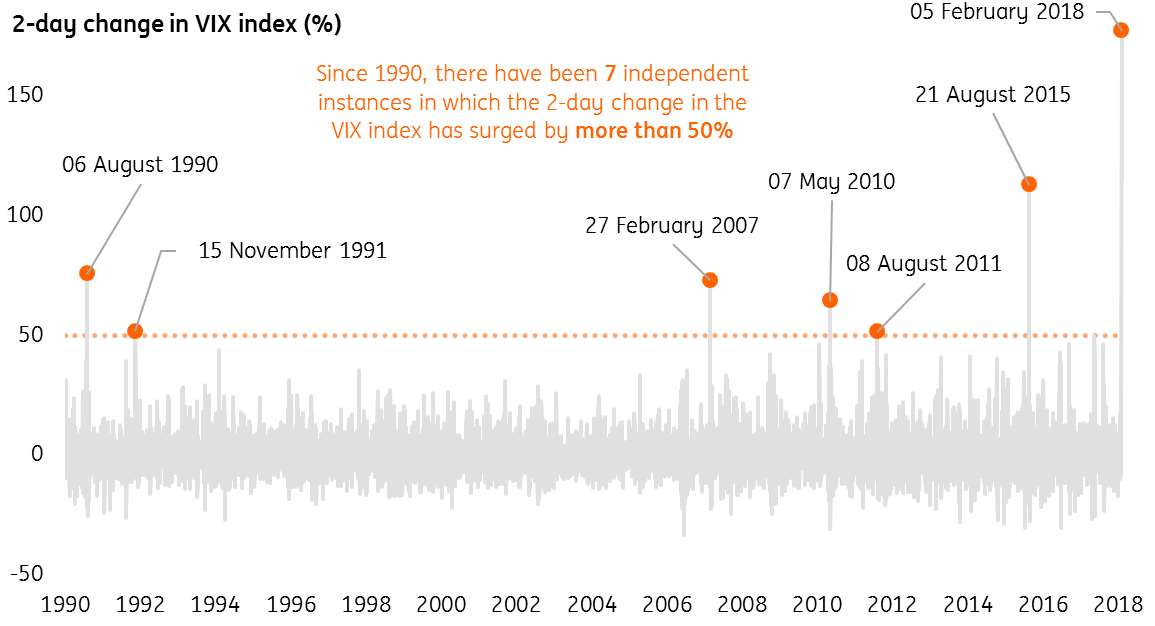

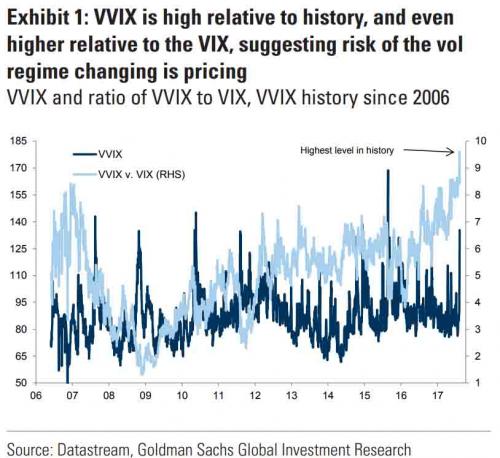

The VIX Surge of Feb 2018

Volatility trading has become a popular niche in investing circles over the last several years. It is easy to understand why: with yields at record lows it has been challenging to find an alternative to equities that offers a respectable return. Volatility, however, continues to be volatile (which is a good thing in this context) and the steepness of the volatility curve has offered investors attractive returns by means of the volatility carry trade. In this type of volatility trading the long end of the vol curve is sold, often using longer dated futures in the CBOE VIX Index, for example. The idea is that profits are generated as the contract moves towards expiration, “riding down” the volatility curve as it does so. This is a variant of the ever-popular “riding down the yield curve” strategy, a staple of fixed income traders for many decades. The only question here is what to use to hedge the short volatility exposure – highly correlated S&P500 futures are a popular choice, but the resulting portfolio is exposed to significant basis risk. Besides, when the volatility curve flatten and inverts, as it did in spectacular fashion in February, the transition tends to happen very quickly, producing a substantial losses on the portfolio. These may be temporary, if the volatility spike is small or short-lived, but as traders and investors discovered in the February drama, neither of these two desirable outcomes is guaranteed. Indeed as I pointed out in an earlier post this turned out to be the largest ever two-day volatility surge in history. The results for many hedge funds, especially in the quant sector were devastating, with several showing high single digit or double-digit losses for the month.

Over time, investors have become more familiar with the volatility space and have learned to be wary of strategies like volatility carry or option selling, where the returns look superficially attractive, until a market event occurs. So what alternative approaches are available?

