In earlier posts I have described the idea of a meta-strategy as a strategies that trades strategies. It is an algorithm, or set of rules, that is used to decide when to trade an underlying strategy. In some cases a meta-strategy may influence the size in which the underlying strategy is traded, or may even amend the base code. In other word, a meta-strategy actively “trades” an underlying strategy, or group of strategies, much as in the same way a regular strategy may actively trade stocks, going long or short from time to time. One distinction is that a meta-strategy will rarely, if ever, actually “short” an underlying strategy – at most it will simply turn the strategy off (reduce the position size to zero) for a period.

For a more detailed description, see this post:

In this post I look at a meta-strategy that developed for a client’s strategy in S&P E-Mini futures. What is extraordinary is that the underlying strategy was so badly designed (not by me!) and performs so poorly that no rational systematic trader would likely give it a second look – instead he would toss it into the large heap of failed ideas that all quantitative researchers accumulate over the course of their careers. So this is a textbook example that illustrates the power of meta-strategies to improve, or in this case transform, the performance of an underlying strategy.

1. The Strategy

The Target Trader Strategy (“TTS”) is a futures strategy applied to S&P 500 E-Mini futures that produces a very high win rate, but which occasionally experiences very large losses. The purpose of the analysis if to find methods that will:

1) Decrease the max loss / drawdown

2) Increase the win rate / profitability

For longs the standard setting is entry 40 ticks below the target, stop loss 1000 ticks below the target, and then 2 re-entries 100 ticks below entry 1 and 100 ticks below entry 2

For shorts the standard is entry 80 ticks above the target. stop loss 1000 ticks above the target, and then 2 re-entries 100 ticks above entry 1 and 100 ticks above entry 2

For both directions its 80 ticks above/below for entry 1, 1000 tick stop, and then 1 re entry 100 ticks above/below, and then re-entry 2 100 ticks above/below entry 2

