The SPDR S&P 500 ETF (SPY) is one of the widely traded ETF products on the market, with around $200Bn in assets and average turnover of just under 200M shares daily. So the likelihood of being able to develop a money-making trading system using publicly available information might appear to be slim-to-none. So, to give ourselves a fighting chance, we will focus on an attempt to predict the overnight movement in SPY, using data from the prior day’s session.

In addition to the open/high/low and close prices of the preceding day session, we have selected a number of other plausible variables to build out the feature vector we are going to use in our machine learning model:

The daily volume

The previous day’s closing price

The 200-day, 50-day and 10-day moving averages of the closing price

The 252-day high and low prices of the SPY series

We will attempt to build a model that forecasts the overnight return in the ETF, i.e. [O(t+1)-C(t)] / C(t)

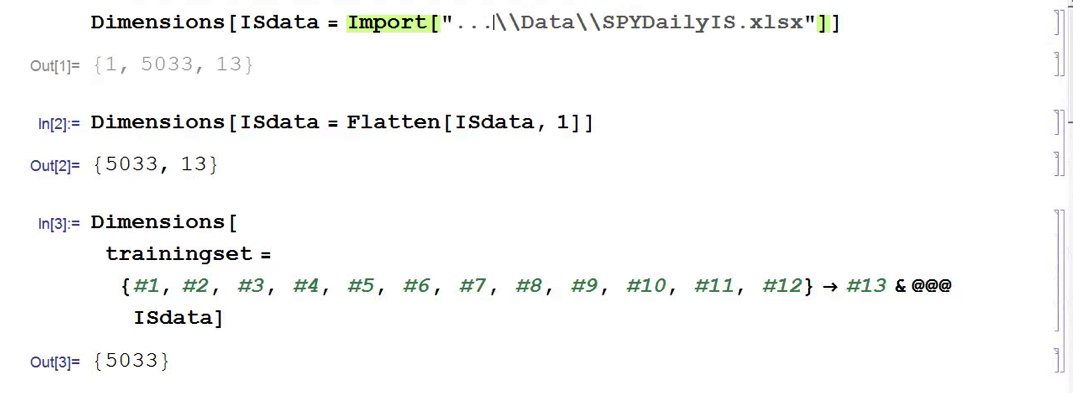

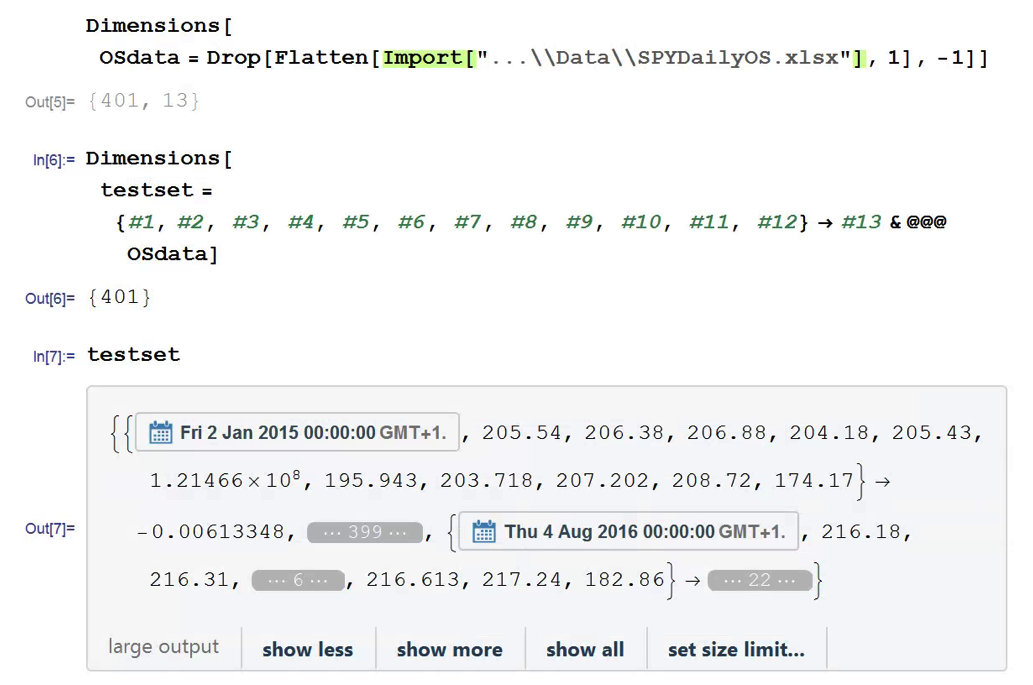

In this exercise we use daily data from the beginning of the SPY series up until the end of 2014 to build the model, which we will then test on out-of-sample data running from Jan 2015-Aug 2016. In a high frequency context a considerable amount of time would be spent evaluating, cleaning and normalizing the data. Here we face far fewer problems of that kind. Typically one would standardized the input data to equalize the influence of variables that may be measured on scales of very different orders of magnitude. But in this example all of the input variables, with the exception of volume, are measured on the same scale and so standardization is arguably unnecessary.

First, the in-sample data is loaded and used to create a training set of rules that map the feature vector to the variable of interest, the overnight return:

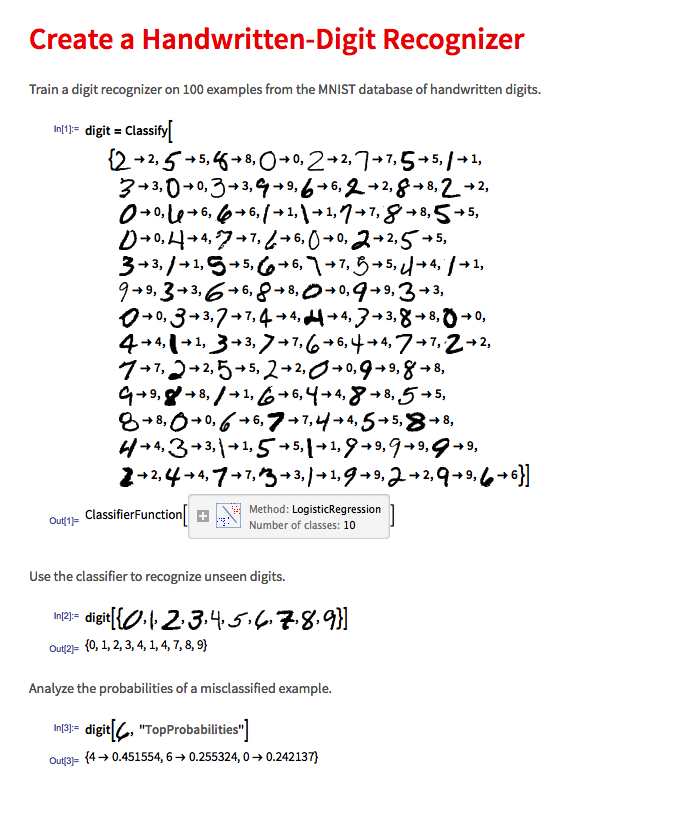

In Mathematica 10 Wolfram introduced a suite of machine learning algorithms that include regression, nearest neighbor, neural networks and random forests, together with functionality to evaluate and select the best performing machine learning technique. These facilities make it very straightfoward to create a classifier or prediction model using machine learning algorithms, such as this handwriting recognition example:

