The Importance of Sample Frequency

Too often we apply a default time horizon for our trading, whether it below (daily, weekly) or higher (hourly, 5 minute) frequency. Sometimes the choice is dictated by practical considerations, such as a desire to avoid overnight risk, or the (lack of0 availability of low-latency execution platform.

But there is an alternative approach to the trade frequency decision that often yields superior results in terms of trading performance. The methodology derives from signal processing and the idea essentially is to use Fourier transforms to help identify the cyclical behavior of the strategy alpha and hence determine the best time-frames for sampling and trading. I wrote about this is a previous blog post, in which I described how to use principal components analysis to investigate the factors driving the returns in various pairs trading strategies. Here I want to take a simpler approach, in which we use Fourier analysis to select suitable sample frequencies. The idea is simply to select sample frequencies where the signal strength appears strongest, in the hope that it will lead to superior performance characteristics in what strategy we are trying to develop.

Signal Decomposition for S&P500 eMini Futures

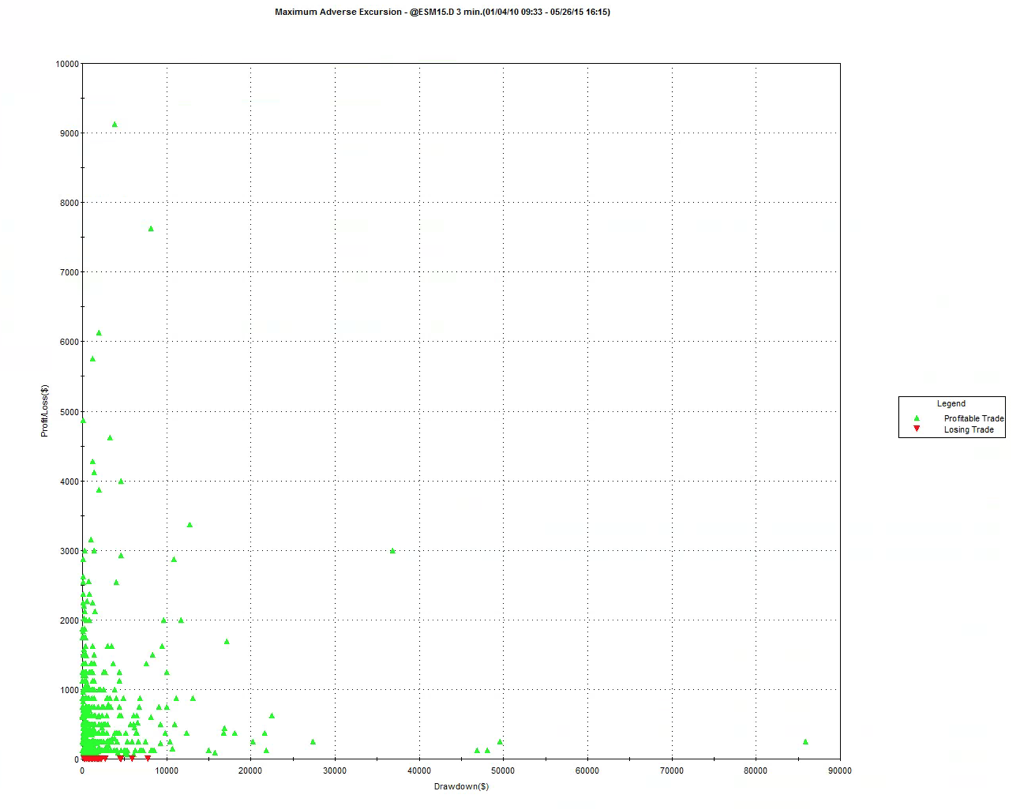

Let’s take as an example the S&P 500 emini futures contract. The chart below shows the continuous ES futures contract plotted at 1-minute intervals from 1998. At the bottom of the chart I have represented the signal analysis as a bar chart (in blue), with each bar representing the amplitude at each frequency. The white dots on the chart identify frequencies that are spaced 10 minutes apart. It is immediately evident that local maxima in the spectrum occur around 40 mins, 60 mins and 120 mins. So a starting point for our strategy research might be to look at emini data sampled at these frequencies. Incidentally, it is worth pointing out that I have restricted the session times to 7AM – 4PM EST, which is where the bulk of the daily volume and liquidity tend to occur. You may get different results if you include data from the Globex session.