An Aggressive Approach to Volatility Trading

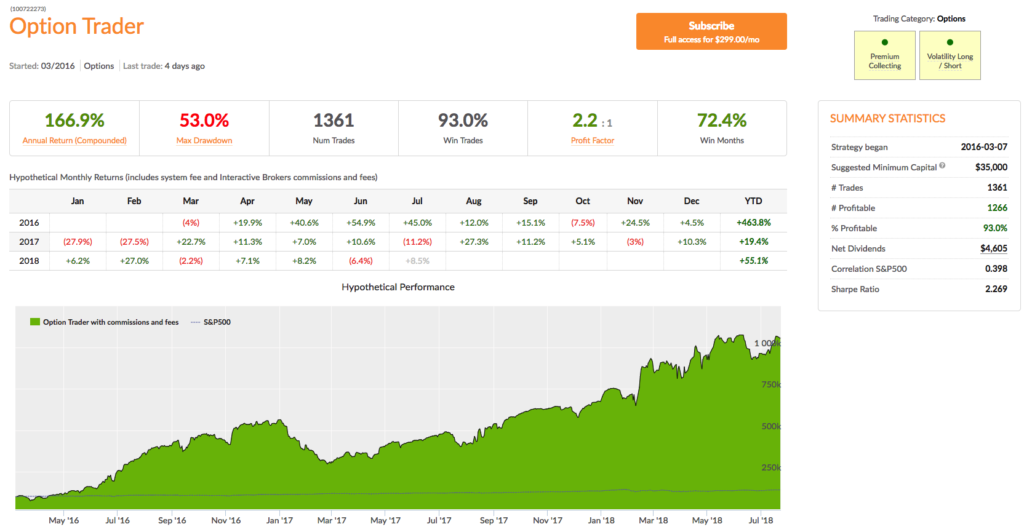

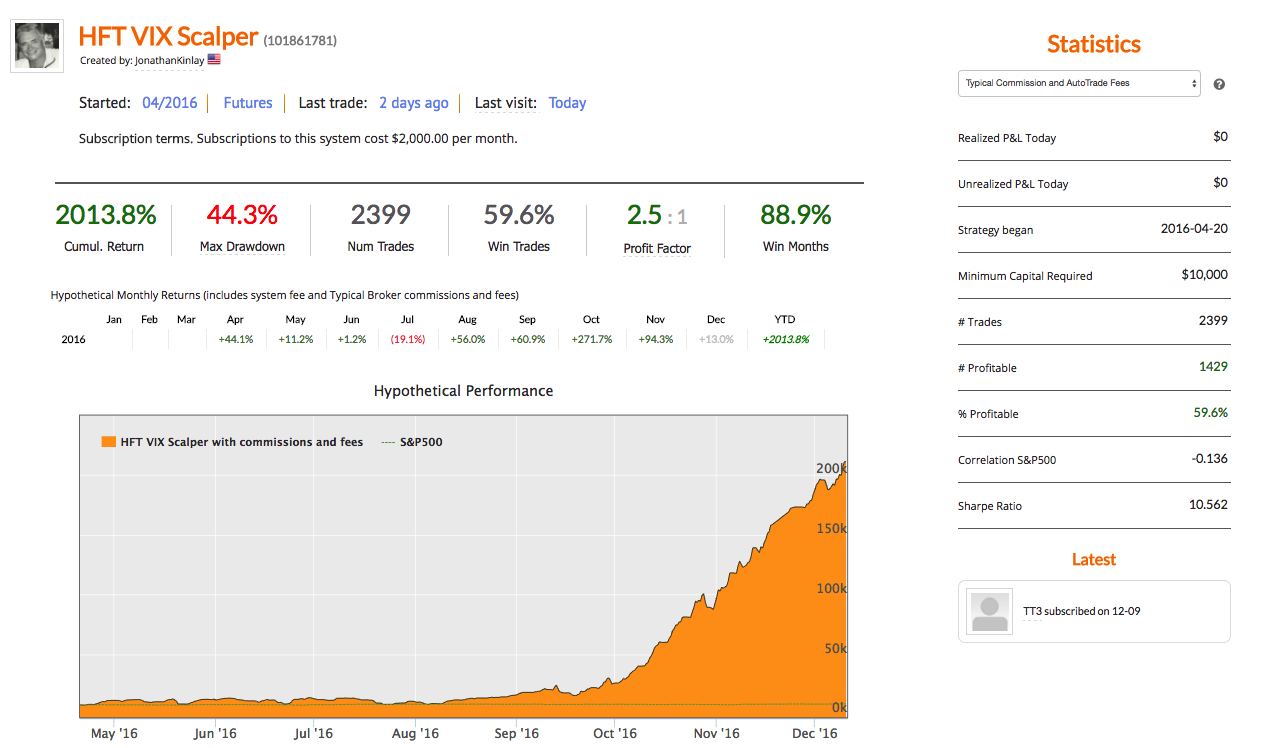

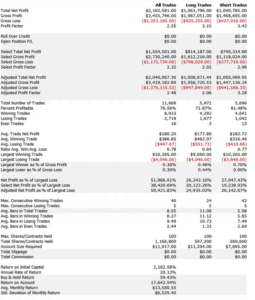

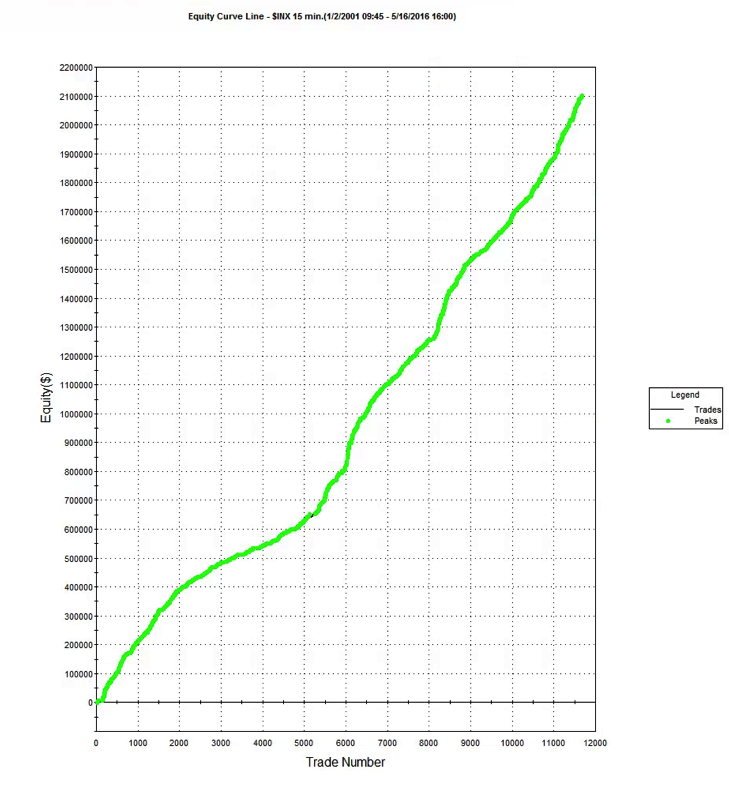

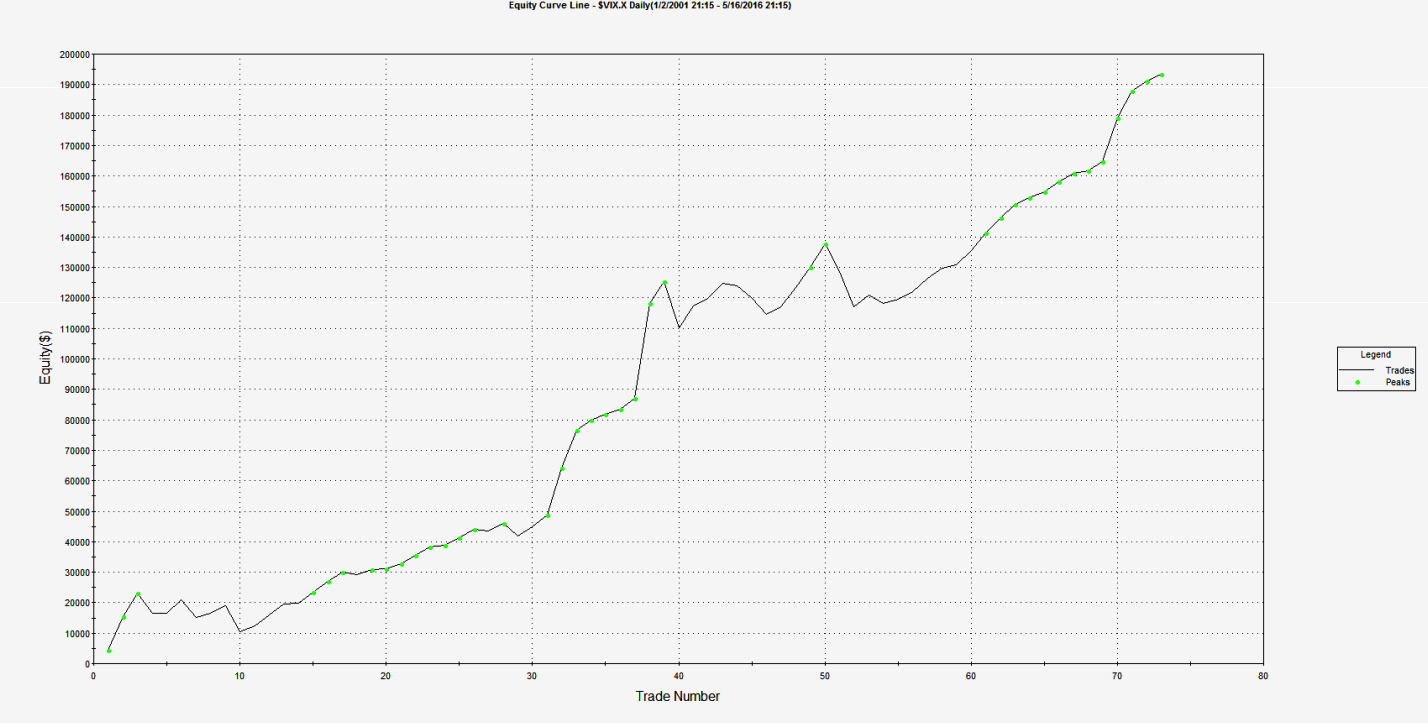

In my blog post Riders on the Storm I described one such approach: the Option Trader strategy on our Algo Trading Platform made a massive gain of 27% for the month of February and as a result strategy performance is now running at over 55% for 2018 YTD, while maintaining a Sharpe Ratio of 2.23.

The challenge with this style of volatility trading is that it requires a trader (or trading system) with a very strong stomach and an investor astute enough to realize that sizable drawdowns are in a sense “baked in” for this trading strategy and should be expected from time to time. But traders are often temperamentally unsuited to this style of trading – many react by heading for the hills and liquidating positions at the first sign of trouble; and the great majority of investors are likewise unable to withstand substantial drawdowns, even if the eventual outcome is beneficial.