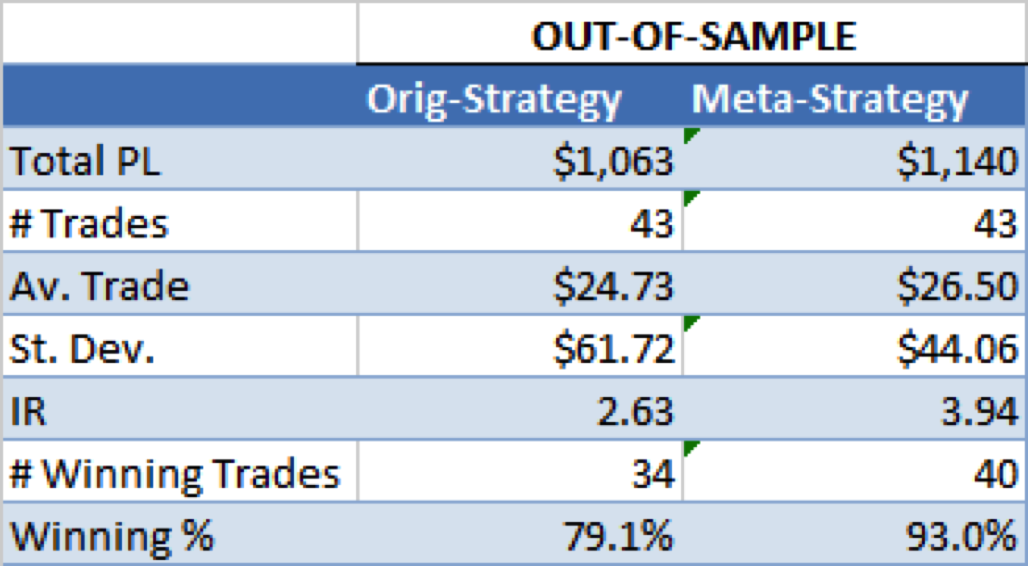

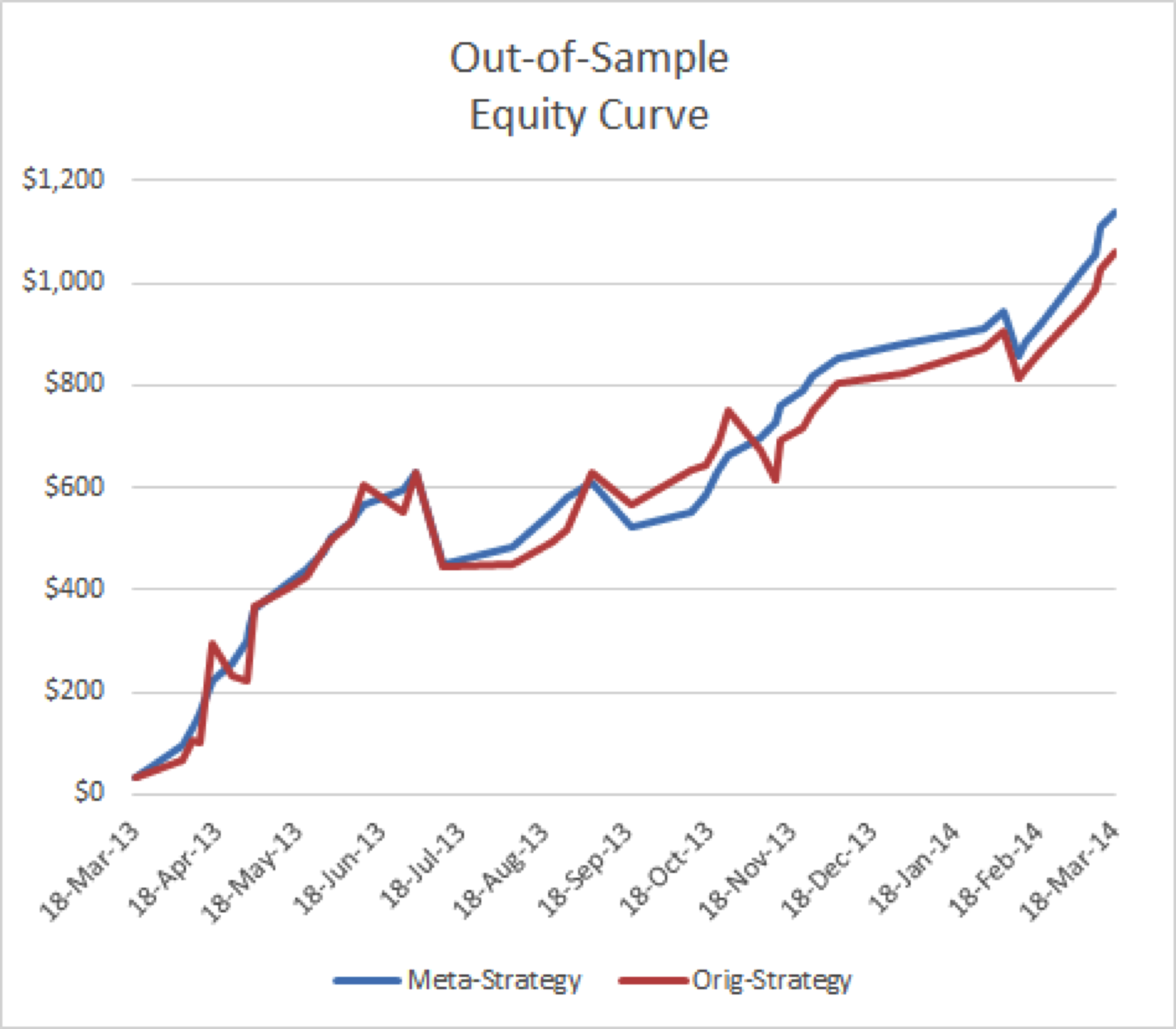

2. Strategy Performance

2.1 Overall Performance

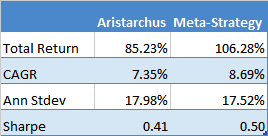

