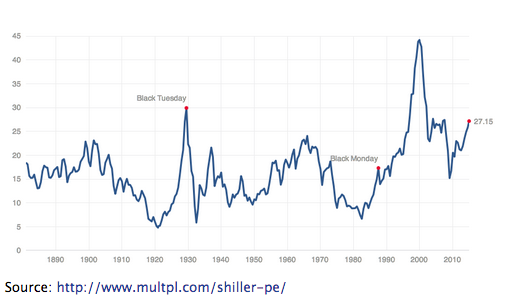

As the commentators at Phoenix Capital point out, the CAPE (cyclical adjusted price to earnings) is showing a reading that suggests the market is now as overvalued as it was in 2007. The only times in history that the market has been more overvalued was during the 1929 bubble and the Tech bubble.

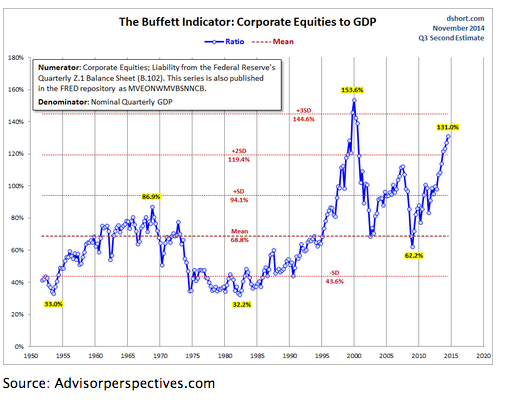

Total stock market cap to GDP, a metric that Warren Buffett’s calls the “single best measure” of stock market value has reached 130%. It’s the highest reading since the DOTCOM bubble (which was 153%). Put another way, stocks are even more overvalued than they were in 2007 and have only been more overvalued during the Tech Bubble: the single biggest stock market bubble in 100 years.

Meanwhile, per Phoenix Capital:

1) Investor sentiment is back to super bullish autumn 2007 levels.

2) Insider selling to buying ratios are back to autumn 2007 levels.

3) Money market fund assets are at 2007 levels (indicating that investors have gone “all in” with stocks).

4) Mutual fund cash levels are at a historic low (again investors are “all in” with stocks).

5) Margin debt (money borrowed to buy stocks) is near record highs.

In plain terms, the market is overvalued, overbought, overextended, and over leveraged. This is a recipe for a correction if not a collapse.

There are only two ways out of this: either GDP picks up, or the market corrects. The Fed is betting the farm on the former outcome. In a sense, it is following a kind of martingale strategy, because the size of the its gamble increases with the level of over-valuation (whether you measure the risk in terms of potential market losses, or increased unemployment-related costs). So, as per gambling theory, providing the bet size is unlimited, the subsequent win (it terms of the surpluses generated from a sizable pickup in GDP ) will be more than enough to offset the costs of supporting the market to these nosebleed levels. In a sense, Bernanke was correct: the bet size is unlimited, if you own the printing presses for the world’s de-facto reserve currency. But what this fails to take account of is the possibility, however remote, of a decoupling from the US$ standard. The world’s appetite for US dollars might yet prove finite. In which case, watch out below.