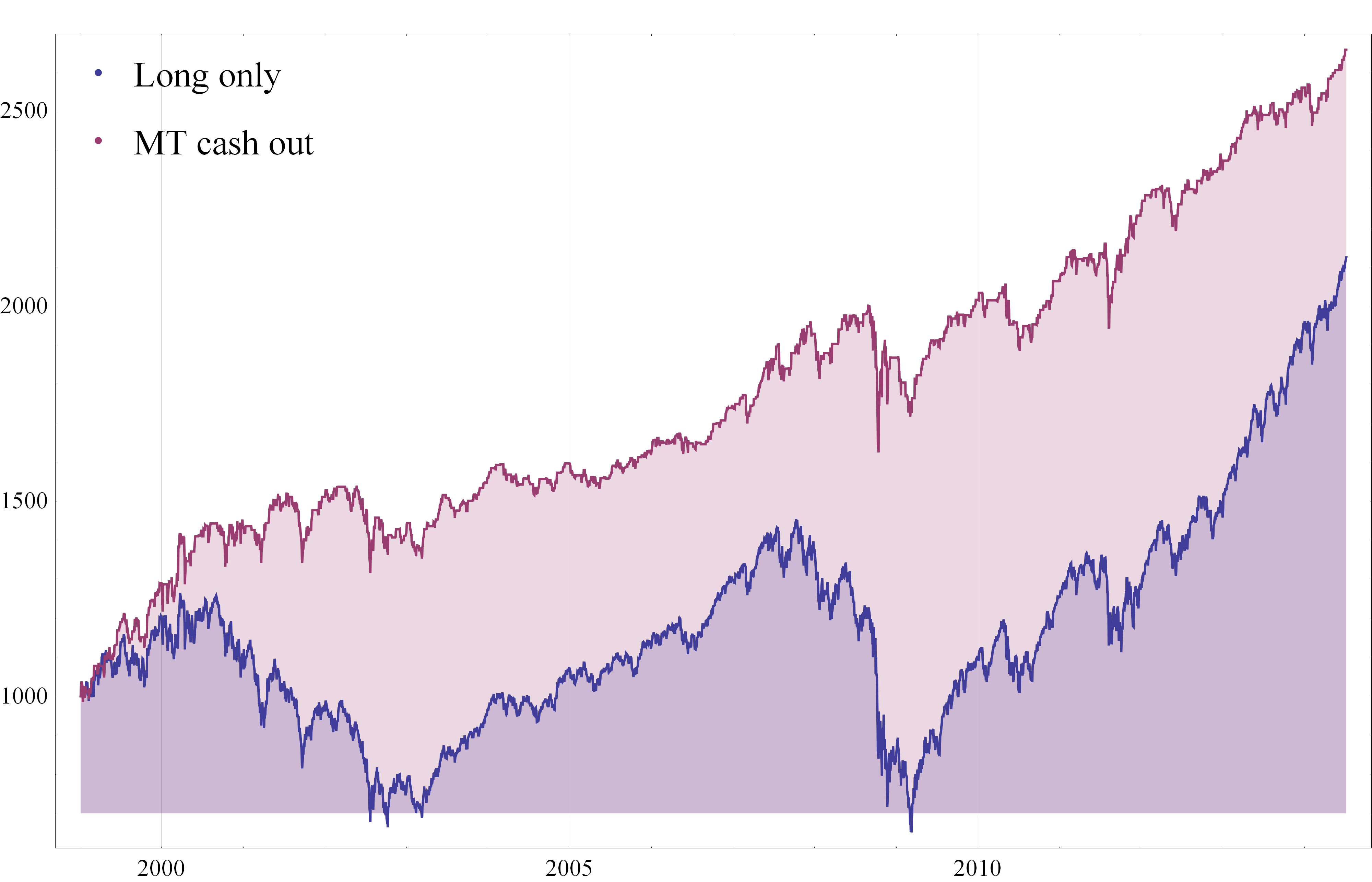

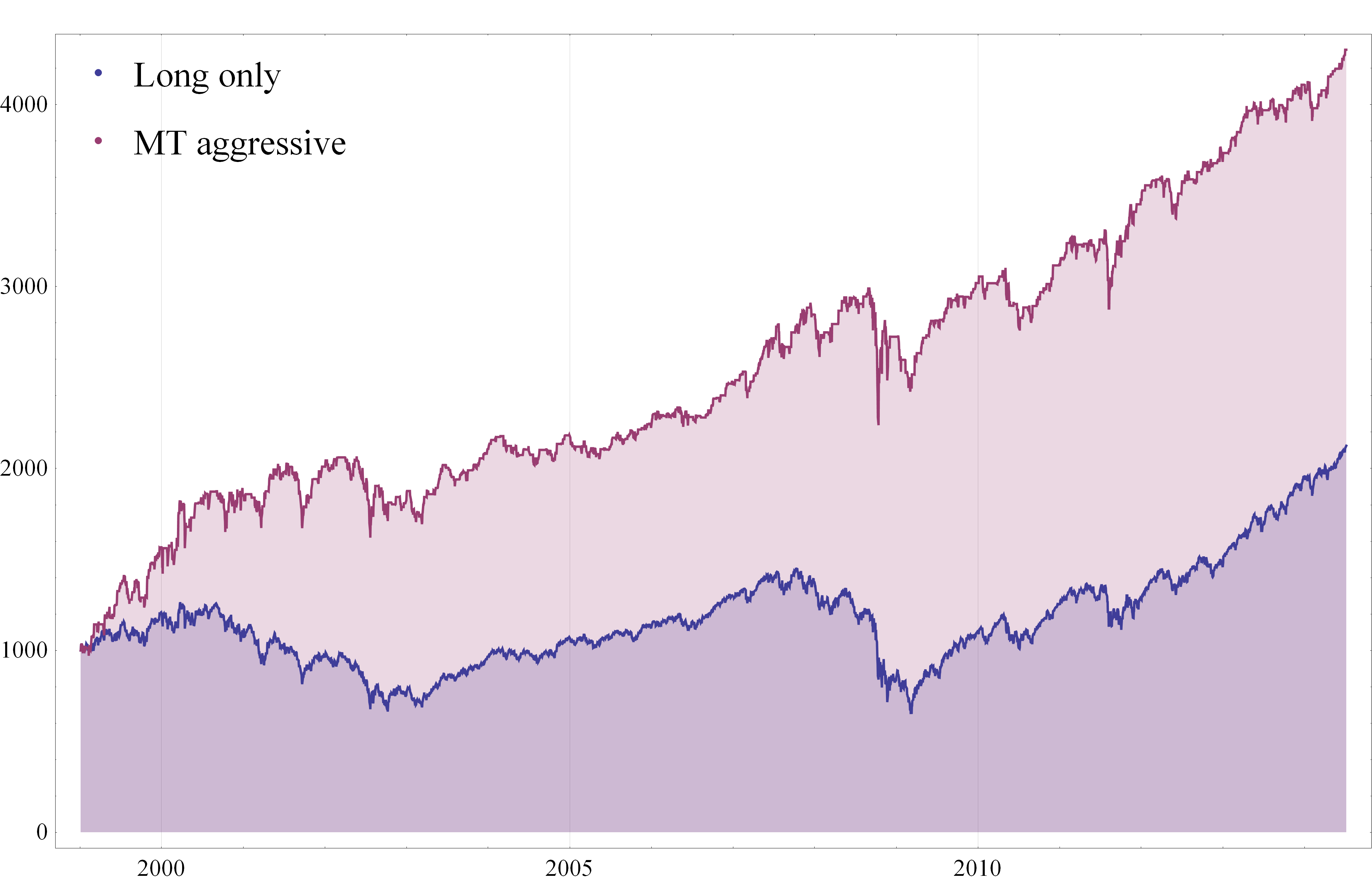

The Market Timing Approach

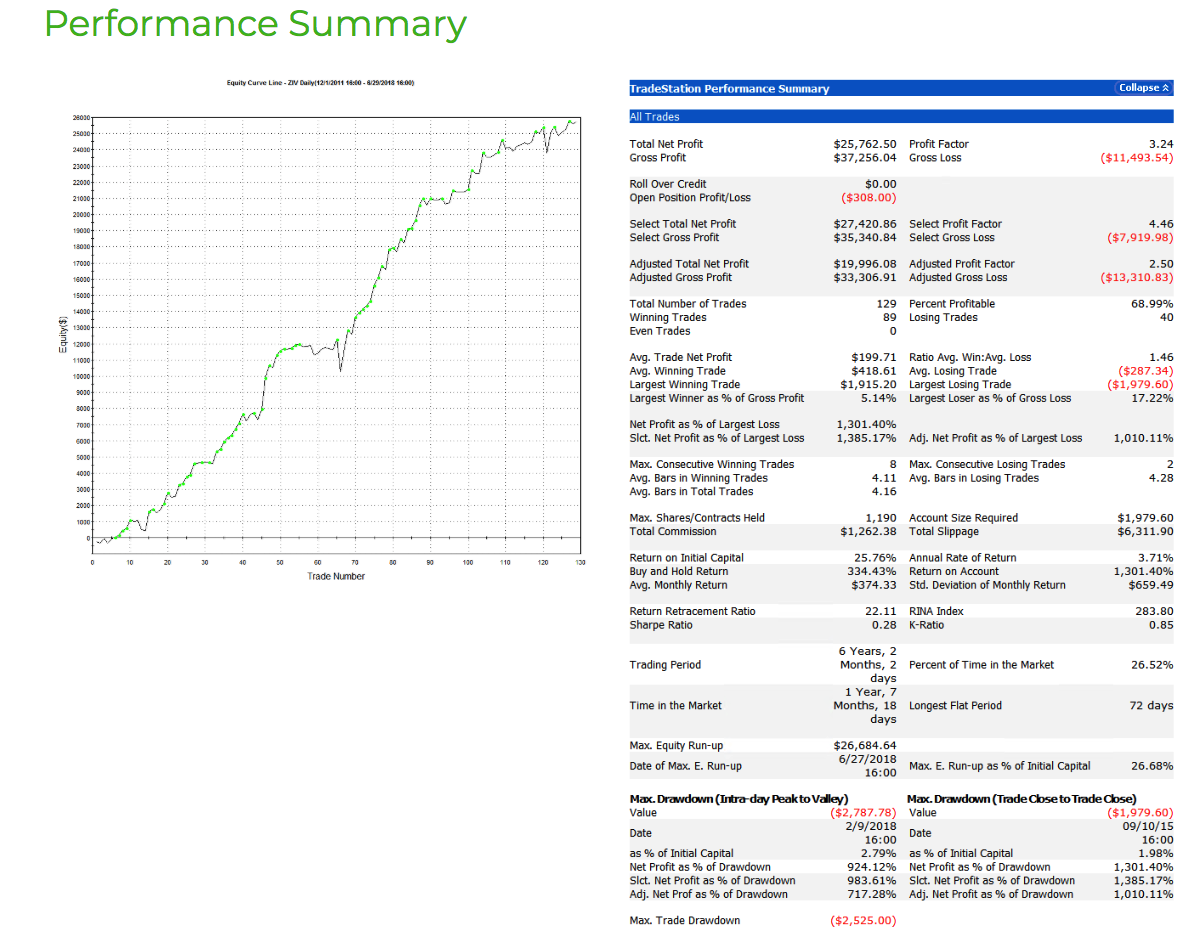

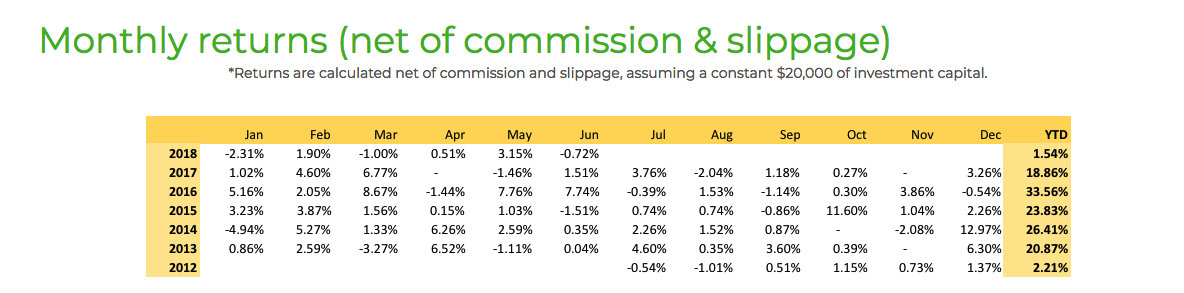

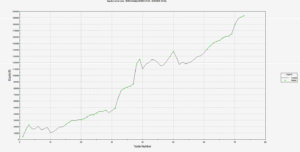

So what alternatives are there? One way of dealing with the problem of volatility spikes is simply to try to avoid them. That means developing a strategy logic that step aside altogether when there is a serious risk of an impending volatility surge. Market timing is easy to describe, but very hard to implement successfully in practice. The VIX Swing Trader strategy on the Systematic Algotrading platform attempts to do just that, only trading when it judges it safe to do so. So, for example, it completely side-stepped the volatility debacle in August 2015, ending the month up +0.74%. The strategy managed to do the same in February this year, finishing ahead +1.90%, a pretty creditable performance given how volatility funds performed in general. One helpful characteristic of the strategy is that it trades the less-volatile mid-section of the volatility curve, in the form of the VelocityShares Daily Inverse VIX MT ETN (ZIV). This ensures that the P&L swings are much less dramatic than for strategies exposed to the front end of the curve, as most volatility strategies are.

A potential weakness of the strategy is that it will often miss great profit opportunities altogether, since its primary focus is to keep investors out of trouble. Allied to this, the system may trade only a handful of times each month. Indeed, if you look at the track record above you find find months in which the strategy made no trades at all. From experience, investors are almost as bad at sitting on their hands as they are at taking losses: patience is not a highly regarded virtue in the investing community these days. But if you are a cautious, patient investor looking for a source of uncorrelated alpha, this strategy may be a good choice. On the other hand, if you are looking for high returns and are willing to take the associated risks, there are choices better suited to your goals.

