Several readers responded to my recent invitation to send me details of their trading strategies, to see if I could develop a meta-strategy with superior overall performance characteristics (see original post here).

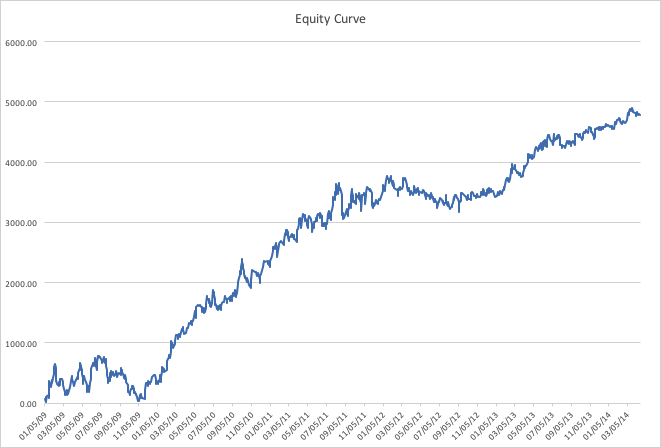

One reader sent me the following strategy in EUR futures, with a promising-looking equity curve over the period from 2009-2014.

I have no information about the underlying architecture of the strategy, but a performance analysis shows that it trades approximately once per day, with a win rate of 49%, a PNL per trade of $4.79 and a IR estimated to be 2.6.

Designing the Meta-Strategy

My task was to see if I could design a meta-strategy that would “trade” the underlying strategy, i.e. produce signals to turn the underlying strategy on or off. Here we are designing a long-only strategy, where a “buy” trade represents the signal to turn the underlying strategy on, while an exit trade from the meta-strategy turns the underlying strategy off.

The meta-strategy is built in trade time rather than calendar time – we don’t want the meta-strategy trying to turn the underlying trading strategy on or off while it is in the middle of a trade. The data we use in the design exercise is the trade-by-trade equity curve, including the date and timestamp and the open, high, low and close values of the equity curve for each trade.

No allowance for trading costs is necessary since all of the transaction costs are baked into the PNL of the underlying strategy – there are no additional costs entailed in turning the strategy on or off, as long as we do that in a period when there is no open position.

In designing the meta-strategy I chose simply to try to improve the overall net PNL. This is a good starting point, but one would typically go on to consider a variety of other possible criteria, including, for example, Net Profit / Av. Max Drawdown, Net Profit / Flat Time, MAR Ratio, Sharpe Ratio, Kelly Criterion, or a combination of them.

