Regular readers will recall my mentioning out VIX Futures scalping strategy which we ran on the Collective2 site for a while:

The strategy, while performing very well, proved difficult for subscribers to implement, given the latencies involved in routing orders via the Collective 2 web site. So we began thinking about slower strategies that investors could follow more easily, placing less reliance on the fill rate for limit orders.

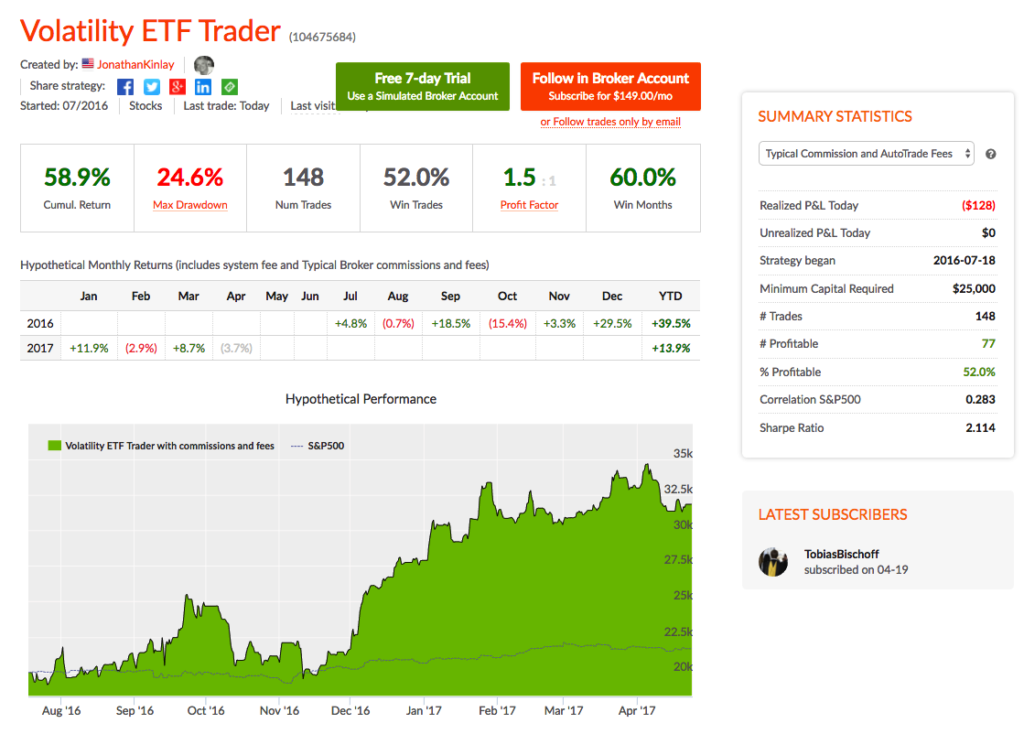

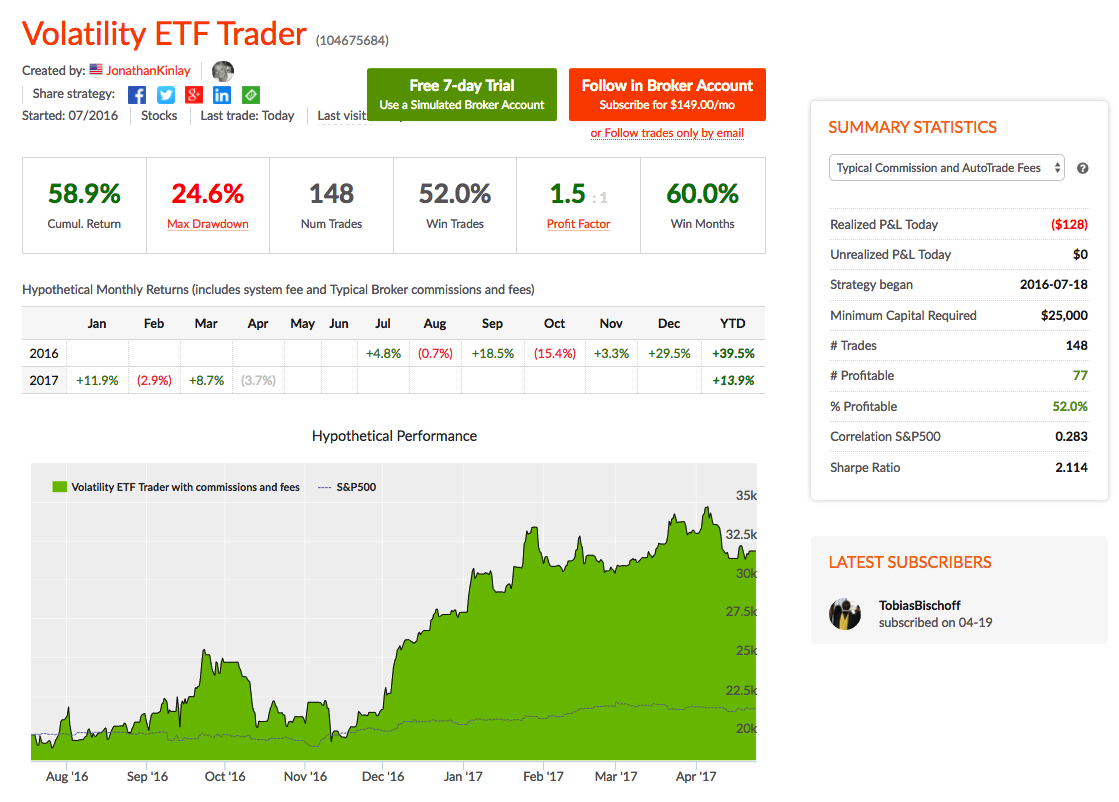

Our VIX ETF Trader strategy has been running on Collective 2 for several months now and is being traded successfully by several subscribers. The performance so far has been quite good, with net returns of 58.9% from July 2016 and a Sharpe ratio over 2, which is not at all bad for a low frequency strategy. The strategy enters and exits using a mix of limit and stop orders, so although some slippage is incurred the trade entries and exits work much more smoothly overall.

Having let the strategy settle for several months trading only the ProShares Short VIX Short-Term Futures ETF (SVXY)we are now ready to ramp things up. From today the strategy will also trade several other VIX ETF products including the VelocityShares Daily Inverse VIX ST ETN (XIV), ProShares Ultra VIX Short-Term Futures (UVXY) and VelocityShares Daily 2x VIX ST ETN (TVIX). All of the trades in these products are entered and exited using market or stop orders, and so will be easy for subscribers to follow. For now we are keeping the required account size pegged at $25,000 although we will review that going forward. My guess is that a capital allocation should be more than sufficient to trade the product in the kind of size we use on the Collective 2 versions of the strategies, especially if the account uses portfolio margin rather than standard Reg-T.

With the addition of the new products to the portfolio mix, we anticipate the strategy Sharpe ratio with rise to over 3 in the year ahead.

The advantage of using a site like Collective 2 from the investor’s viewpoint is that, firstly, you get to see a lot of different trading styles and investment strategies. You can select the strategies in a wide range of asset classes that fit your own investment preferences and trade several of them live in your own brokerage account. (Setting up your account for live trading is straightforward, as described on the C2 site). A major advantage of investing this way is that it doesn’t entail the commitment of capital that is typically required for a hedge fund or managed account investment: you can trade the strategies in much smaller size, to fit your budget.

From our perspective, we find it a useful way to showcase some of the strategies we trade in our hedge fund, so that if investors want to they can move up to more advanced, but similar investment products. We plan to launch new strategies on Collective 2 in the near futures , including an equity portfolio strategy and a CTA futures strategy.

If you would like more information, contact us for further details.

{kind=link}