There is no standard definition of high frequency trading, nor a single type of strategy associated with it. Some strategies generate returns, not by taking any kind of view on market direction, but simply by earning Exchange rebates. In other cases the strategy might try to trade ahead of the news as it flows through the market, from stock to stock (or market to market). Perhaps the most common and successful approach to HFT is market making, where one tries to earn (some fraction of) the spread by constantly quoting both sides of the market. In the latter approach, which involves processing vast numbers of order messages and other market data in order to decide whether to quote (or pull a quote), latency is of utmost importance. I would tend to argue that HFT market making owes its success as much, or more, to computer science than it does to trading or microstructure theory.

By contrast, Systematic Strategies’s approach to HFT has always been model-driven. We are unable to outgun firms like Citadel or Getco in terms of their speed of execution; so, instead, we focus on developing theoretical models of market behavior, on the assumption that we are more likely to identify a source of true competitive advantage that way. This leads to slower, less latency-sensitive strategies (the models have to be re-estimated or recomputed in real time), but which may nonetheless trade hundreds of times a day.

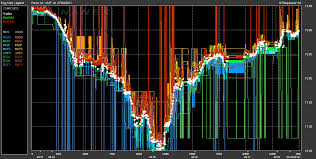

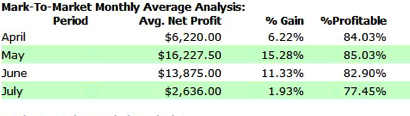

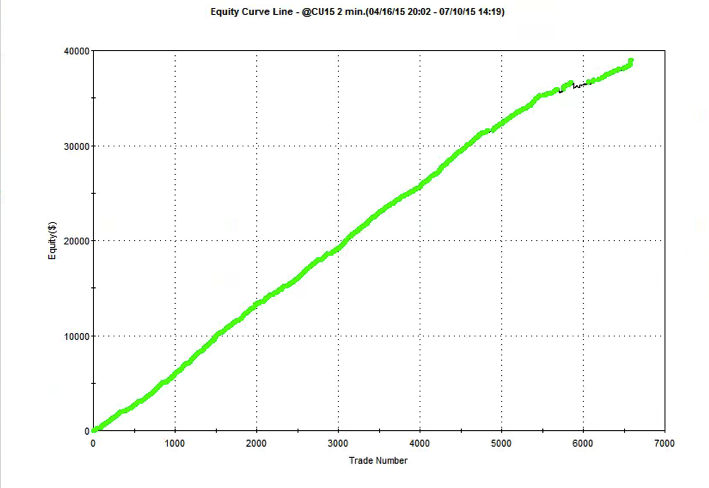

A good example is provided by our high frequency scalping strategy in Corn futures, which trades around 100-200 times a day, with a win rate of over 80%.

One of the most important considerations in engineering a HFT strategy of this kind is to identify a suitable bar frequency. We find that our approach works best using data at frequencies of 1-5 minutes, trading at latencies of around 1 millisec, whereas other firms are reacting to data tick-by-tick, with latencies measured in microseconds.

Often strategies are built using only data derived from with a single market, based on indicators involving price action, pattern trading rules, volume or volatility signals. In other cases, however, signals are derived from other, related markets: the VXX-ES-TY complex would be a typical example of this kind of inter-market approach.

When we build strategies we often start by using a simple retail platform like TradeStation or MultiCharts. We know that if the strategy can make money on a platform with retail levels of order and market data latency (and commission rates), then it should perform well when we transfer it to a production environment, with much lower latencies and costs. We might be able to trade only 1-2 contracts in TradeStation, but in production we might aim to scale that up to 10-15 contract per trade, or more, depending on liquidity. For that reason we prefer to trade only intraday, when market liquidity is deepest; but we often find sufficient levels of liquidity to make trading worthwhile 1-2 hours before the open of the day session.

Generally, while we look for outside money for our lower frequency hedge fund strategies, we tend not to do so for our HFT strategies. After all, what’s the point? Each strategy has limited capacity and typically requires no more than a $100,000 account, at most. And besides, with Sharpe Ratios that are typically in double-digits, it’s usually in our economic interest to use all of the capacity ourselves. Nor do we tend to license strategies to other trading firms. Again, why would we? If the strategies work, we can earn far more from trading rather than licensing them.

We have, occasionally, developed strategies for other firms for markets in which we have no interest (the KOSPI springs to mind). But these cases tend to be the exception, rather than the rule.