades per year.

The procedure we will follow has been described in various earlier posts – in particular see this post, in which I discuss the process of developing a Meta-Strategy: Improving A Hedge Fund Investment – Cantab Capital’s Quantitative Aristarchus Fund

Using the performance data of the WDP from 1997-2012, we develop a meta-strategy that seeks to time an investment in the program, taking profits after reaching a specified profit target, which is based on the TrueRange, or after holding for a maximum of 8 months. The key part of the strategy code is as follows:

If MarketPosition = 1 then begin

TargPrL = EntryPrice + TargFr * TrueRange;

Sell(“ExTarg-L”) next bar at TargPrL limit;

If Time >= TimeEx or BarsSinceEntry >= NBarEx1 or (BarsSinceEntry >= NBarEx3 and C > EntryPrice)

or (BarsSinceEntry >= NBarEx2 and C < EntryPrice) then

Sell(“ExMark-L”) next bar at market;

end;

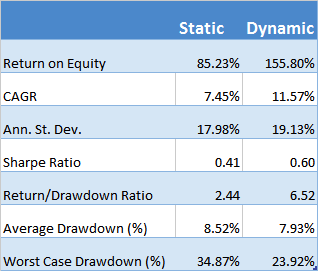

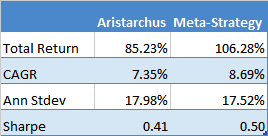

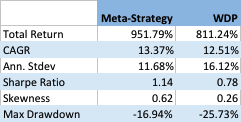

It appears that by timing an investment in the program we can improve the CAGR by around 0.86% per year, and with annual volatility that is lower by around 4.4% annually. As a consequence, the Sharpe ratio of the meta-strategy is considerably higher: 1.14 vs 0.78 for the WDP.

Like most trend-following CTA strategies, Winton’s WDP has positive skewness, an attractive feature that means that the strategy has a preponderance of returns in the positive right tail of the distribution. Also in common with most CTA strategies, on the other hand, the WDP suffers from periodic large drawdowns, in this case amounting to -25.73%.

The meta-strategy improves on the baseline profile of the WDP, increasing the positive skew, while substantially reducing downside risk, leading to a much lower maximum drawdown of -16.94%.

Conclusion

Despite its stellar reputation in the CTA world, investors could theoretically improve on the performance of Winton Capital’s flagship program by using a simple meta-strategy that times entry to and exit from the program using simple technical indicators. The meta-strategy produces higher returns, lower volatility and with higher positive skewness and lower downside risk.