This is a follow up to my earlier post on a Calendar Spread Strategy in VIX Futures (more information on calendar spreads ).

The strategy trades the front two months in the CFE VIX futures contract, generating an annual profit of around $25,000 per spread.

DAY TRADING SYSTEM

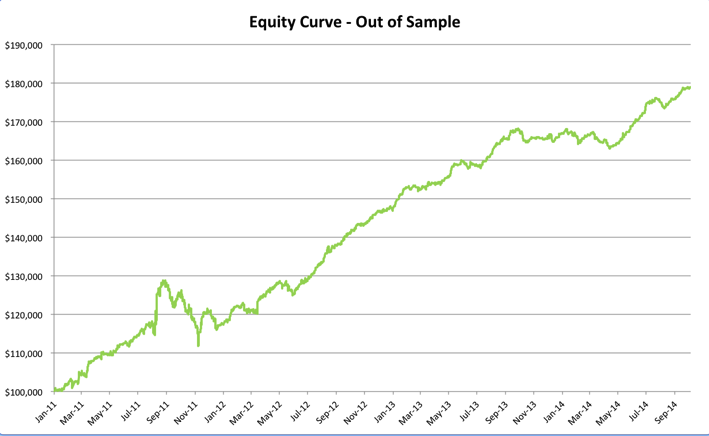

I built an equivalent day trading system in VIX futures in Trading Technologies visual ADL language, using 1-min bar data for 2010, and tested the system out-of-sample in 2011-2014. (for more information on X-Trader/ ADL go here).

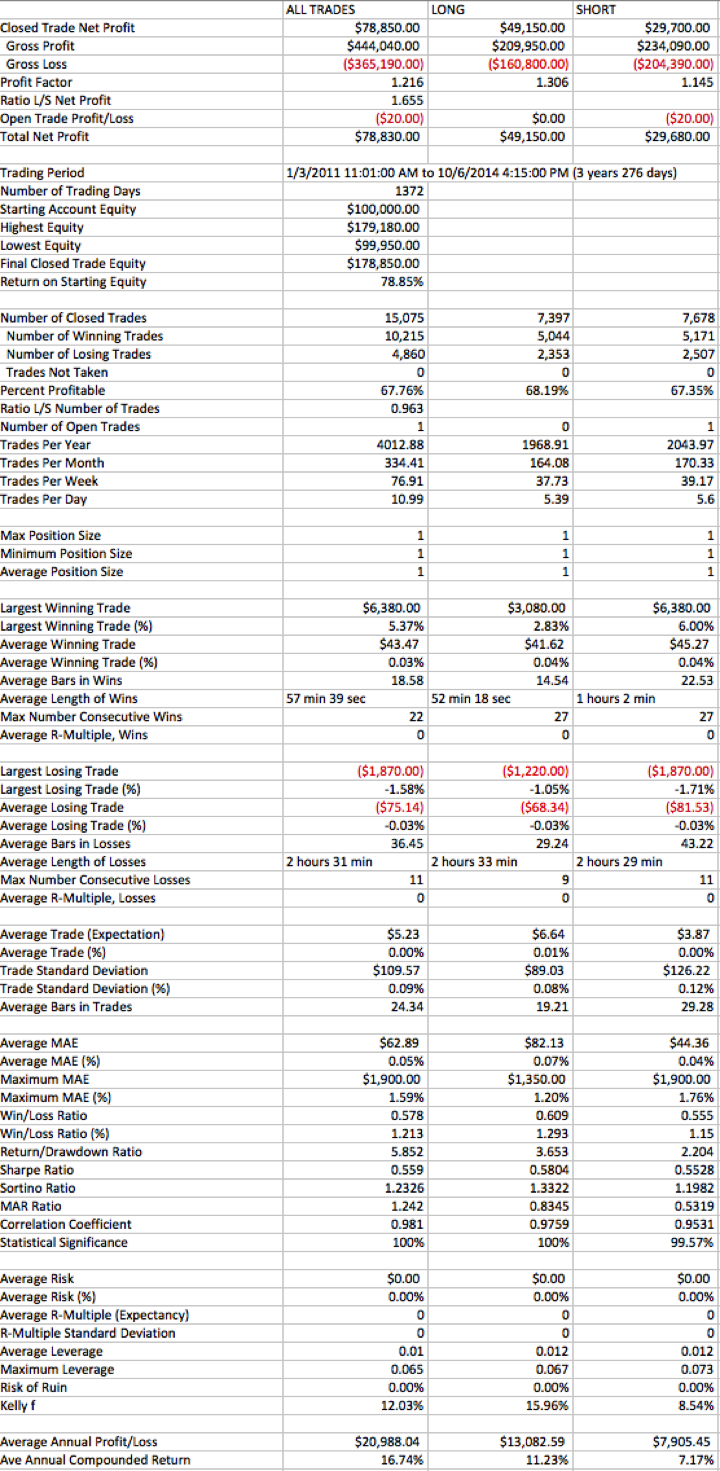

The annual net PL is around $20,000 per spread, with a win rate of 67%. On the downside, the profit factor is rather low and the average trade is barely 1/10 of a tick). Note that this is net of Bid-Ask spread of 0.05 ($50) and commission/transaction costs of $20 per round turn. These cost assumptions are reasonable for online trading at many brokerage firms.

However, the strategy requires you to work the spread to enter passively (thereby reducing the cost of entry). This is usually only feasible on a platform suitable for a high frequency trading, where you can assume that your orders have acceptable priority in the limit order queue. This will result in a reasonable proportion of your passive bids and offers will be executed. Typically the spread trade is held throughout the session, exiting on close (since this is a day trading system).

Overall, while the trading system characteristics are reasonable, the spread strategy is better suited to longer (i.e. overnight) holding periods, since the VIX futures market is not the most liquid and the tick value is large. We’ll take a look at other day trading strategies in more liquid products, like the S&P 500 e-mini futures, for example, in another post.

(click to enlarge)

(click to enlarge)

(click to enlarge)