The Hedging Approach to Volatility Trading

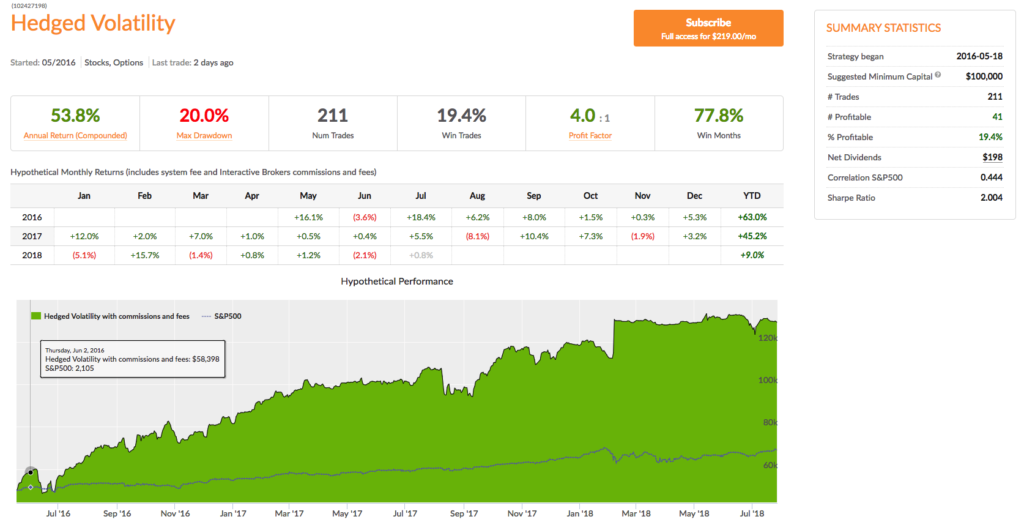

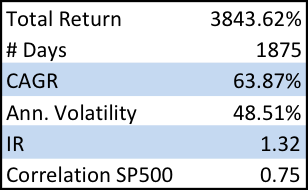

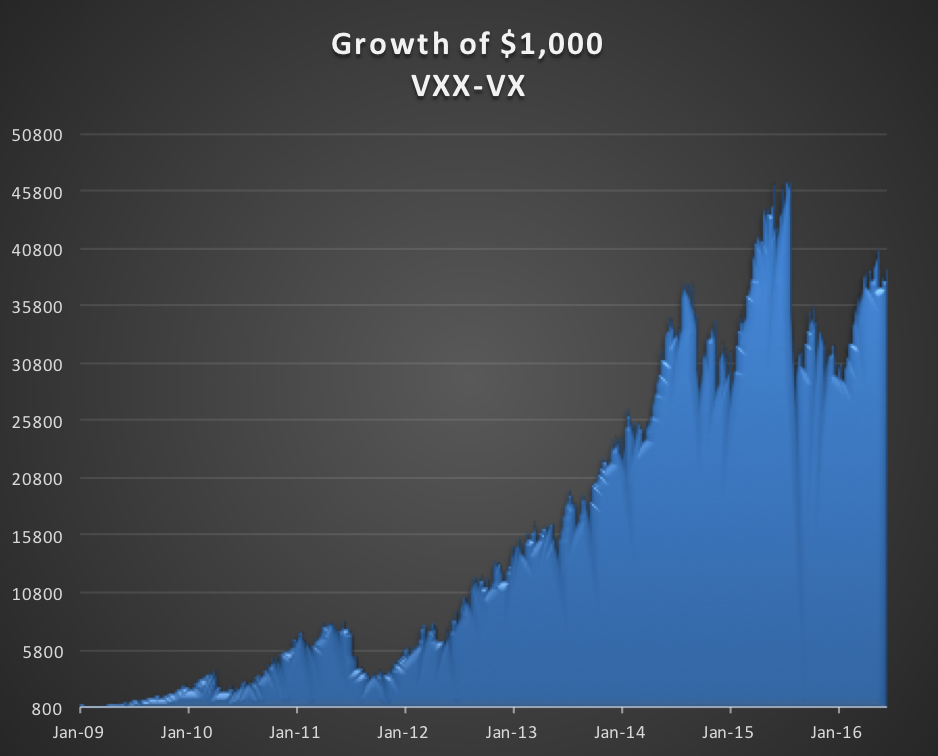

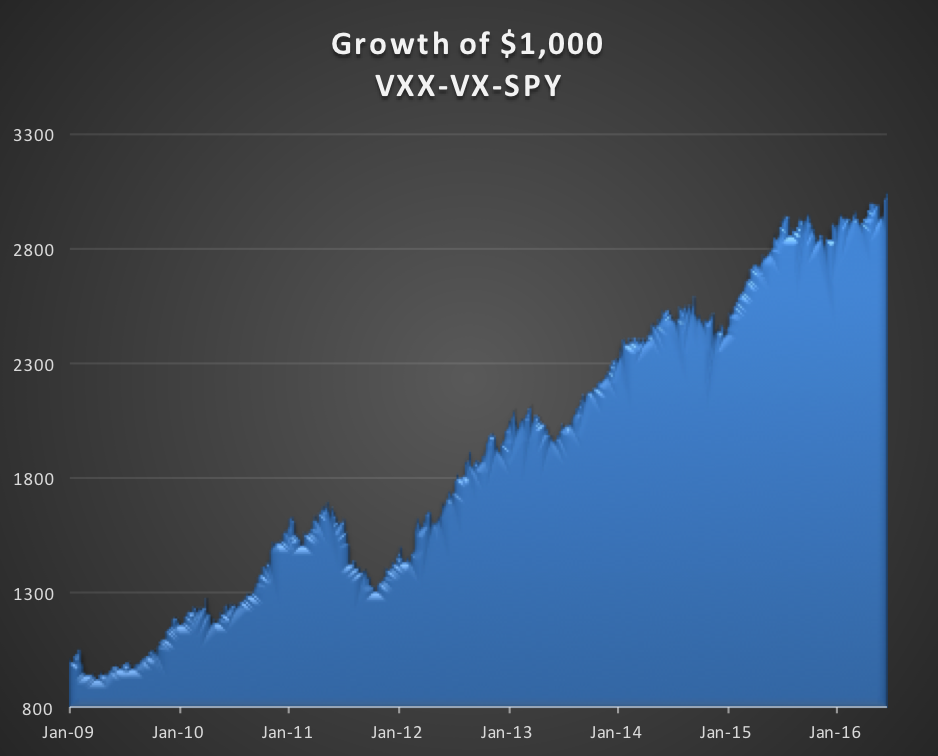

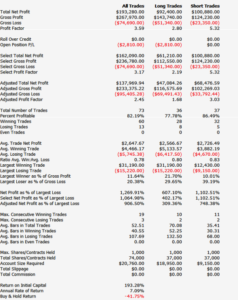

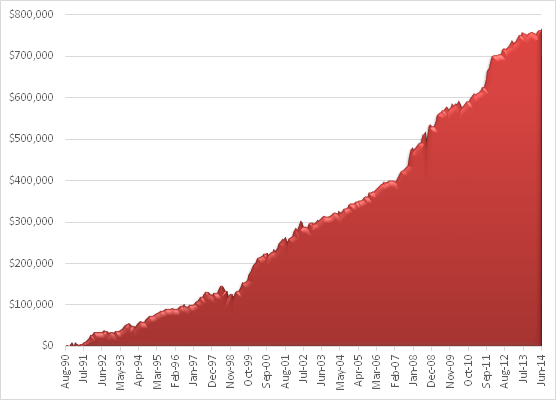

A “middle ground” is taken in our Hedged Volatility strategy. Like the VIX Swing Trader this strategy trades VIX ETFs/ETNs, but it does so across the maturity table. What distinguishes this strategy from the others is its use of long call options in volatility products like the iPath S&P 500 VIX ST Futures ETN (VXX) to hedge the short volatility exposure in other ETFs in the portfolio. This enables the strategy to trade much more frequently, across a wider range of ETF products and maturities, with the security of knowing that the tail risk in the portfolio is protected. Consequently, since live trading began in 2016, the strategy has chalked up returns of over 53% per year, with a Sharpe Ratio of 2 and Sortino Ratio above 3. Don’t be confused by the low % of trades that are profitable: the great majority of these loss-making “trades” are in fact hedges, which one would expect to be losers, as most long options trades are. What matters is the overall performance of the strategy.

All of these strategies are available on our Systematic Algotrading Platform, which offers investors the opportunity to trade the strategies in their own brokerage account for a monthly subscription fee.