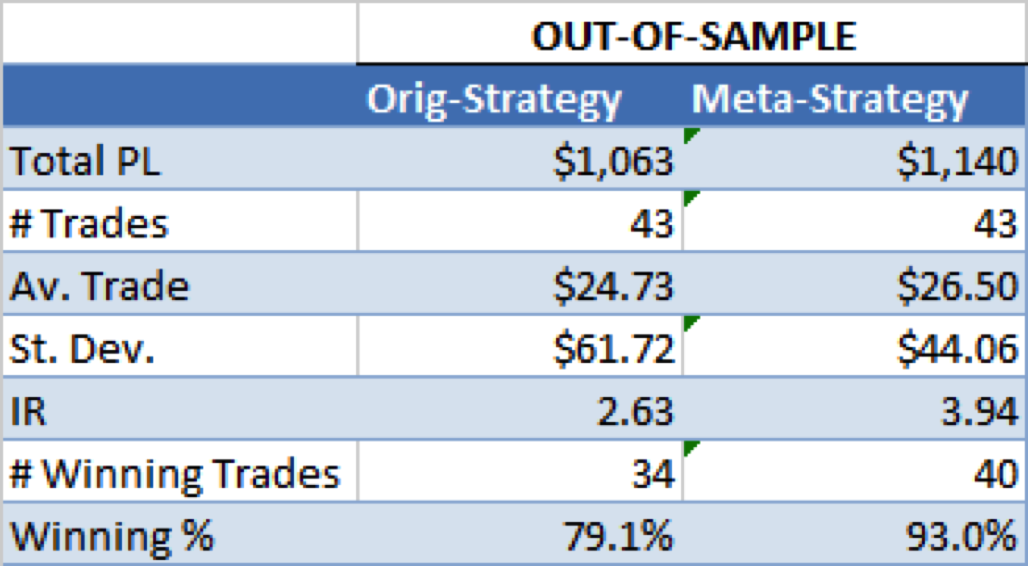

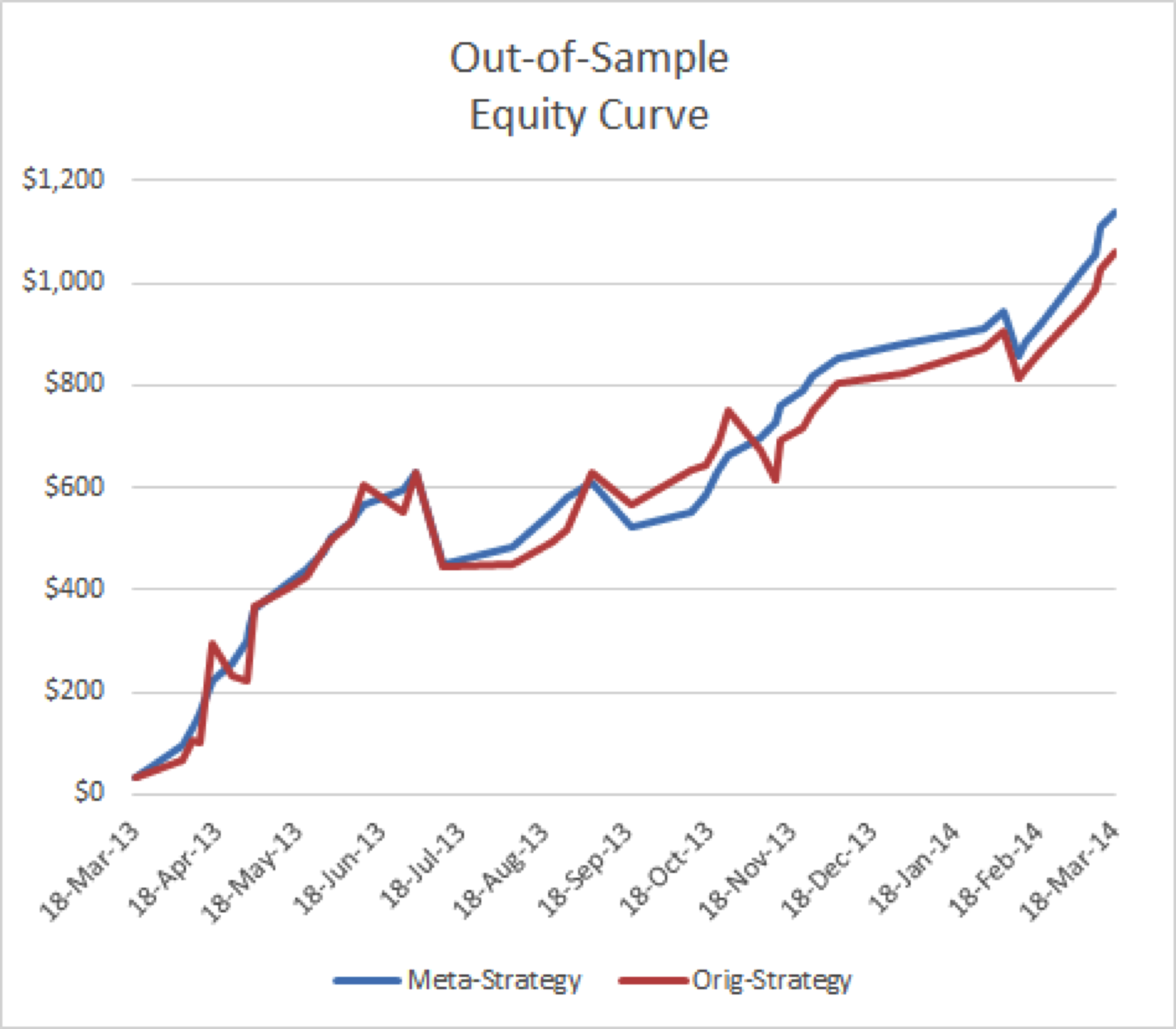

I used 80% of the trade data to design and test the strategy and reserved 20% of the data to test the performance of the meta-strategy out-of-sample.