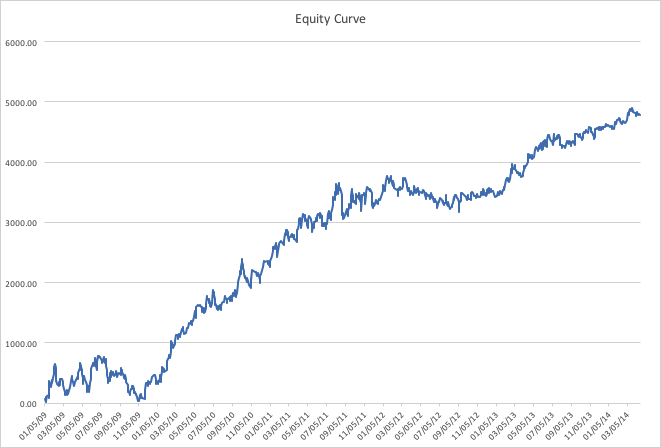

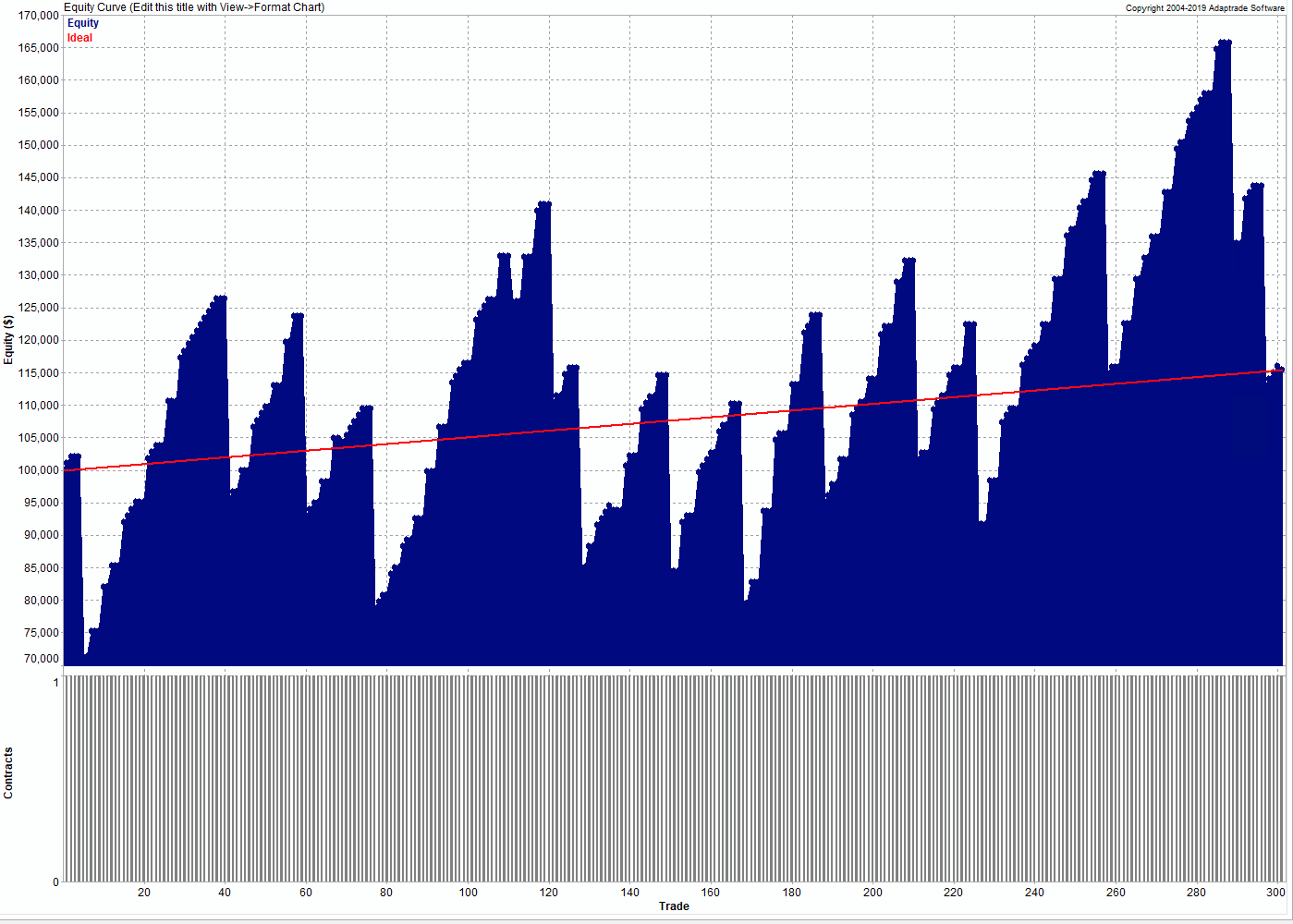

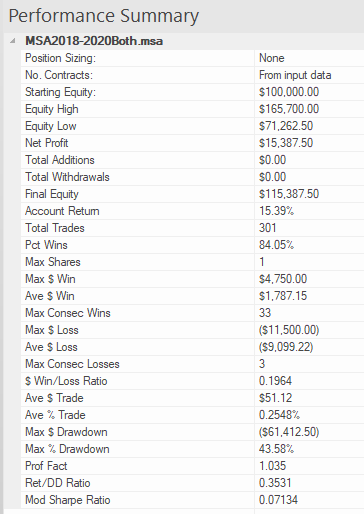

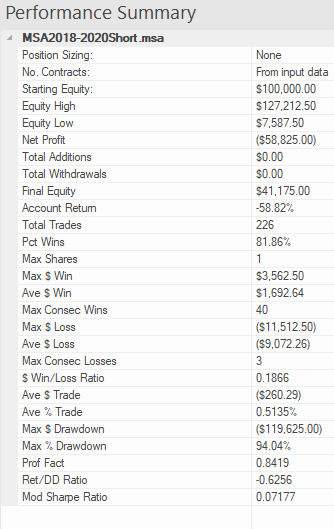

The overall performance of the strategy over the period from 2018 to 2020 is summarized in the chart of the strategy equity curve and table of performance statistics below.

