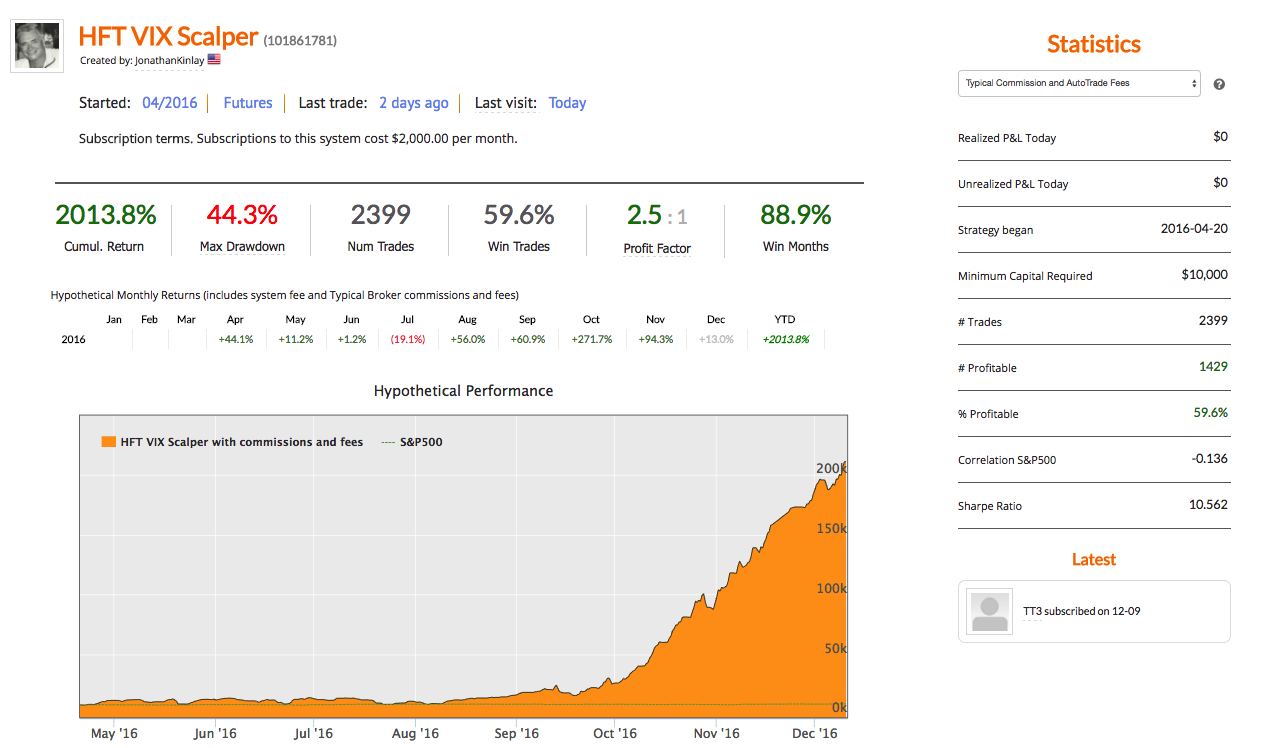

Our high frequency VIX scalping strategy is now the #1 top performing strategy on Collective2, with returns of over 2700% since April 2016 with a Sharpe Ratio above 10 and Profit Factor of 2.8.

For more background on HFT scalping strategies see the following post:

http://jonathankinlay.com/2014/05/the-mathematics-of-scalping/