The Multi-Strategy Approach

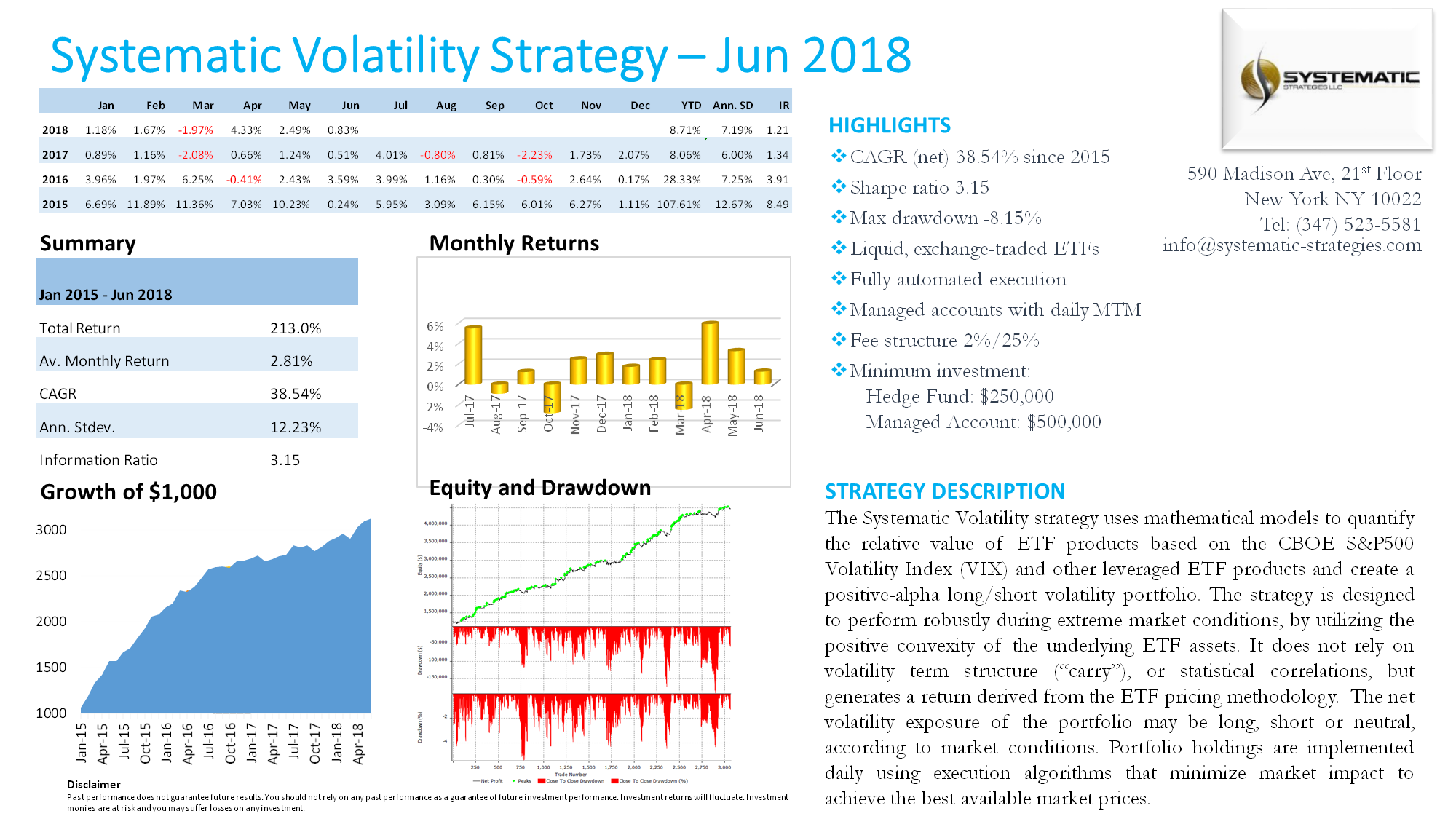

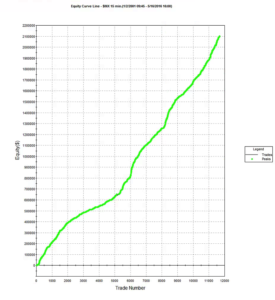

The approach taken by the Systematic Volatility Strategy in our Systematic Strategies hedge fund again seeks to steer a middle course between risk and return. It does so by using a meta-strategy approach that dynamically adjusts the style of strategy deployed as market conditions change. Rather than using options (the strategy’s mandate includes only ETFs) the strategy uses leveraged ETFs to provide tail risk protection in the portfolio. The strategy has produced an average annual compound return of 38.54% since live trading began in 2015, with a Sharpe Ratio of 3.15:

A more detailed explanation of how leveraged ETFs can be used in volatility trading strategies is given in an earlier post:

http://jonathankinlay.com/2015/05/investing-leveraged-etfs-theory-practice/

Conclusion: Choosing the Investment Style that’s Right for You

