Summary

In this article, I will apply market timing techniques to several popular mutual funds.

The market timing approach produces annual rates of return that are 3% to 7% higher, with lower risk, than an equivalent buy and hold mutual fund investment.

Investors could in some cases have earned more than double the return achieved by holding a mutual fund investment over a 10-year period.

Hedging strategies that use market timing signals are able to sidestep market corrections, volatile conditions and the ensuing equity drawdowns.

Hedged portfolios typically employ around 12% less capital than the equivalent buy and hold strategy.

Background to the Market Timing Approach

In an earlier article, I discussed how to use marketing timing techniques to hedge an equity portfolio correlated to the broad market. I showed how, by using signals produced by a trading system modeled on the CBOE VIX index, we can smooth out volatility in an equity portfolio consisting of holdings in the SPDR S&P 500 ETF (NYSEARCA:SPY). An investor will typically reduce their equity holdings by a modest amount, say 20%, or step out of the market altogether during periods when the VIX index is forecast to rise, returning to the market when the VIX is likely to fall. An investment strategy based on this approach would have avoided most of the 2000-03 correction, as well as much of the market turmoil of 2008-09.

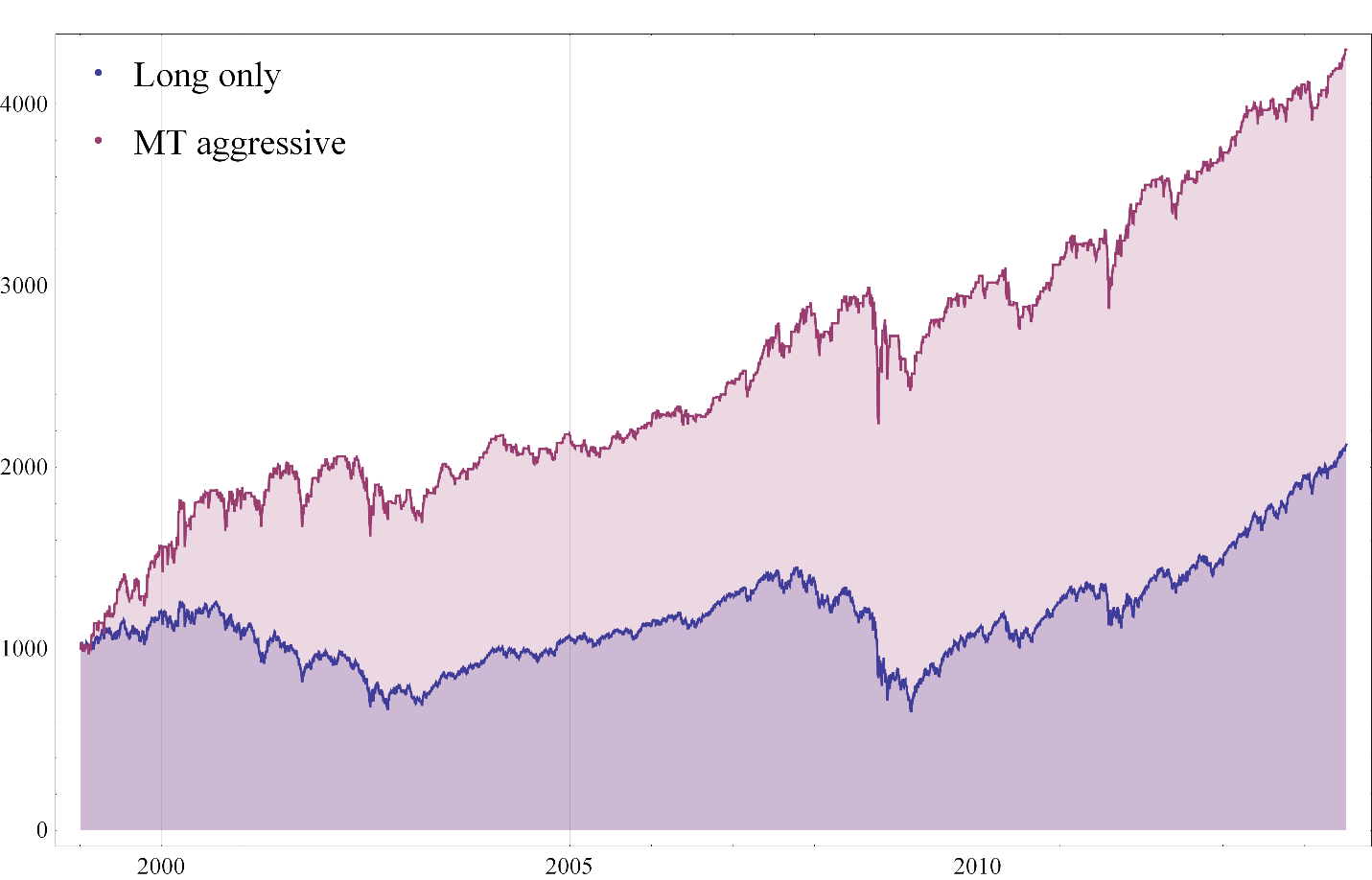

A more levered version of the hedging strategy, which I termed the MT aggressive portfolio, uses the VIX index signals to go to cash during high volatility periods, and then double the original equity portfolio holdings (using standard Reg-T leverage) during benign market conditions, as signaled by the model. The MT aggressive approach would have yielded net returns almost three times greater than that of a buy and hold portfolio in the SPY ETF, over the period from 1999-2014. Even though this version of the strategy makes use of leverage, the average holding in the portfolio would have been slightly lower than in the buy and hold portfolio because, in a majority of days, the strategy would have been 100% in cash. The result is illustrated in the chart in Fig. 1, which is reproduced below.

Fig. 1: Value of $1,000 – Long-Only Vs. MT Aggressive Portfolio

Source: Yahoo Finance.

Note that this approach does not entail shorting any stock. And for investors who prefer to buy and hold, I would make the point that the MT aggressive approach would have enabled you to buy almost three times as much stock in dollar terms by mid-2014 than would be the case if you had simply owned the SPY portfolio over the entire period.

Market Timing and Mutual Funds

With that background, we turn our attention to how we can use market timing techniques to improve returns from equity mutual funds. The funds selected for analysis are the Vanguard 500 Index Admiral (MUTF:VFIAX), Fidelity Spartan 500 Index Advtg (MUTF:FUSVX) and BlackRock S&P 500 Stock K (MUTF:WFSPX). This group of popular mutual funds is a representative sample of available funds that offer broad equity market exposure, with a high degree of correlation to the S&P 500 index. In what follows, we will focus attention on the MT aggressive approach, although other more conservative hedging strategies are equally valid.