This is all very intuitive and unsurprising: the clearest signals occur at frequencies that most traders typically tend to trade, using hourly data, for example. Any strategy developer is already quite likely to consider these and other common frequencies as part of their regular research process. There are many instances of successful trading strategies built on emini data sampled at 60 minute intervals.

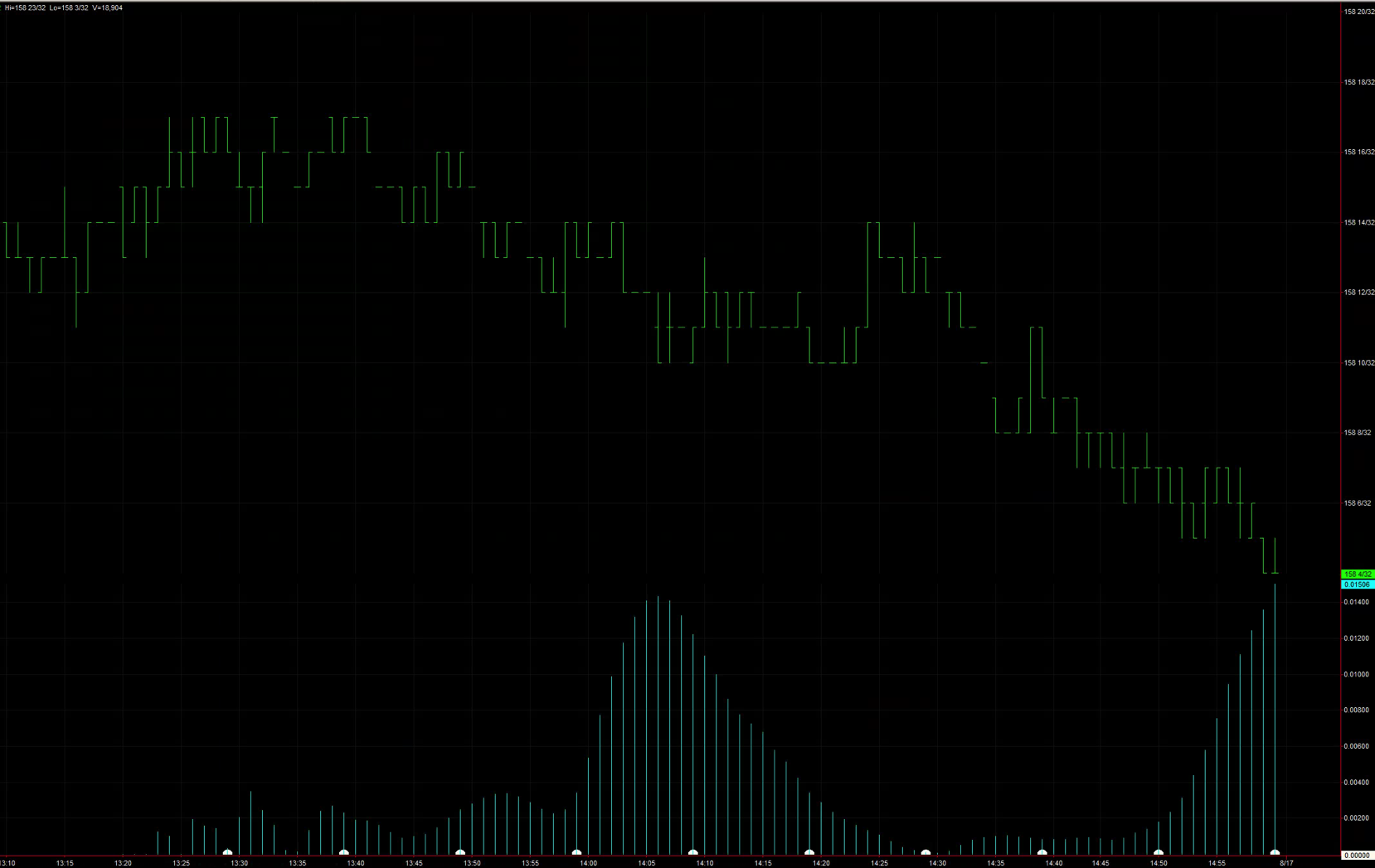

Signal Decomposition for US Bond Futures

Let’s look at a rather more interesting example: US (30 year) Bond futures. Unlike the emini contract, the spectral analysis of the US futures contract indicates that the strongest signal by far occurs at a frequency of around 47 minutes. This is decidedly an unintuitive outcome – I can’t think of any reason why such a strong signal should appear at this cycle length, but, statistically it does.