We create a predictive model on the SPY trainingset, allowing Mathematica to pick the best machine learning algorithm:

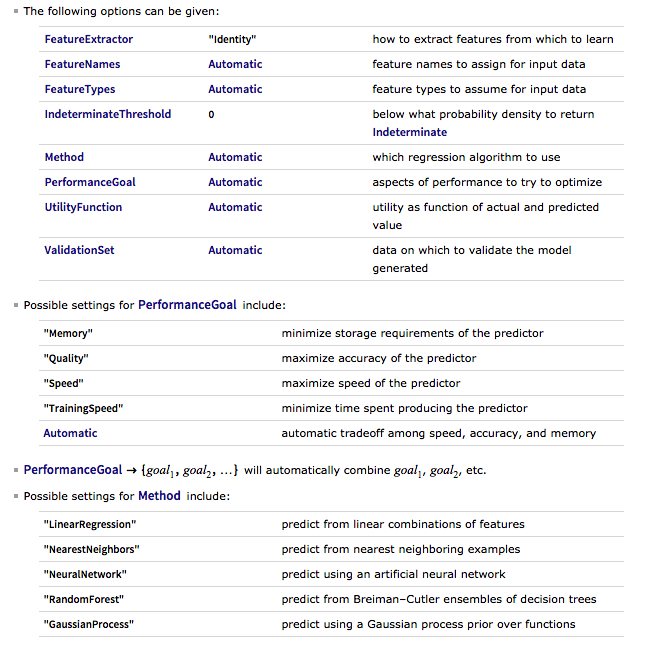

There are a number of options for the Predict function that can be used to control the feature selection, algorithm type, performance type and goal, rather than simply accepting the defaults, as we have done here:

Having built our machine learning model, we load the out-of-sample data from Jan 2015 to Aug 2016, and create a test set:

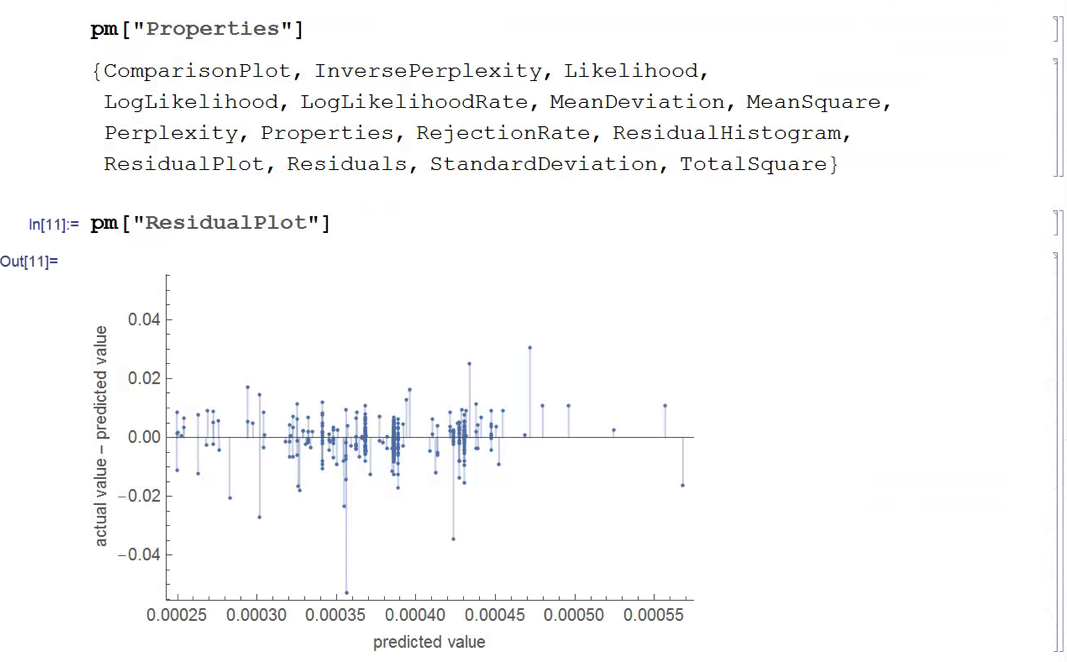

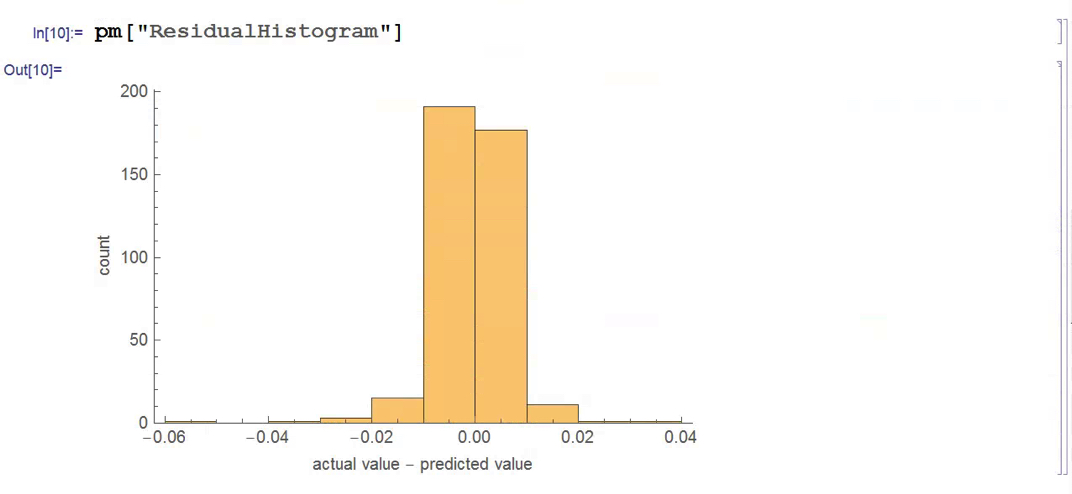

We next create a PredictionMeasurement object, using the Nearest Neighbor model , that can be used for further analysis:

There isn’t much dispersion in the model forecasts, which all have positive value. A common technique in such cases is to subtract the mean from each of the forecasts (and we may also standardize them by dividing by the standard deviation).

The scatterplot of actual vs. forecast overnight returns in SPY now looks like this:

There’s still an obvious lack of dispersion in the forecast values, compared to the actual overnight returns, which we could rectify by standardization. In any event, there appears to be a small, nonlinear relationship between forecast and actual values, which holds out some hope that the model may yet prove useful.

From Forecasting to Trading

There are various methods of deploying a forecasting model in the context of creating a trading system. The simplest route, which we will take here, is to apply a threshold gate and convert the filtered forecasts directly into a trading signal. But other approaches are possible, for example:

Combining the forecasts from multiple models to create a prediction ensemble

Using the forecasts as inputs to a genetic programming model

Feeding the forecasts into the input layer of a neural network model designed specifically to generate trading signals, rather than forecasts

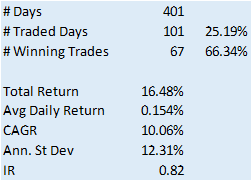

In this example we will create a trading model by applying a simple filter to the forecasts, picking out only those values that exceed a specified threshold. This is a standard trick used to isolate the signal in the model from the background noise. We will accept only the positive signals that exceed the threshold level, creating a long-only trading system. i.e. we ignore forecasts that fall below the threshold level. We buy SPY at the close when the forecast exceeds the threshold and exit any long position at the next day’s open. This strategy produces the following pro-forma results:

Conclusion

The system has some quite attractive features, including a win rate of over 66% and a CAGR of over 10% for the out-of-sample period.

