Magicicada is the genus of the 13-year and 17-year periodical cicadas of eastern North America. Magicicada species spend most of their 13- and 17-year lives underground feeding on xylem fluids from the roots of deciduous forest trees in the eastern United States. After 13 or 17 years, mature cicada nymphs emerge in the springtime at any given locality, synchronously and in tremendous numbers. Within two months of the original emergence, the lifecycle is complete, the eggs have been laid, and the adult cicadas are gone for another 13 or 17 years.

The emergence period of large prime numbers (13 and 17 years) has been hypothesized to be a predator avoidance strategy adopted to eliminate the possibility of potential predators receiving periodic population boosts by synchronizing their own generations to divisors of the cicada emergence period. If, for example, the cycle length was, say, 12 years, then the species would be exposed to predators regenerating over cycles of 2, 3, 4, or 6 years. Limiting their cycle to a large prime number reduces the variety of predators the species is likely to face.

Prime Cycles in Trading Strategies

What has any of this to do with trading? When building a strategy in a particular market we might start by creating a model that works reasonably well on, say, 5-minute bars. Then, in order to improve the risk-adjusted returns we might try create a second sub-strategy on a different frequency. This will hopefully result in a new series of signals, an increase in the number of trades, and corresponding improvement in the risk-adjusted returns of the overall strategy. This phenomenon is referred to as temporal diversification.

What time frequency should we select for our second sub-strategy? There are many factors to consider, of course, but one of them is that we would like to see as few duplicate signals between the two sub-strategies. Otherwise we will simply be replicating trades, rather than reducing the overall level of strategy risk through temporal diversification. The best way to minimize the overlap in signals generated by multiple sub-strategies is to use prime number bar frequencies (5 minute, 7 minute, 11 minute, etc).

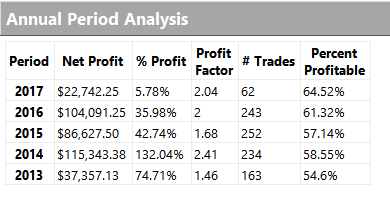

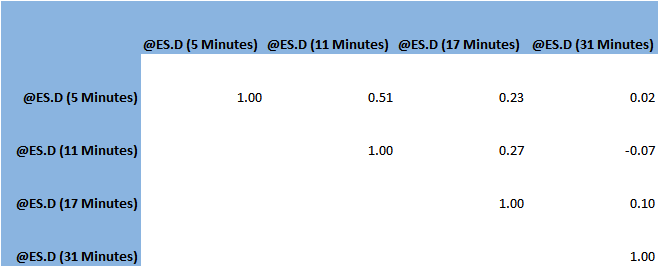

S&P500 Swing Trading Strategy

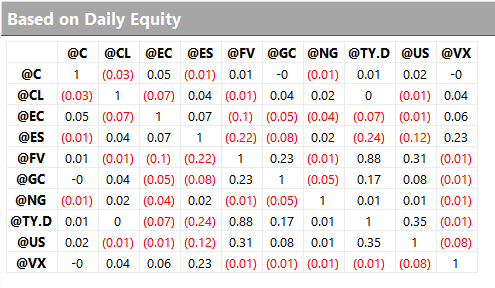

An example of this approach is our EMini Swing Trading strategy which we operate on our Systematic Algotrading Platform. This strategy is actually a combination of several different sub-strategies that operate on 5-minute, 11-minute, 17-minute and 31-minute bars. Each strategy focuses on a different set of characteristics of the S&P 500 futures market, but the key point here is that the trading signals very rarely overlap and indeed several of the sub-strategies have a low correlation.