Results

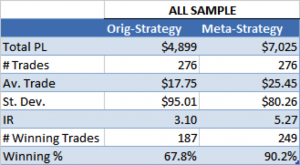

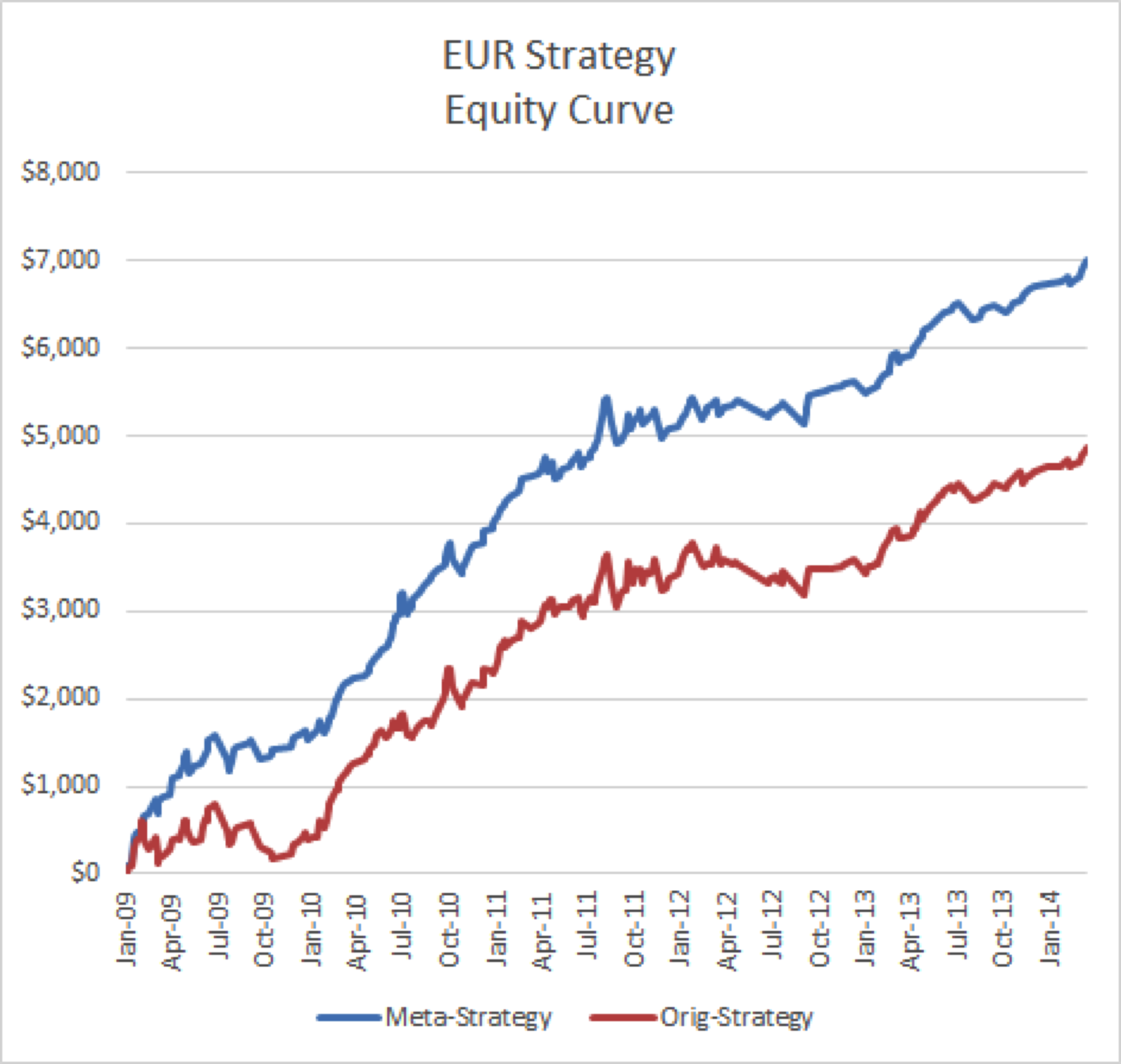

The analysis summarized below shows a clear improvement in the overall performance of the meta-strategy, compared to the underlying strategy. Net PNL and Average Trade are increased by 40%, while the trade standard deviation is noticeably reduced, leading to a higher IR of 5.27 vs 3.10. The win rate increases from around 2/3 to over 90%.

Although not as marked, the overall improvement in strategy performance metrics during the out-of-sample test period is highly significant, both economically and statistically.

Note that the Meta-strategy is a long-only strategy in which each “trade” is a period in which the system trades the underlying EUR futures strategy. So in fact, in the Meta-strategy, each trade represents a number of successive underlying, real trades (which of course may be long or short).

Put another way, the Meta-Strategy turns the underlying trading strategy on and off 276 times in total.

Conclusion

It is feasible to design a meta-strategy that improves the overall performance characteristics of an underlying trading strategy, by identifying the higher-value trades and turning the strategy on or off based on forecasts of its future performance.

No knowledge is required of the mechanics of the underlying trading strategy in order to design a profitable Meta-strategy.

Meta-strategies have been successfully applied to problems of capital allocation, where decisions are made on a regular basis about how much capital to allocate to multiple trading strategies, or traders.