Obviously, this is a very basic illustration: we would want to factor in trading commissions, and the slippage incurred entering and exiting positions in the post- and pre-market periods, which will negatively impact performance, of course. On the other hand, we have barely begun to scratch the surface in terms of the variables that could be considered for inclusion in the feature vector, and which may increase the explanatory power of the model.

In other words, in reality, this is only the beginning of a lengthy and arduous research process. Nonetheless, this simple example should be enough to give the reader a taste of what’s involved in building a predictive trading model using machine learning algorithms.

Spending 12-14 hours a day managing investors’ money doesn’t leave me a whole lot of time to sit around watching TV. And since I have probably less than 10% of the ad-tolerance of a typical American audience member, I inevitably turn to TiVo, Netflix, or similar, to watch a commercial-free show. Which means that I am inevitably several years behind the cognoscenti of the au-courant. This has its pluses: I avoid a lot of drivel that way.

So it was that I recently tuned in to watch Deadwood, a masterpiece of modern drama written by the talented David Milch, of NYPD Blue fame. The setting of the show is unpromising: a mud-caked camp in South Dakota around the turn of the 19th century that appears to portend yet another formulaic Western featuring liquor, guns, gals and gold and not much else. The first episode appeared at first to confirm my lowest expectations. I struggled through the second. But by the third I was hooked.

What makes Deadwood such a triumph are its finely crafted plots and intricate sub-plots; the many varied and often complex characters, superbly played by Ian McShane (with outstanding performances by Brad Dourif, Powers Boothe, amongst an abundance of others, no less gifted); and, of course, the dialogue.

Yes, the dialogue: hardly the crowning glory of the typical Hollywood Western. And here, to make matters worse, almost every sentence uttered by many of the characters is replete with such shocking profanity that one is eventually numbed into accepting it as normal. But once you get past that, something strange and rather wonderful overtakes you: a sense of being carried along on a river of creative wordsmith-ing that at times eddies, bubbles, plunges and roars its way through scenes that are as comedic, dramatic and action-packed as any I have seen on film. For those who have yet to enjoy the experience, I offer one small morsel:

Around the start of Series 2 a rather strange idea occurred to me that, try as I might, I was increasingly unable to suppress as the show progressed: that the writing – some of it at least – was almost Shakespearian in its ingenuity and, at times, lyrical complexity.

Convinced that I had taken leave of my senses I turned to Google and discovered, to my surprise, that there is a whole cottage industry of Deadwood fans who had made the same connection. There is even – if you can imagine it – an online quiz that tests if you are able to identify the source of a number of quotes that might come from the show, or one of the Bard’s many plays. I kid you not:

Intrigued, I took the test and scored around 85%. Not too bad for a science graduate, although I expect most English majors would top 90%-95%. That gave me an idea: could one develop a machine learning algorithm to do the job?

Here’s how it went.

Milch or Shakespeare? – A Machine Learning Classification Algorithm

We start by downloading the text of a representative selection of Shakespeare’s plays, avoiding several of the better-known works from which many of the quotations derive:

For testing purposes, let’s download a sample of classic works by other authors:

Let’s build an initial test classifier, as follows:

It seems to work ok:

So far so good. Let’s import the script for Deadwood series 1-3:

Next, let’s import the quotations used in the online test:

etc

We need to remove the relevant quotes from the Deadwood script file used to train the classifier, of course (otherwise it’s cheating!). We will strip an additional 200 characters before the start of each quotation, and 500 characters after each quotation, just for good measure:

and so on….

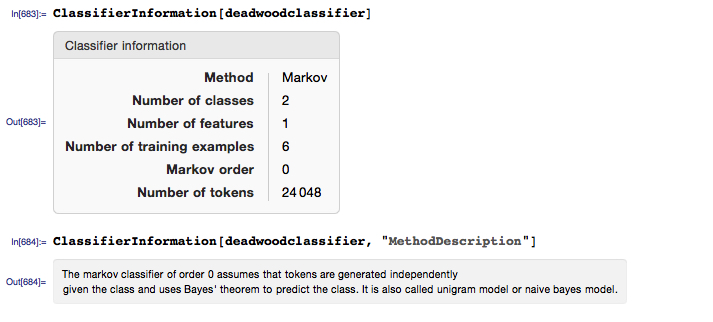

Now we are ready to build our classifier:

And we can obtain some information about the classifier, as follows:

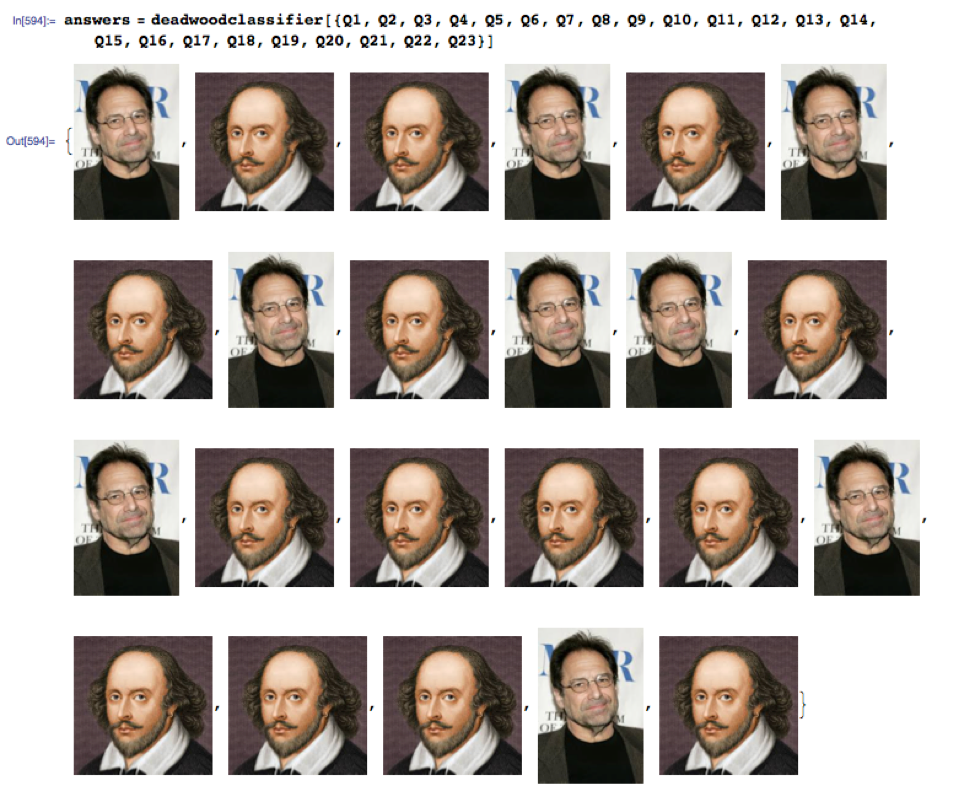

Let’s see how it performs:

Or, if you prefer tabular form:

The machine learning model scored a total of 19 correct answers out of 23, or 82%.