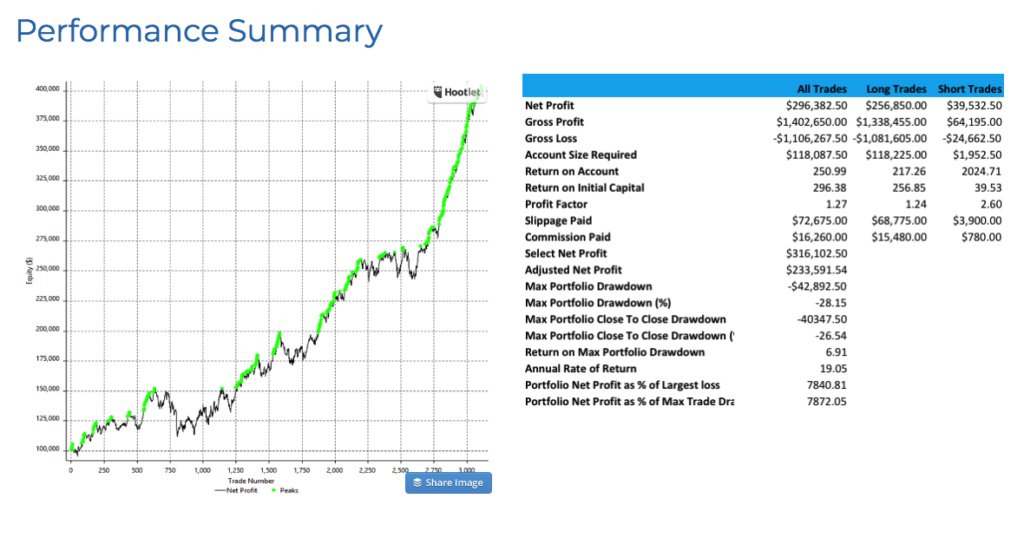

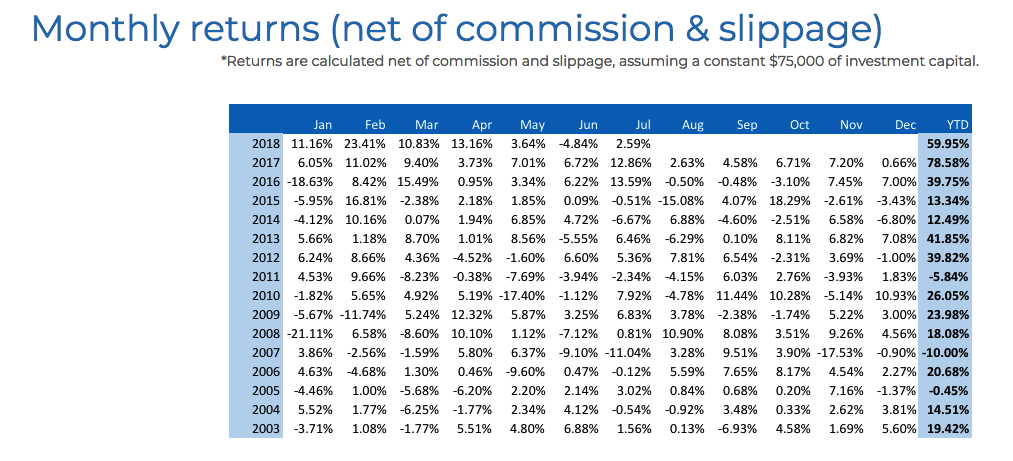

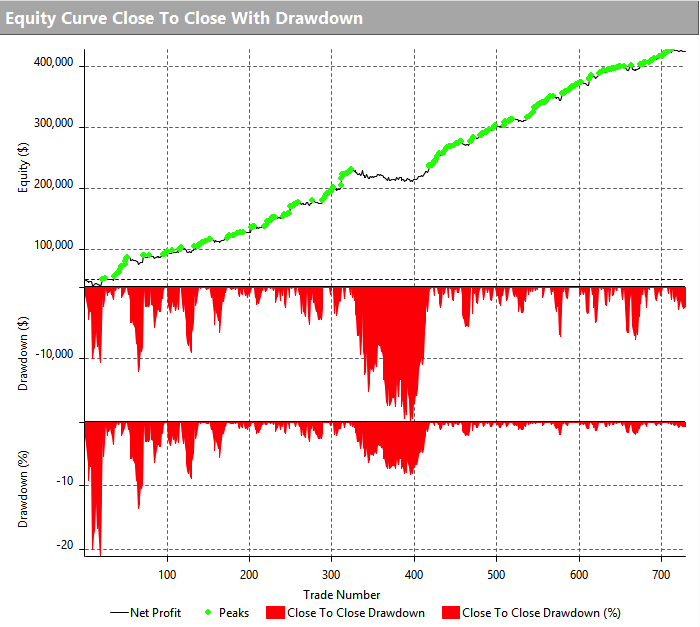

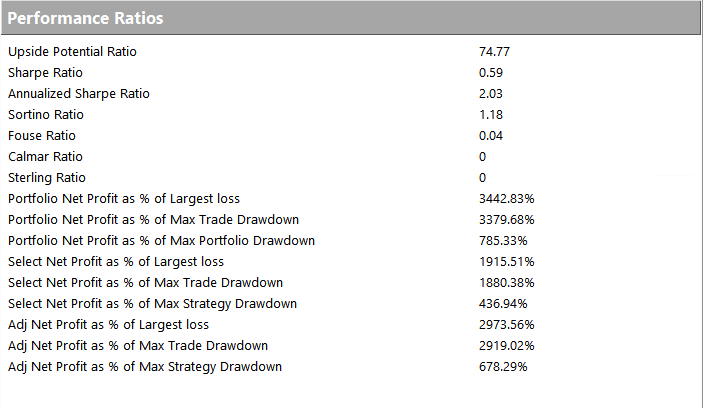

The resulting increase in trade frequency and temporal diversification produces very attractive risk-adjusted performance: after an exceptional year in 2017 which saw a 78.58% net return, the strategy is already at +60% YTD in 2018 and showing no sign of slowing down.

Investors can auto-trade the E-Mini Swing Trading strategy and many other strategies in their own account – see the Leaderboard for more details.