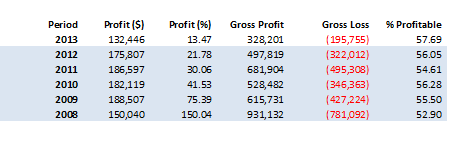

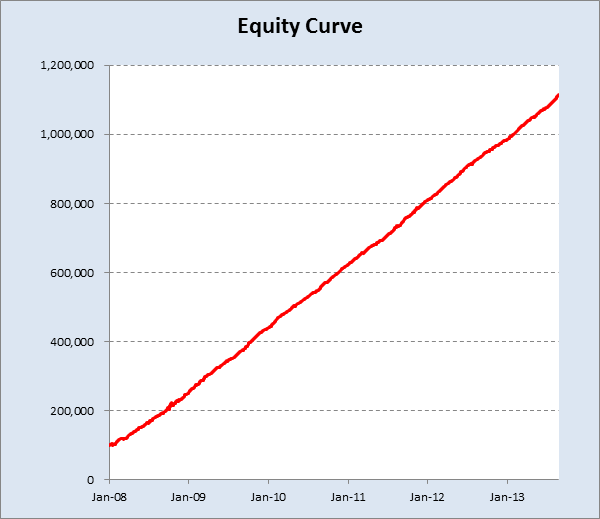

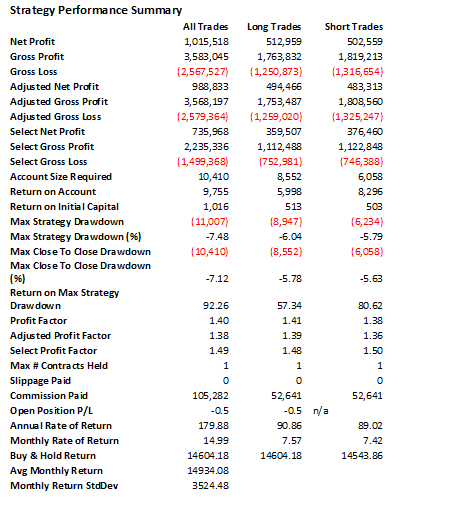

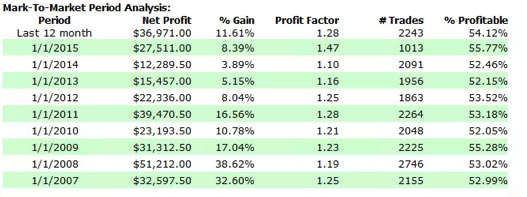

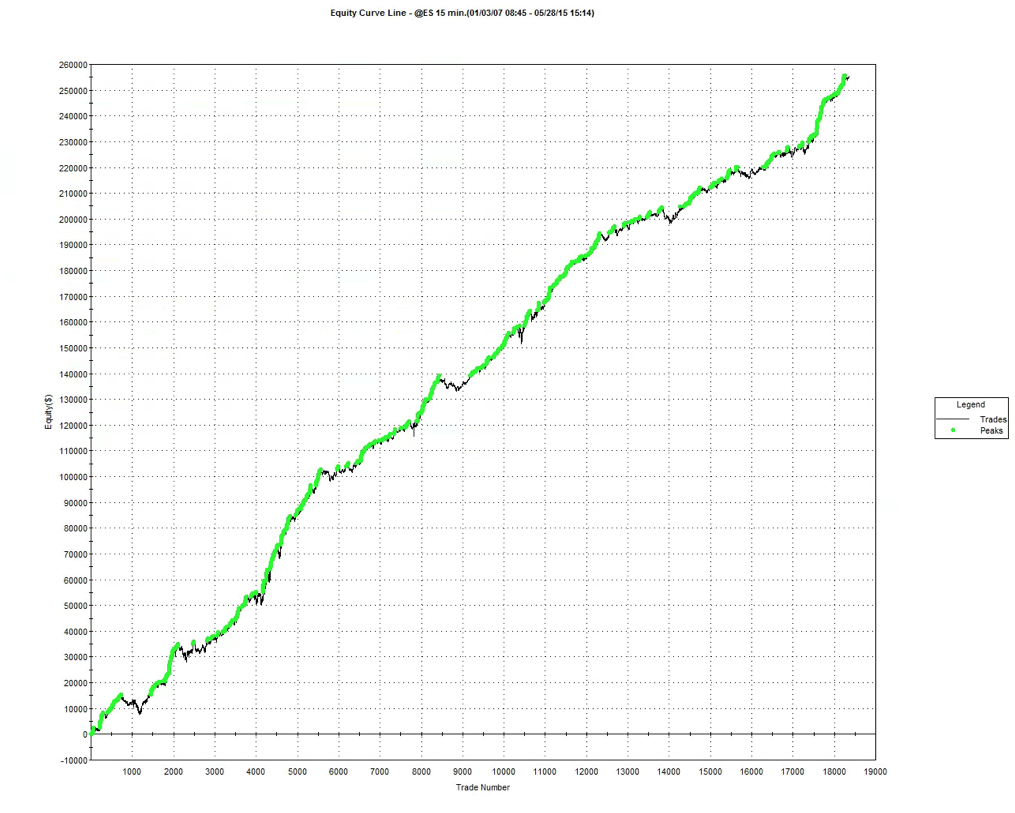

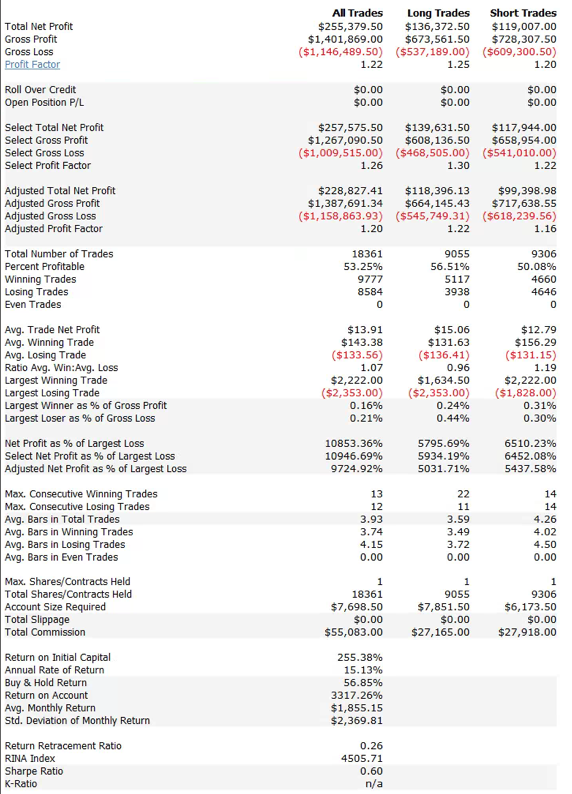

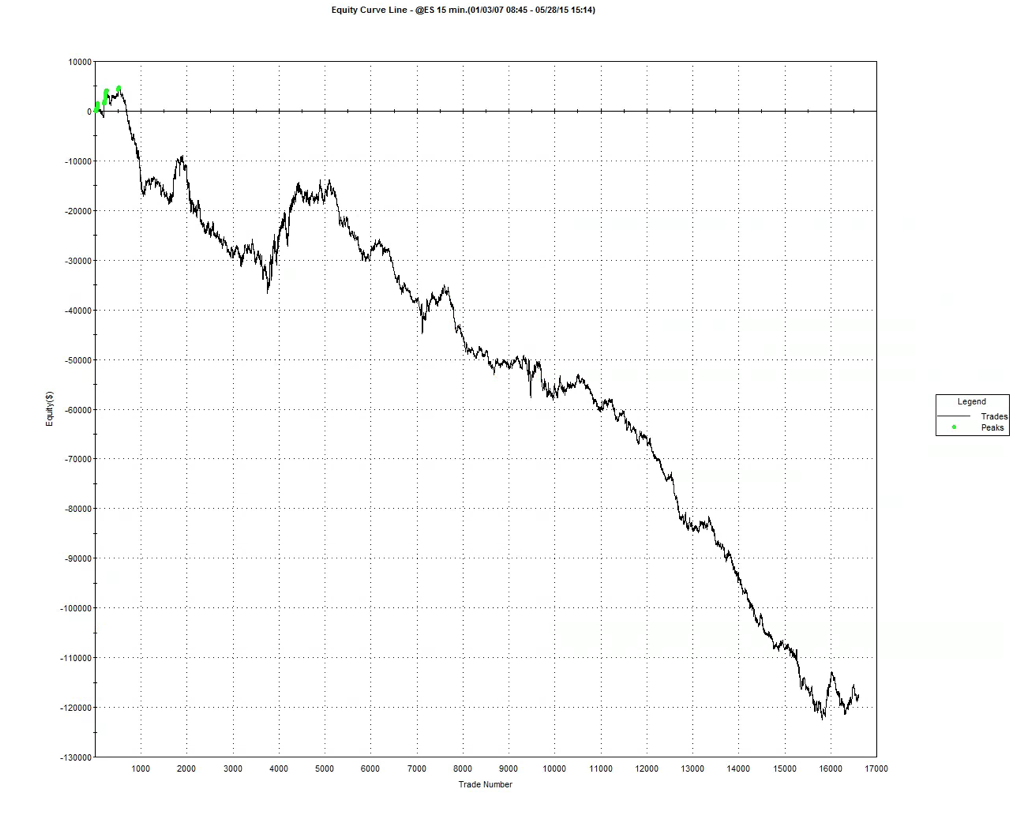

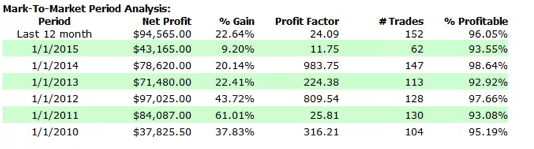