Fooling the Machine

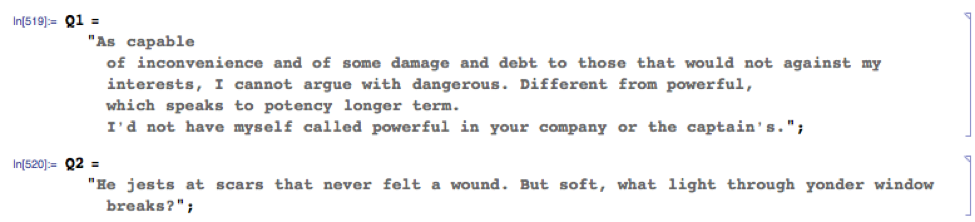

Let’s take a look as some of the questions the algorithm got wrong.

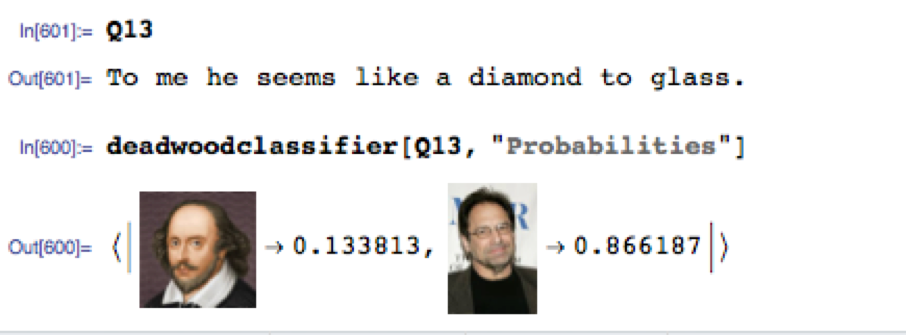

Quotation no. 13 is challenging, as it comes from Pericles, one of Shakespeare’s lesser-know plays and the idiom appears entirely modern. The classifier assigns an 87% probability of Milch being the author (I got it wrong too).

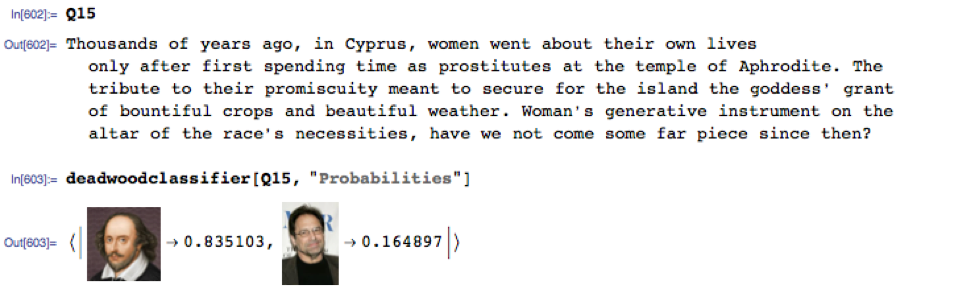

On Quotation no. 15 the algorithm was just as mistaken, but in the other direction (I got this one right, but only because I recalled the monologue from the episode):

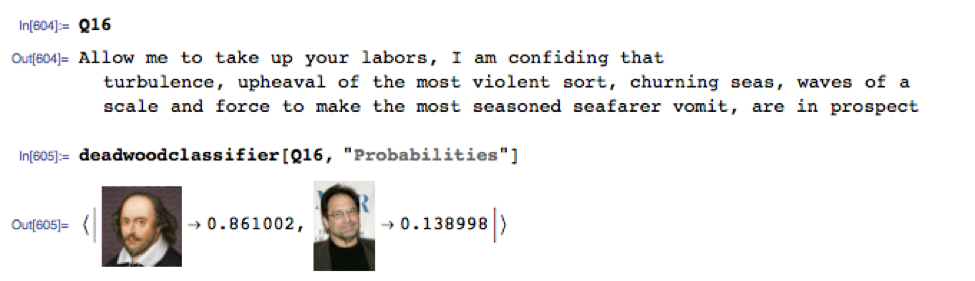

Quotation no.16 strikes me as entirely Shakespearian in form and expression and the classifier thought so too, favoring the Bard by 86% to only 14% for Milch:

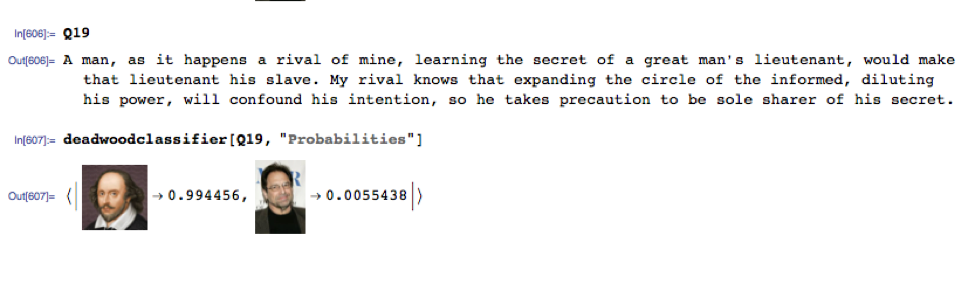

Quotation no. 19 had the algorithm fooled completely. It’s a perfect illustration of a typical kind of circumlocution favored by Shakespeare that is imitated so well by Milch’s Deadwood characters:

Conclusion

The model clearly picked up distinguishing characteristics of the two authors’ writings that enabled it to correctly classify 82% of the quotations, quite a high percentage and much better than we would expect to do by tossing a coin, for example. It’s a respectable performance, but I might have hoped for greater accuracy from the model, which scored about the same as I did.

I guess those who see parallels in the writing of William Shakespeare and David Milch may be onto something.

Postscript

The Hollywood Reporter recently published a story entitled

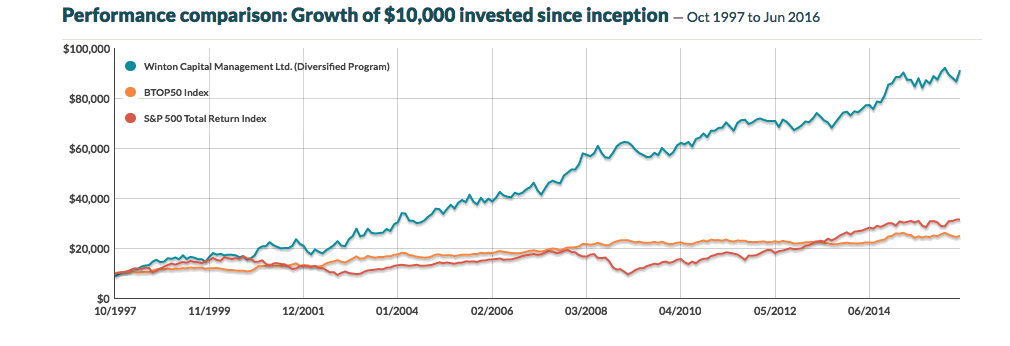

Winton Capital Management is a renowned quant fund and one of the world’s largest, most successful CTAs. The firm’s flagship investment strategy, the Winton Diversified Program, follows a systematic investment process that is based on statistical research to invest globally long and short, using leverage, in a diversified range of liquid instruments, including exchange traded futures, forwards, currency forwards traded over the counter, equity securities and derivatives linked to such securities.