We consider performance over the 10-year period from 2005, as at least one of the funds opened late in 2004. In each case, the MT aggressive portfolio is created by exiting the current mutual fund position and going 100% to cash, whenever the VIX model issues a buy signal in the VIX index. Conversely, we double our original mutual fund investment when the model issues a sell signal in the VIX index. In calculating returns, we make an allowance for trading costs of $3 cents per share for all transactions.

Returns for each of the mutual funds, as well as for the SPY ETF and the corresponding MT aggressive hedge strategies, are illustrated in the charts in Fig. 2. The broad pattern is similar in each case – we see significant outperformance of the MT aggressive portfolios relative to their ETF or mutual fund benchmarks. Furthermore, in most cases the hedge strategy tends to exhibit lower volatility, with less prolonged drawdowns during critical periods such as 2000/03 and 2008/09.

Fig. 2 – Value of $1,000: Mutual Fund Vs. MT Aggressive Portfolio January 2005 – June 2014

Source: Yahoo Finance.

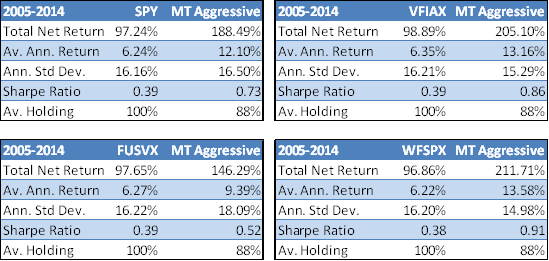

Looking at the performance numbers in more detail, we can see from the tables shown in Fig. 3 that the MT aggressive strategies outperformed their mutual fund buy and hold benchmarks by a substantial margin. In the case of VFIAX and WFSPX, the hedge strategies produce a total net return more than double that of the corresponding mutual fund. With one exception, FUSVX, annual volatility of the MT aggressive portfolio was similar to, or lower than, that of the corresponding mutual fund, confirming our reading of the charts in Fig. 2. As a consequence, the MT aggressive strategies have higher Sharpe Ratios than any of the mutual funds. The improvement in risk adjusted returns is significant – more than double in the case of two of the funds, and about 40% higher in the case of the third.

Finally, we note that the MT aggressive strategies have an average holding that is around 12% lower than the equivalent long-only fund. That’s because of the periods in which investment proceeds are held in cash.

Fig. 3: Mutual Fund and MT Aggressive Portfolio Performance January 2005 – June 2014

Source: Yahoo Finance.

Conclusion

The aim of market timing is to smooth out the returns by hedging, and preferably avoiding altogether periods of market turmoil. In other words, the objective is to achieve the same, or better, rates of return, with lower volatility and drawdowns. We have demonstrated that this can be done, not only when the underlying investment is in an ETF such as SPY, but also where we hold an investment in one of several popular equity mutual funds. Over a 10-year period the hedge strategies produced consistently higher returns, with lower volatility and drawdown, while putting less capital at risk than their counterpart buy and hold mutual fund investments.