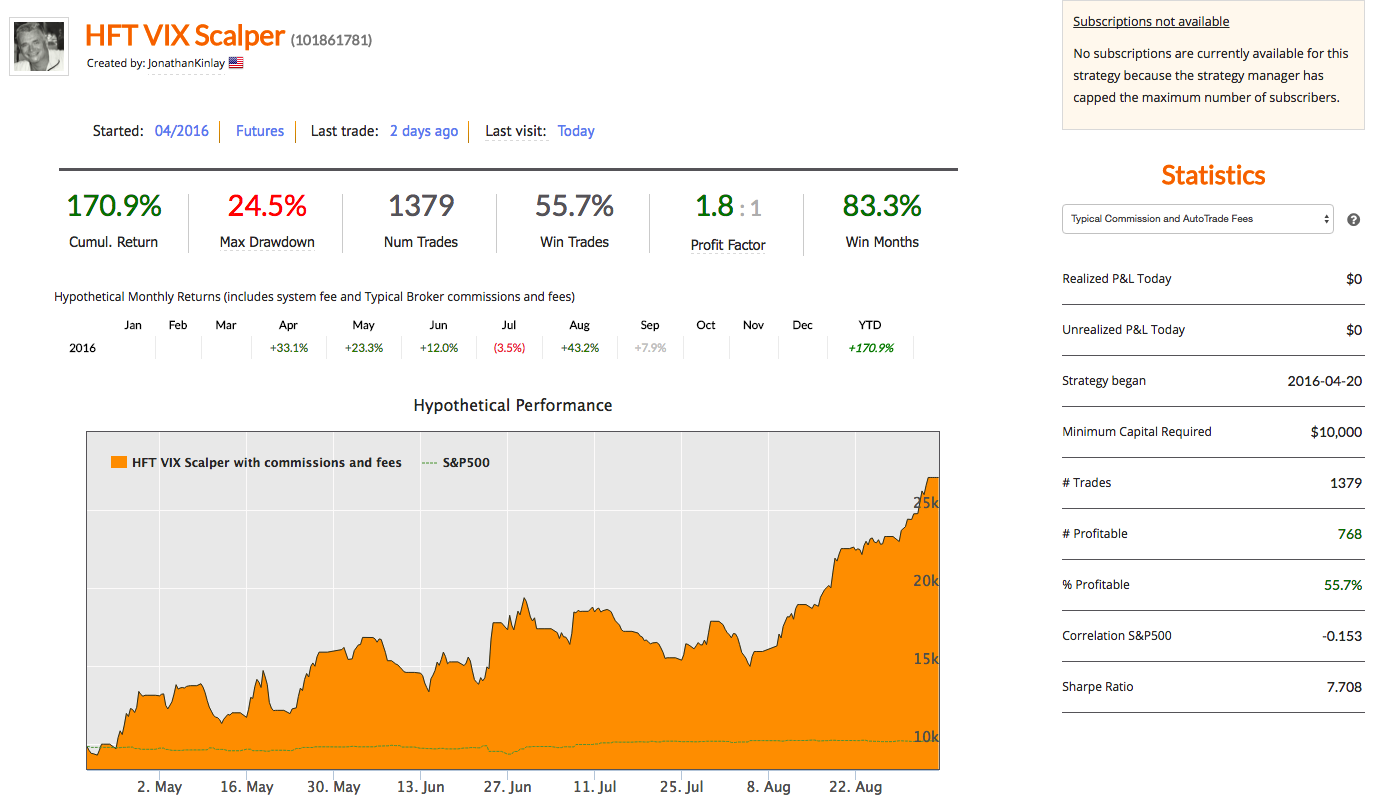

There are different styles of volatility trading and the investor should consider carefully which best suits his own investment temperament. For the “high risk” investor seeking the greatest profit the Option Trader strategy in an excellent choice, producing returns of +176% per year since live trading began in 2016. At the other end of the spectrum, the VIX Swing trader is suitable for an investor with a cautious trading style, who is willing to wait for the right opportunities, i.e. ones that are most likely to be profitable. For investors seeking to capitalize on opportunities in the volatility space, but who are concerned about the tail risk arising from major market corrections, the Hedge Volatility strategy offers a better choice. Finally, for investors able to invest $250,000 or more, a hedge fund investment in our Systematic Volatility strategy offers the highest risk-adjusted rate of return.

{kind=link}

{kind=link}

{kind=link}