The performance of the program over the last 19 years has been impressive, especially considering its size, which now tops around $13Bn in assets.

Source: CTA Performance

A Meta-Strategy to Beat Winton Capital

With that background, the idea of improving the exceptional results achieved by David Harding and his army of quants seems rather far fetched, but I will take a shot. In what follows, I am assuming that we are permitted to invest and redeem an investment in the program at no additional cost, other than the stipulated fees. This is, of course, something of a stretch, but we will make that assumption based on the further stipulation that we will make no more than two such trades per year.

Using the performance data of the WDP from 1997-2012, we develop a meta-strategy that seeks to time an investment in the program, taking profits after reaching a specified profit target, which is based on the TrueRange, or after holding for a maximum of 8 months. The key part of the strategy code is as follows:

If MarketPosition = 1 then begin

TargPrL = EntryPrice + TargFr * TrueRange;

Sell(“ExTarg-L”) next bar at TargPrL limit;

If Time >= TimeEx or BarsSinceEntry >= NBarEx1 or (BarsSinceEntry >= NBarEx3 and C > EntryPrice)

or (BarsSinceEntry >= NBarEx2 and C < EntryPrice) then

Sell(“ExMark-L”) next bar at market;

end;

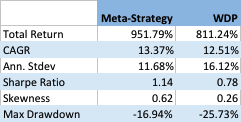

It appears that by timing an investment in the program we can improve the CAGR by around 0.86% per year, and with annual volatility that is lower by around 4.4% annually. As a consequence, the Sharpe ratio of the meta-strategy is considerably higher: 1.14 vs 0.78 for the WDP.

Like most trend-following CTA strategies, Winton’s WDP has positive skewness, an attractive feature that means that the strategy has a preponderance of returns in the positive right tail of the distribution. Also in common with most CTA strategies, on the other hand, the WDP suffers from periodic large drawdowns, in this case amounting to -25.73%.

The meta-strategy improves on the baseline profile of the WDP, increasing the positive skew, while substantially reducing downside risk, leading to a much lower maximum drawdown of -16.94%.

Conclusion

Despite its stellar reputation in the CTA world, investors could theoretically improve on the performance of Winton Capital’s flagship program by using a simple meta-strategy that times entry to and exit from the program using simple technical indicators. The meta-strategy produces higher returns, lower volatility and with higher positive skewness and lower downside risk.

The current 15-year drought in the South West is the most severe since recordkeeping for the Colorado River began in 1906. Lake Mead, which supplies much of the water to Colorado Basin communities, is now more than half empty.

A 120 foot high band of rock, bleached white by the water, and known as the “bathtub ring” encircles the lake, a stark reminder of the water crisis that has enveloped the surrounding region. The Colorado River takes a 1,400 mile journey from the Rockies to Mexico, irrigating over 5 million acres of farmland in the Basin states of Wyoming, Utah, Colorado, New Mexico, Nevada, Arizona, and California.

The Colorado River Compact signed in 1922 enshrined the States’ water rights in law and Mexico was added to the roster in 1994, taking the total allocation to over 16.5 million acre-feet per year. But the average freshwater input to the lake over the century from 1906 to 2005 reached only 15 million acre-feet. The river can’t come close to meeting current demand and the problem is only likely to get worse. A 2009 study found that rainfall in the Colorado Basin could fall as much as 15% over the next 50 years and the shortfall in deliveries could reach 60% to 90% of the time.

Impact on Las Vegas

With an average of only 4 inches of rain a year, and a daily high temperatures of 103 o F during the summer, Las Vegas is perhaps the most hard pressed to meet the demand of its 2 million residents and 40 million visitors annually.

Despite its conspicuous consumption, from the tumbling fountains of the Bellagio to the Venetian’s canals, since 2002, Las Vegas has been obliged to cut its water use by a third, from 314 gallons per capita a day to 212. The region recycles around half of its wastewater which is piped back into Lake Mead, after cleaning and treatment. Residents are allowed to water their gardens no more than one day a week in peak season, and there are stiff fines for noncompliance.

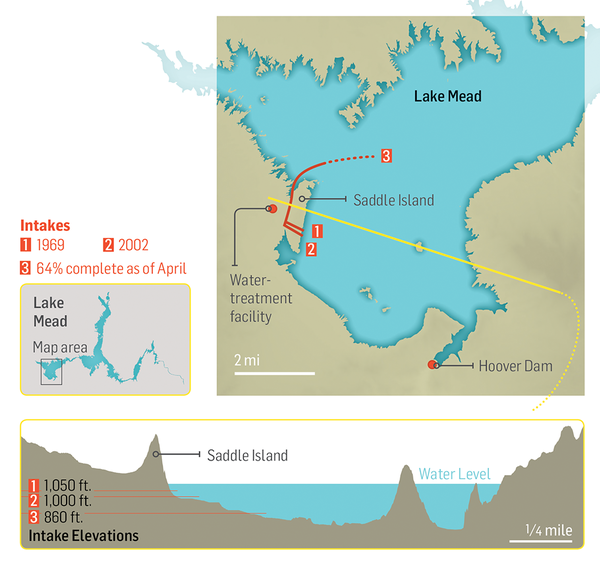

The Third Straw

Historically, two intake pipes carried water from Lake Mead to Las Vegas, about 25 miles to the west. In 2012, realizing that the highest of these, at 1050 feet, would soon be sucking air, the Southern Nevada Water Authority began construction of a new pipeline. Known as the Third Straw, Intake No. 3 reaches 200 feet deeper into the lake—to keep water flowing for as long as there’s water to pump. The new pipeline, which commenced operations in 2015, doesn’t draw more water from the lake than before, or make the surface level drop any faster. But it will keep taps flowing in Las Vegas homes and casinos even if drought-stricken Lake Mead drops to its lowest levels.