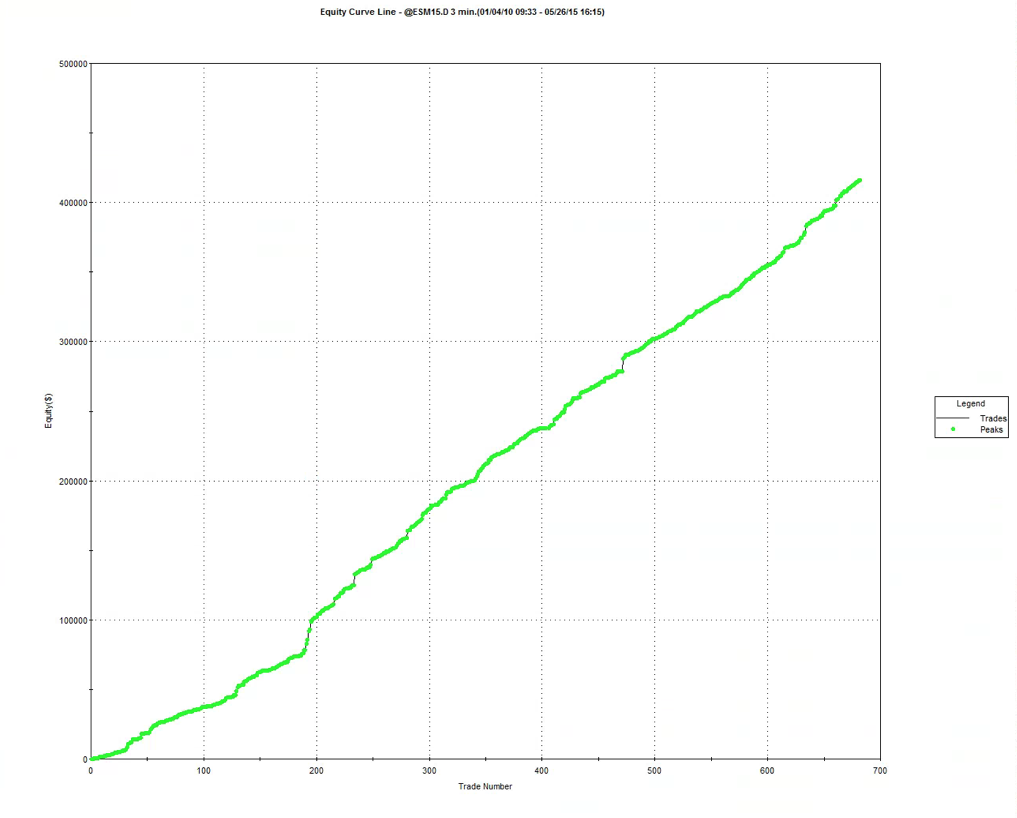

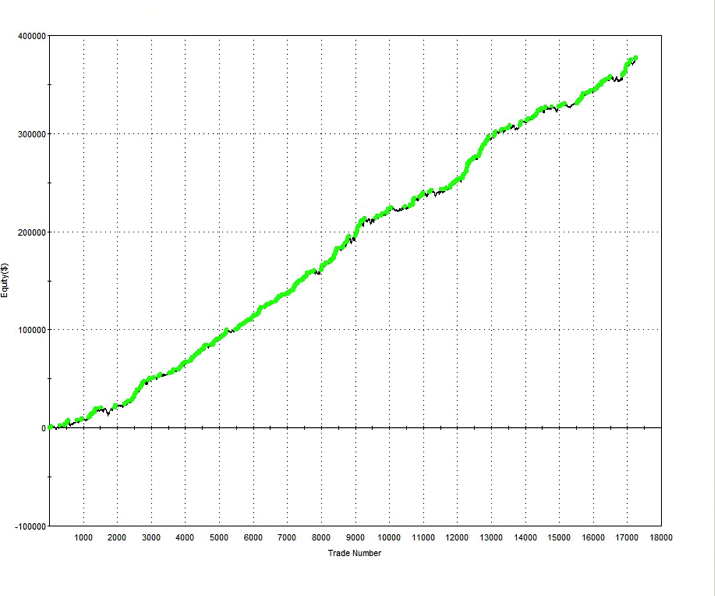

Does it work? Readers can judge for themselves: below is an example of an equity curve for a strategy on US futures sampled at 47 minute frequency over the period from 2002. The strategy has performed very consistently, producing around $25,000 per contract per year, after commissions and slippage.

Conclusion

While I have had similar success with products as diverse as Corn and VIX futures, the frequency domain approach is by no means a panacea: there are plenty of examples where I have been unable to construct profitable strategies for data sampled at the frequencies with very strong signals. Conversely, I have developed successful strategies using data at frequencies that hardly registered at all on the spectrum, but which I selected for other reasons. Nonetheless, spectral analysis (and signal processing in general) can be recommended as a useful tool in the arsenal of any quantitative analyst.