There is a great deal of market lore related to the US presidential elections. It is generally held that elections are good for the market, regardless of whether the incoming president is Democrat or Republican. To examine this thesis, I gathered data on presidential elections since 1950, considering only the first term of each newly elected president. My reason for considering first terms only was twofold: firstly, it might be expected that a new president is likely to exert a greater influence during his initial term in office and secondly, the 2016 contest will likewise see the appointment of a new president (rather than the re-election of a current one).

Market Performance Post Presidential Elections

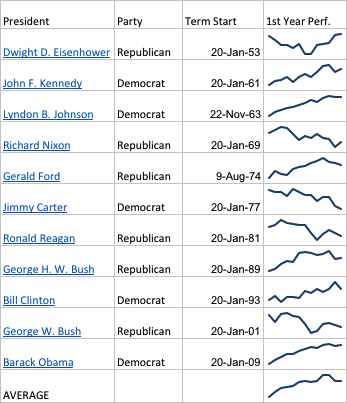

The table below shows the 11 presidential races considered, with sparklines summarizing the cumulative return in the S&P 500 Index in the 12 month period following the start of the presidential term of office. The majority are indeed upward sloping, as is the overall average.

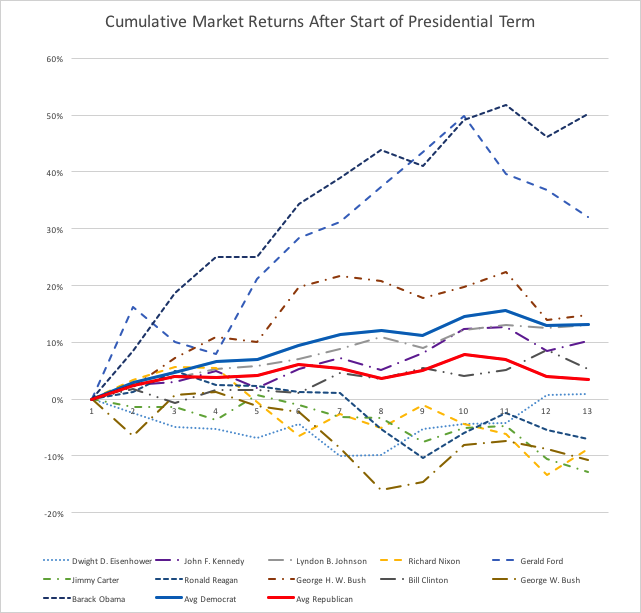

A more detailed picture emerges from the following chart. It transpires that the generally positive “presidential effect” is due overwhelmingly to the stellar performance of the market during the first year of the Gerald Ford and Barack Obama presidencies. In both cases presidential elections coincided with the market nadir following, respectively, the 1973 oil crisis and 2008 financial crisis, after which the economy staged a strong recovery.

Democrat vs. Republican Presidencies

There is a marked difference in the average market performance during the first year of a Democratic presidency vs. a Republican presidency. Doubtless, plausible explanations for this disparity are forthcoming from both political factions. On the Republican side, it could be argued that Democratic presidents have benefitted from the benign policies of their (often) Republican predecessors, while incoming Republican presidents have had to clean up the mess left to them by their Democratic predecessors. Democrats would no doubt argue that the market, taking its customary forward view, tends to react favorably to the prospect of a more enlightened, liberal approach to the presidency (aka more government spending).

Market Performance Around the Start of Presidential Terms

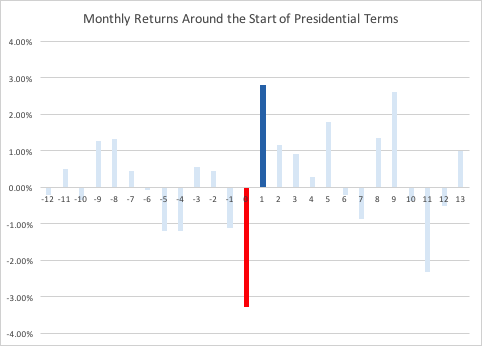

I shall leave such political speculations to those interested in pursuing them and instead focus on matters of a more apolitical nature. Specifically, we will look at the average market returns during the twelve months leading up to the start of a new presidential term, compared to the average returns in the twelve months after the start of the term. The results are as follows:

The twelve months leading up to the start of the presidential term are labelled -12, -11, …, -1, while the following twelve months are labelled 1, 2, … , 12. The start of the term is designated as month zero, while months that fall outside the 24 month period around the start of a presidential term are labelled as month 13.

The key finding stands out clearly from the chart: namely, that market returns during the start month of a new presidential term are distinctly negative, averaging -3.3% , while returns in the first month after the start of the term are distinctly positive, averaging 2.81%.

Assuming that market returns are approximately Normally distributed, a standard t-test rejects the null hypothesis of no difference in the means of the month 0 and month 1 returns, at the 2% confidence level. In other words, the “presidential effect” is both large and statistically significant.

Conclusion: Trading the Election

Given the array of candidates before the electorate this election season, I am strongly inclined to take the trade. The market will certainly “feel the Bern” in the unlikely event that Bernie Sanders is elected president. I can even make an argument for a month 1 recovery, when the market realizes that there are limits to how much economic damage even a Socialist president can do, given constitutional checks and balances, “pen and phone” not withstanding.

Again, an incoming president Trump is likely to be greeted by a sharp market sell-off, based on jittery speculation about the Donald’s proclivity to start a trade war with China, or Mexico, or a ground war with Russia, Iran, or anyone else. Likewise, however, the market will fairly quickly come around to the realization that electioneering rhetoric is unlikely to provide much guidance as to what a president Trump is likely to do in practice.

A Hillary Clinton presidency is likely to be seen, ex-ante, as the most benign for the market, especially given the level of (financial) support she has received from Wall Street. However, there’s a glitch: Bernie is proving much tougher to shake off than she could ever have anticipated. In order to win over his supporters, she is going to have to move out of the center ground, towards the left. Who knows what hostages to fortune a desperate Clinton is likely to have to offer the election gods in her bid to secure the White House?

In terms of the mechanics, while you could take the trade in ETF’s or futures, this is one of those situations ideally suited to options and I am inclined to suggest combining a front-month put spread with a back-month call spread.