Modeling Water Levels in Lake Mead

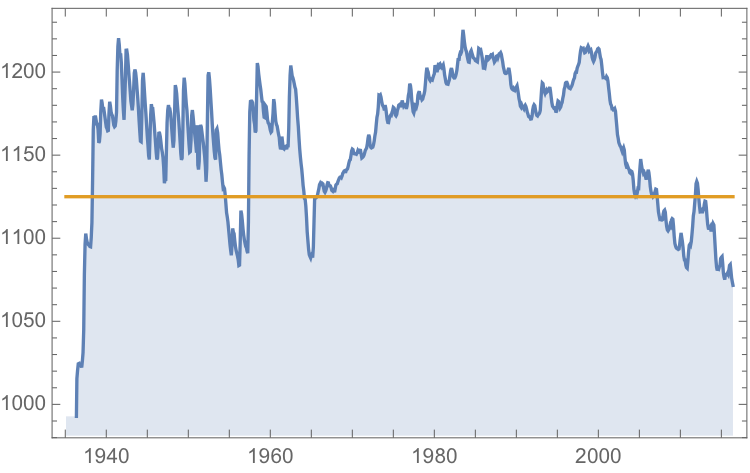

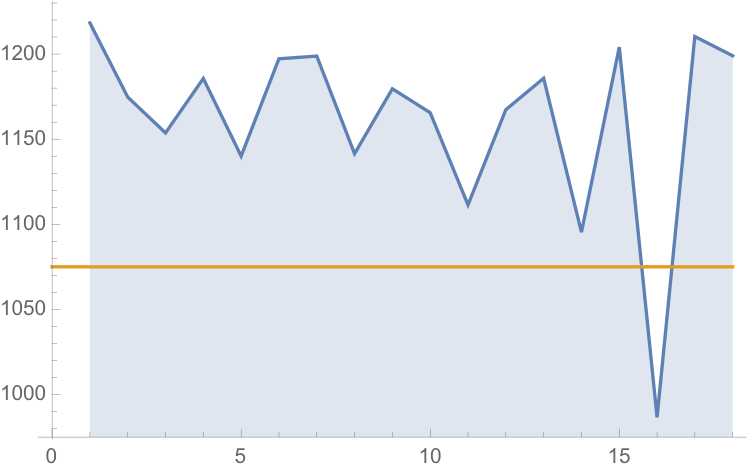

The monthly reported water levels in Lake Mead from Feb 1935 to June 2016 are shown in the chart below. The reference line is the drought level, historically defined as 1,125 feet.

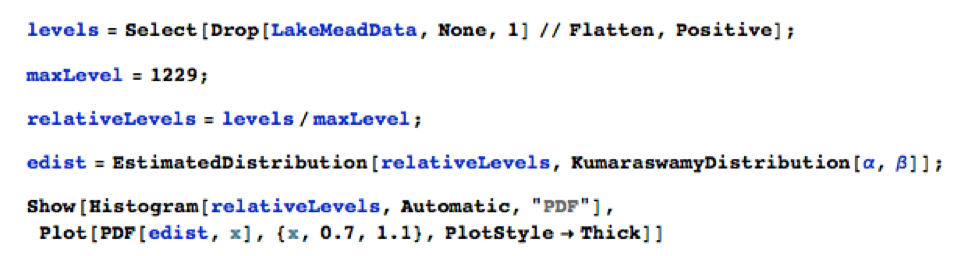

One statistical technique widely applied in hydrology involves fitting a Kumaraswamy distribution to the relative water level. According to the Arizona Game and Fish Department, the maximum lake level is 1229 feet. We model the water level relative to the maximum level, as follows.

The fit of the distribution appears quite good, even in the tails:

ProbabilityPlot[relativeLevels, edist]

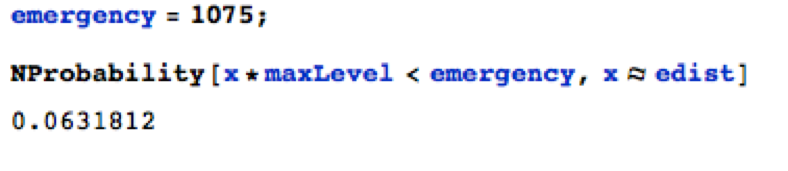

Since water levels have been below the drought level for some time, let’s instead consider the “emergency” level, 1,075 feet. According to this model, there is just over a 6% chance of Lake Mead hitting the emergency level and, consequently, a high probability of breaching the emergency threshold some time over before the end of 2017.

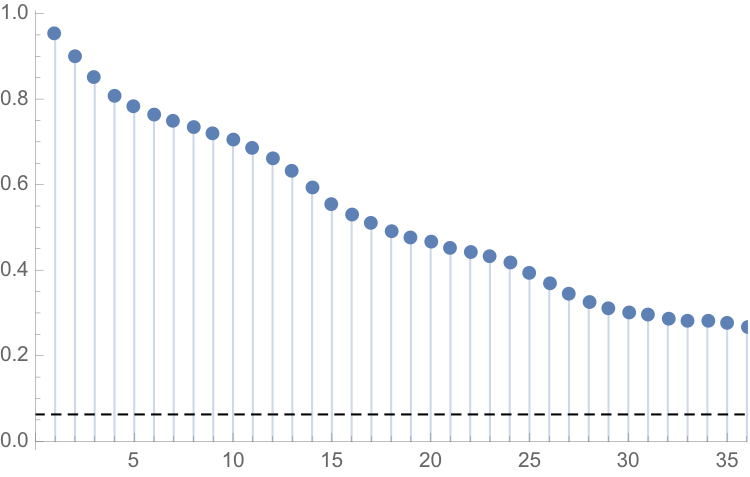

One problem with this approach is that it assumes that each observation is drawn independently from a random variable with the estimated distribution. In reality, there are high levels of autocorrelation in the series, as might be expected: lower levels last month typically increase the likelihood of lower levels this month. The chart of the autocorrelation coefficients makes this pattern clear, with statistically significant coefficients at lags of up to 36 months.

ts[“ACFPlot”]

An alternative methodology that enables us to take account of the autocorrelation in the process is time series analysis. We proceed to fit an autoregressive moving average (ARMA) model as follows:

tsm = TimeSeriesModelFit[ts, “ARMA”]

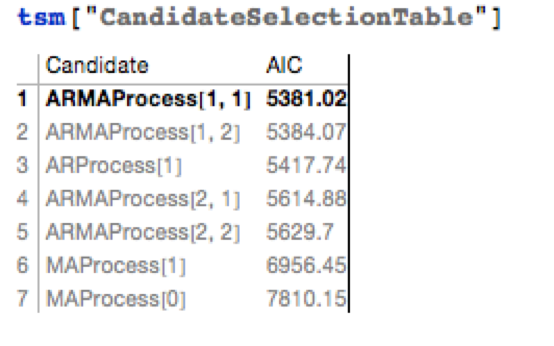

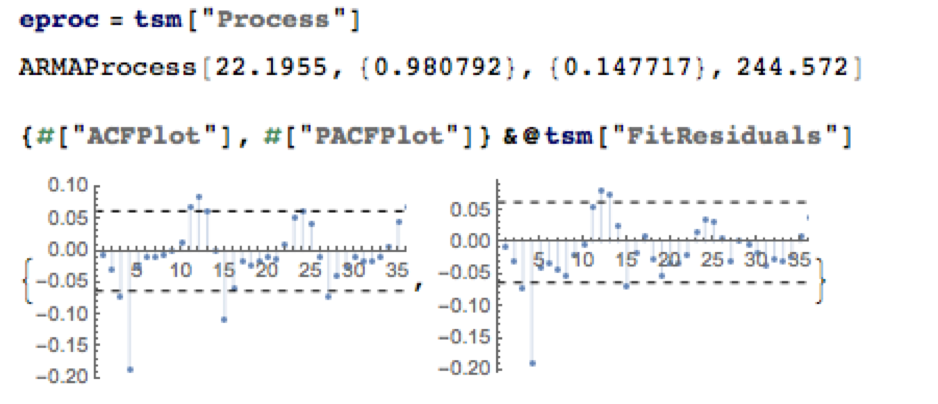

The best fitting model in an ARMA(1,1) model, according to the AIC criterion:

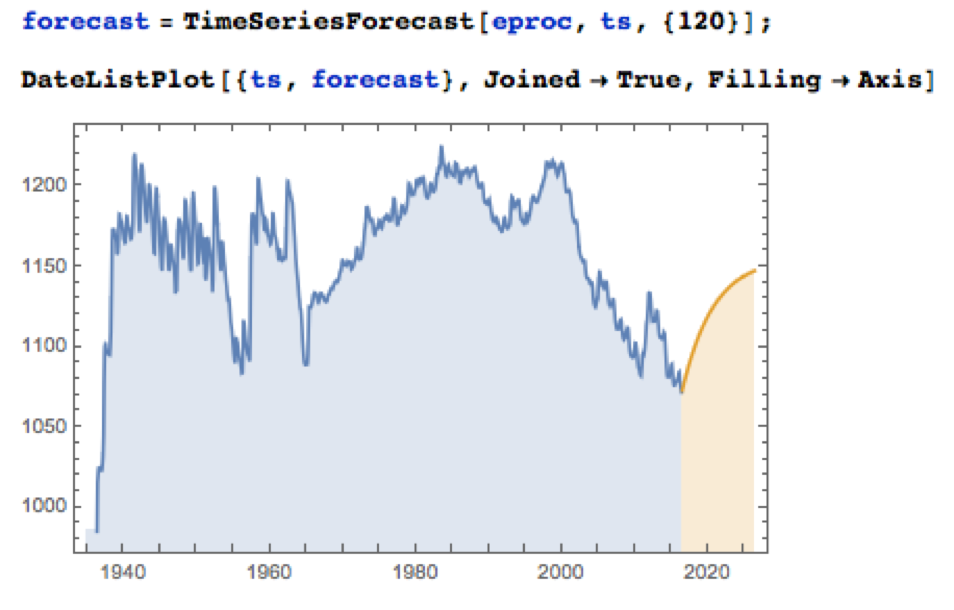

Applying the fitted ARMA model, we forecast the water level in Lake Mead over the next ten years as shown in the chart below. Given the mean-reverting moving average component of the model, it is not surprising to see the model forecasting a return to normal levels.

There is some evidence of lack of fit in the ARMA model, as shown in the autocorrelations of the model residuals:

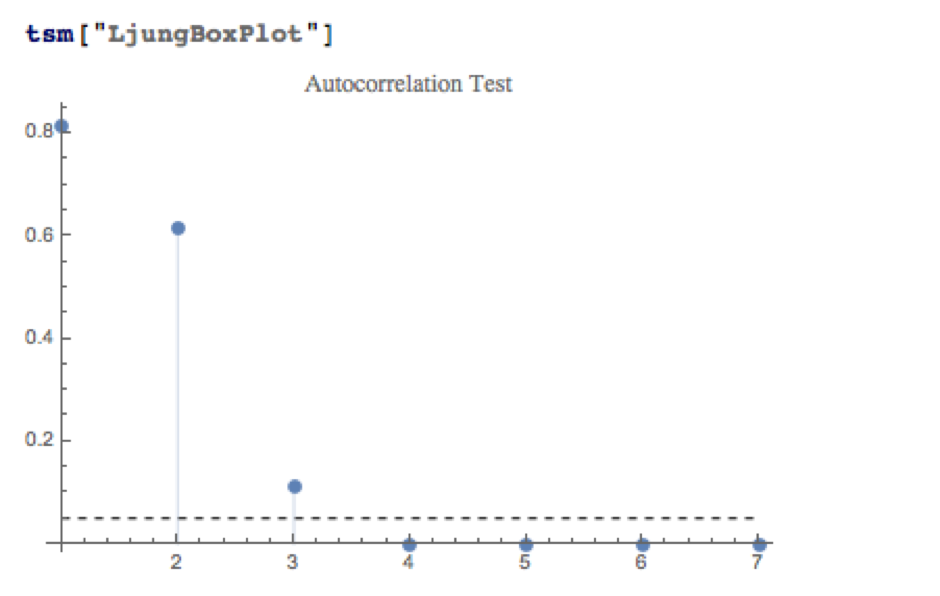

A formal test reveals that residual autocorrelations at lags 4 and higher are jointly statistically significant:

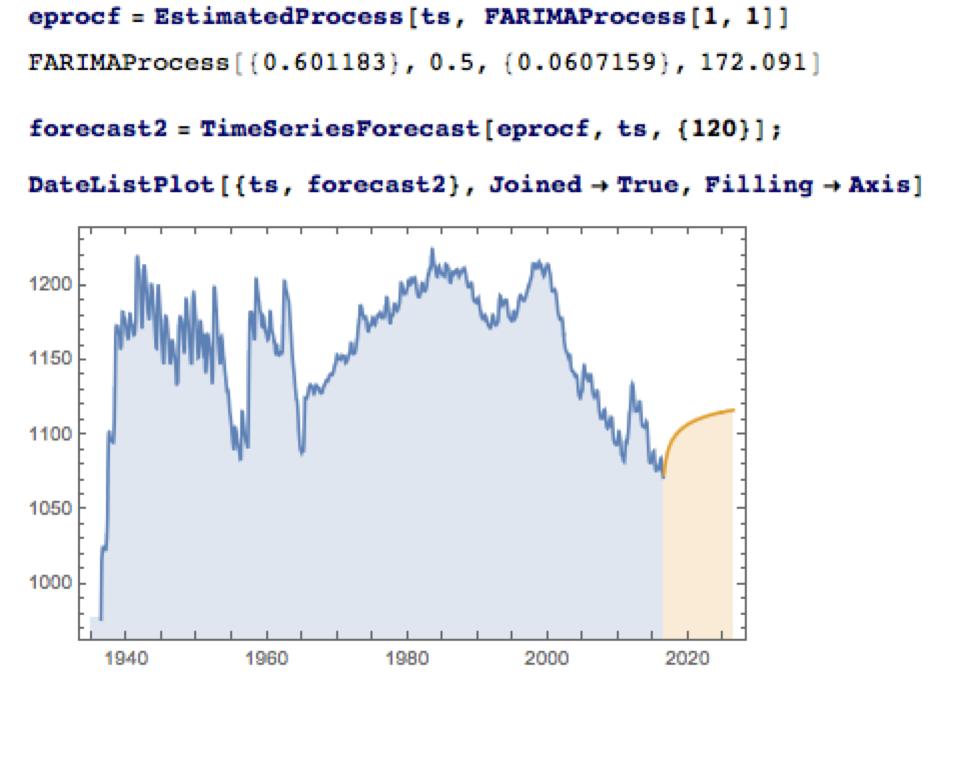

The slowly decaying pattern of autocorrelations in the water level series suggests a possible “long memory” effect, which can be better modelled as a fractionally integrated process. The forecasts from such a model, like the ARMA model forecasts, display a tendency to revert to a long term mean; but the reversion process is dampened by the reinforcing, long-memory effect captured in the FARIMA model.

The Prospects for the Next Decade

Taking the view that the water level in Lake Mead forms a stationary statistical process, the likelihood is that water levels will rise to 1,125 feet or more over the next ten years, easing the current water shortage in the region.

On the other hand, there are good reasons to believe that there are exogenous (deterministic) factors in play, specifically the over-consumption of water at a rate greater than the replenishment rate from average rainfall levels. Added to this, plausible studies suggest that average rainfall in the Colorado Basin is expected to decline over the next fifty years. Under this scenario, the water level in Lake Mead will likely continue to deteriorate, unless more stringent measures are introduced to regulate consumption.