These confirm that, while the win rate if very high (over 84%) there strategy experiences many significant drawdowns, including a drawdown of -$61,412.50 (-43.58%). The total return is of the order of 5% per year, the strategy profit factor is fractionally above 1 and the Sharpe Ratio is negligibly small. Many traders would consider the performance to be highly unattractive.

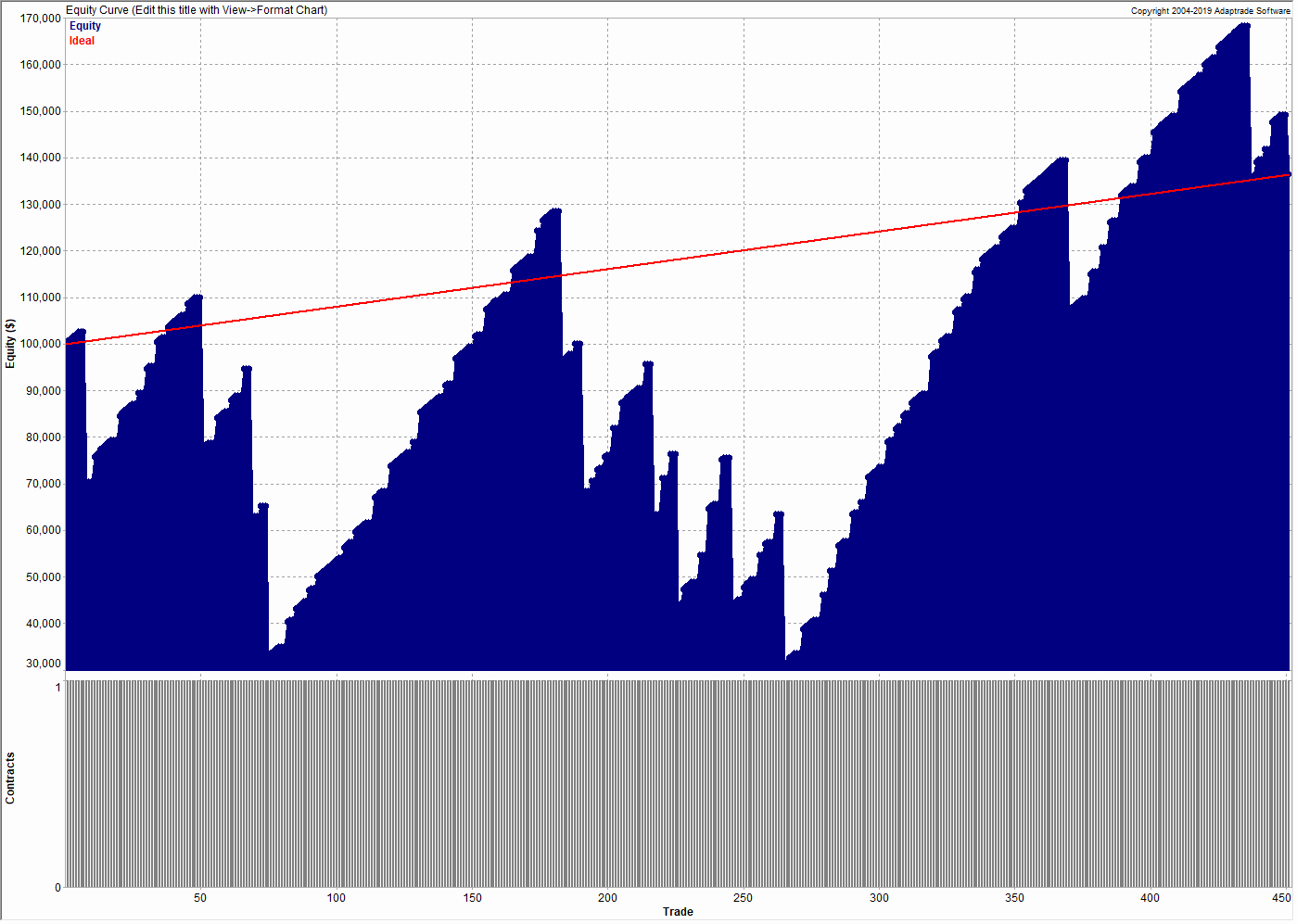

2.2 Long Trades

We break the strategy performance down into long and short trades, and consider them separately. On the long side, the strategy has been profitable, producing a gain of over 36% during the period 2018-2020. It also suffered catastrophic drawdown of over -$97,000 during that period:

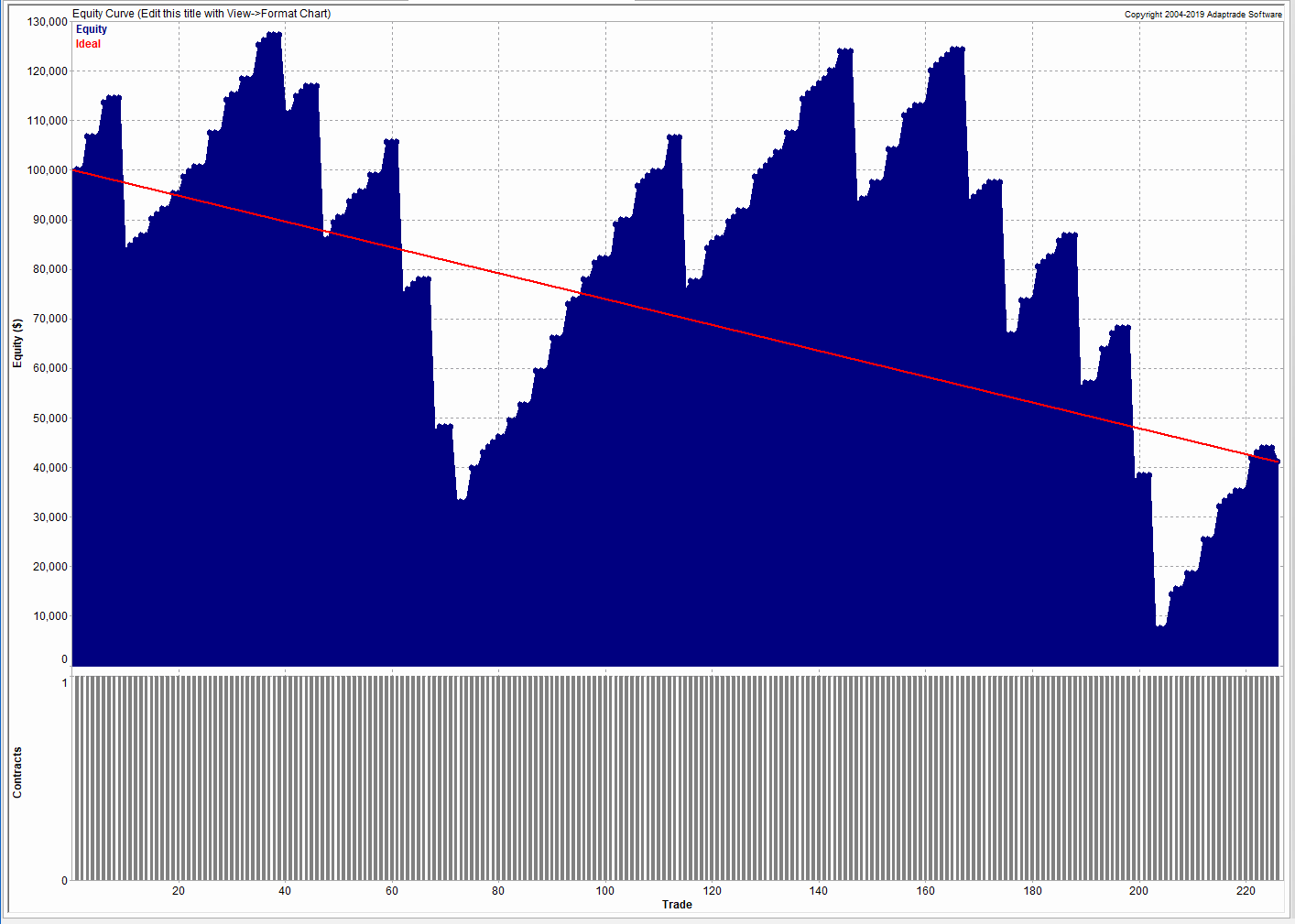

2.3 Short Trades

On the short side, the story is even worse, producing an overall loss of nearly -$59,000:

3. Improving Strategy Performance with a Meta-Strategy

We considered two possible methods to improve strategy performance. The first method attempts to apply technical indicators and other data series to improve trading performance. Here we evaluated price series such as the VIX index and a wide selection of technical indicators, including RSI, ADX, Moving Averages, MACD, ATR and others. However, any improvement in strategy performance proved to be temporary in nature and highly variable, in many cases amplifying the problems with the strategy performance rather than improving them.