Economic Impact

The drought in the South West affects far more than just the water levels in Lake Mead, of course. One study found that California’s agriculture sector alone had lost $2.2Bn and some 17,00 season and part time jobs in 2014, due to drought. Agriculture uses more than 80% of the State’s water, according to Fortune magazine, which goes on to identify the key industries most affected, including agriculture, food processing, semiconductors, energy, utilities and tourism.

Dry fields and bare trees at Panoche Road, looking west, on Wednesday February 5, 2014, near San Joaquin, CA. California drought has hit the Central Valley hard.

In the energy sector, for example, the loss of hydroelectric power cost CA around $1.4Bn in 2014, according to non-profit research group Pacific Institute. Although Intel pulled its last fabrication plant from California in 2009, semiconductor manufacturing is still a going concern in the state. Maxim Integrated, TowerJazz, and TSI Semiconductors all still have fabrication plants in the state. And they need a lot of water. A single semiconductor fabrication plant can use as much water as a small city. That means the current plants could represent three cities worth of consumption.

The drought is also bad news for water utilities, of course. The need to conserve water raises the priority on repair and maintenance, and that means higher costs and lower profit. Complicating the problem, California lacks any kind of management system for its water supply and can’t measure the inflows and outflows to ground water levels at any particular time.

The Bureau of Reclamation has studied more than two dozen options for conserving and increasing water supply, including importation, desalination and reuse. While some were disregarded for being too costly or difficult, the bureau found that the remaining options, if instituted, could yield 3.7 million acre feet per year in savings and new supplies, increasing to 7 million acre feet per year by 2060. Agriculture is the biggest user by far and has to be part of any solution. In the near term, the agriculture industry could reduce its use by 10 to 15 percent without changing the types of crops it grows by using new technology, such as using drip irrigation instead of flood irrigation and monitoring soil moisture to prevent overwatering, the Pacific Institute found.

Conclusion

We can anticipate that a series of short term fixes, like the “Third Straw”, will be employed to kick the can down the road as far as possible, but research now appears almost unanimous in finding that drought is having a deleterious, long term affect on the economics of the South Western states. Agriculture is likely to have to bear the brunt of the impact, but so too will adverse consequences be felt in industries as disparate as food processing, semiconductors and utilities. California, with the largest agricultural industry, by far, is likely to be hardest hit. The Las Vegas region may be far less vulnerable, having already taken aggressive steps to conserve and reuse water supply and charge economic rents for water usage.

Modeling Water Levels in Lake Mead

The monthly reported water levels in Lake Mead from Feb 1935 to June 2016 are shown in the chart below. The reference line is the drought level, historically defined as 1,125 feet.

One statistical technique widely applied in hydrology involves fitting a Kumaraswamy distribution to the relative water level. According to the Arizona Game and Fish Department, the maximum lake level is 1229 feet. We model the water level relative to the maximum level, as follows.

The fit of the distribution appears quite good, even in the tails:

ProbabilityPlot[relativeLevels, edist]

Since water levels have been below the drought level for some time, let’s instead consider the “emergency” level, 1,075 feet. According to this model, there is just over a 6% chance of Lake Mead hitting the emergency level and, consequently, a high probability of breaching the emergency threshold some time over before the end of 2017.

One problem with this approach is that it assumes that each observation is drawn independently from a random variable with the estimated distribution. In reality, there are high levels of autocorrelation in the series, as might be expected: lower levels last month typically increase the likelihood of lower levels this month. The chart of the autocorrelation coefficients makes this pattern clear, with statistically significant coefficients at lags of up to 36 months.

ts[“ACFPlot”]

An alternative methodology that enables us to take account of the autocorrelation in the process is time series analysis. We proceed to fit an autoregressive moving average (ARMA) model as follows:

tsm = TimeSeriesModelFit[ts, “ARMA”]

The best fitting model in an ARMA(1,1) model, according to the AIC criterion:

Applying the fitted ARMA model, we forecast the water level in Lake Mead over the next ten years as shown in the chart below. Given the mean-reverting moving average component of the model, it is not surprising to see the model forecasting a return to normal levels.

There is some evidence of lack of fit in the ARMA model, as shown in the autocorrelations of the model residuals:

A formal test reveals that residual autocorrelations at lags 4 and higher are jointly statistically significant:

The slowly decaying pattern of autocorrelations in the water level series suggests a possible “long memory” effect, which can be better modelled as a fractionally integrated process. The forecasts from such a model, like the ARMA model forecasts, display a tendency to revert to a long term mean; but the reversion process is dampened by the reinforcing, long-memory effect captured in the FARIMA model.

The Prospects for the Next Decade

Taking the view that the water level in Lake Mead forms a stationary statistical process, the likelihood is that water levels will rise to 1,125 feet or more over the next ten years, easing the current water shortage in the region.

On the other hand, there are good reasons to believe that there are exogenous (deterministic) factors in play, specifically the over-consumption of water at a rate greater than the replenishment rate from average rainfall levels. Added to this, plausible studies suggest that average rainfall in the Colorado Basin is expected to decline over the next fifty years. Under this scenario, the water level in Lake Mead will likely continue to deteriorate, unless more stringent measures are introduced to regulate consumption.

Economic Impact

The drought in the South West affects far more than just the water levels in Lake Mead, of course. One study found that California’s agriculture sector alone had lost $2.2Bn and some 17,00 season and part time jobs in 2014, due to drought. Agriculture uses more than 80% of the State’s water, according to Fortune magazine, which goes on to identify the key industries most affected, including agriculture, food processing, semiconductors, energy, utilities and tourism.

In the energy sector, for example, the loss of hydroelectric power cost CA around $1.4Bn in 2014, according to non-profit research group Pacific Institute.

Although Intel pulled its last fabrication plant from California in 2009, semiconductor manufacturing is still a going concern in the state. Maxim Integrated, TowerJazz, and TSI Semiconductors all still have fabrication plants in the state. And they need a lot of water. A single semiconductor fabrication plant can use as much water as a small city. That means the current plants could represent three cities worth of consumption.

The drought is also bad news for water utilities, of course. The need to conserve water raises the priority on repair and maintenance, and that means higher costs and lower profit. Complicating the problem, California lacks any kind of management system for its water supply and can’t measure the inflows and outflows to ground water levels at any particular time.

The Bureau of Reclamation has studied more than two dozen options for conserving and increasing water supply, including importation, desalination and reuse. While some were disregarded for being too costly or difficult, the bureau found that the remaining options, if instituted, could yield 3.7 million acre feet per year in savings and new supplies, increasing to 7 million acre feet per year by 2060. Agriculture is the biggest user by far and has to be part of any solution. In the near term, the agriculture industry could reduce its use by 10 to 15 percent without changing the types of crops it grows by using new technology, such as using drip irrigation instead of flood irrigation and monitoring soil moisture to prevent overwatering, the Pacific Institute found.

Conclusion

We can anticipate that a series of short term fixes, like the “Third Straw”, will be employed to kick the can down the road as far as possible, but research now appears almost unanimous in finding that drought is having a deleterious, long term affect on the economics of the South Western states. Agriculture is likely to have to bear the brunt of the impact, but so too will adverse consequences be felt in industries as disparate as food processing, semiconductors and utilities. California, with the largest agricultural industry, by far, is likely to be hardest hit. The Las Vegas region may be far less vulnerable, having already taken aggressive steps to conserve and reuse water supply and charge economic rents for water usage.

{kind=link}