The second approach proved much more effective, however. In this method we create a meta-strategy which effectively “trades the strategy”, turning it on and off depending on its recent performance. The meta-strategy consists of a set of rules that determines whether or not to continue trading the strategy after a series of wins or losses. In some cases the meta-strategy may increase the trade size for a sequence of trades, at times when it considers the conditions for the underlying strategy to be favorable.

The result of applying the meta-strategy are described in the following sections.

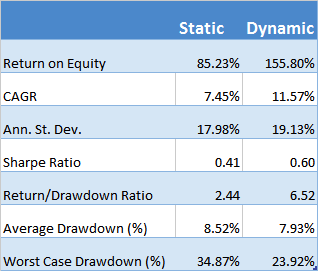

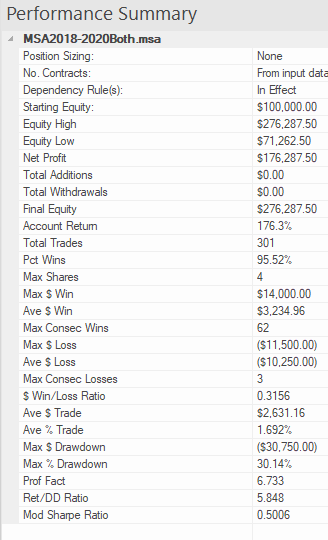

3.1 Long & Short Strategies with Meta-Strategy Overlay

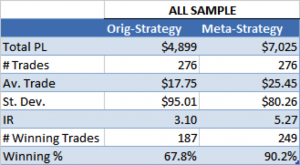

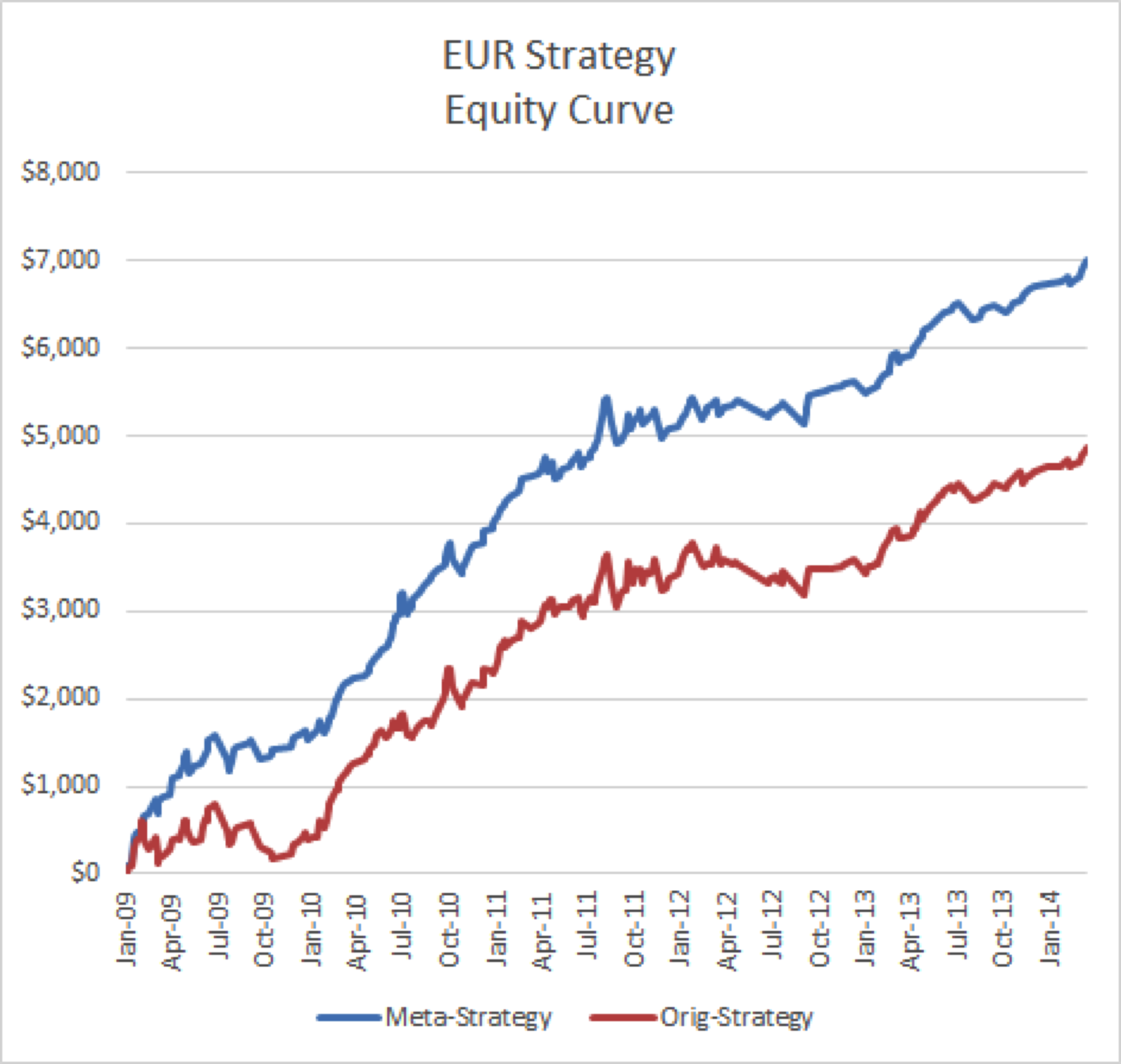

The performance of the long/short strategies combined with the meta-strategy overlay are set out in the chart and table below.

The overall improvements can be summarized as follows:

- Net profit increases from $15,387 to $176,287

- Account return rises from 15% to 176%

- Percentage win rate rises from 84% to 95%

- Profit factor increases from 1.0 to 6.7

- Average trade rises from $51 to $2,631

- Max $ Drawdown falls from -$61,412 to -$30,750

- Return/Max Drawdown ratio rises from 0.35 to 5.85

- The modified Sharpe ratio increases from 0.07 to 0.5

Taken together, these are dramatic improvements to every important aspect of strategy performance.

There are two key rules in the meta-strategy, applicable to winning and losing trades:

Rule for winning trades:

After 3 wins in a row, skip the next trade.

Rule for losing trades:

After 3 losses in a row, add 1 contract until the first win. Subtract 1 contract after each win until the next loss, or back to 1 contract.

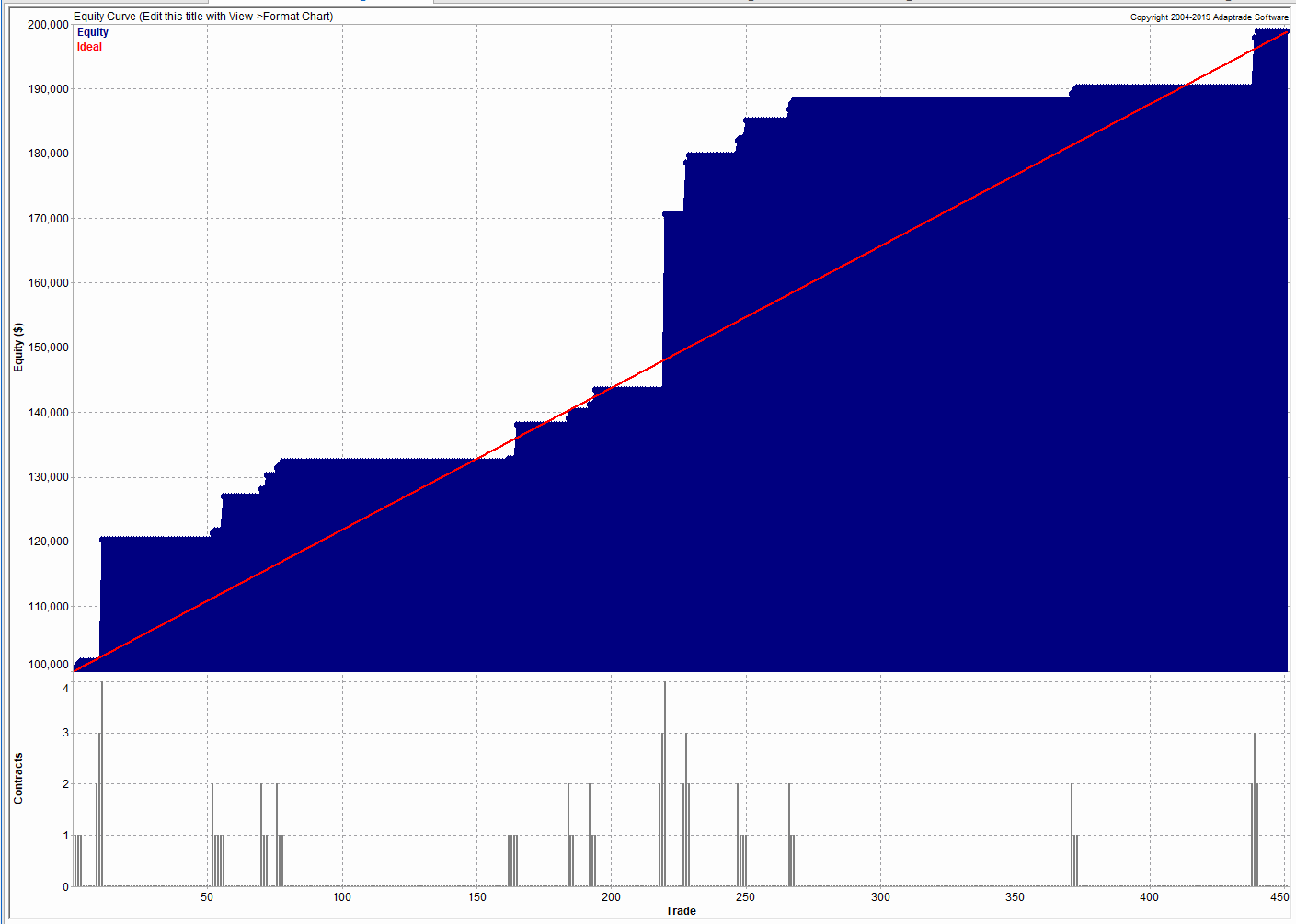

3.2 Long Trades with Meta-Strategy

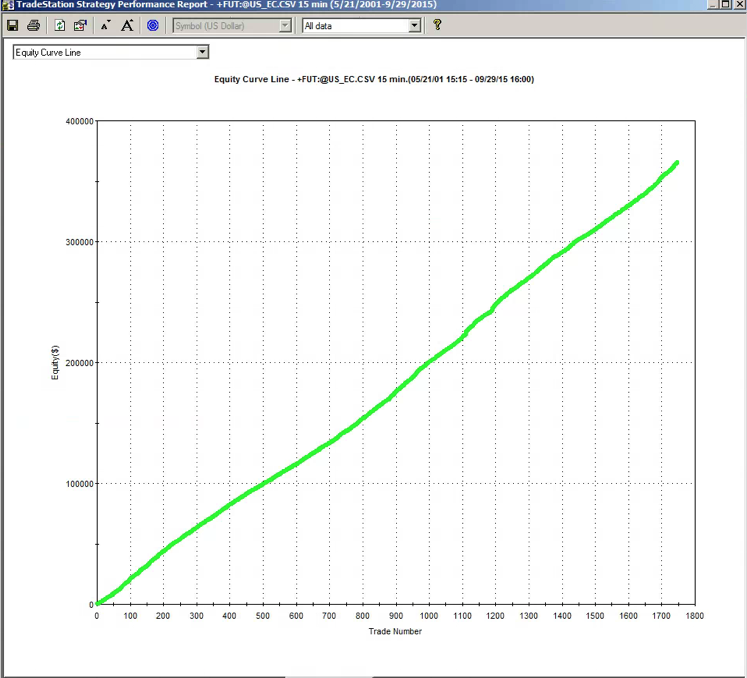

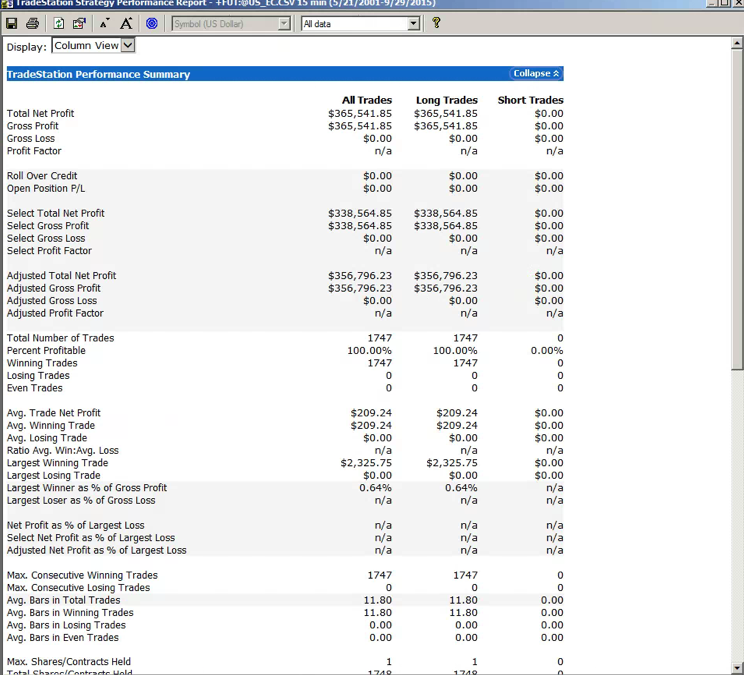

The meta-strategy rules produce significant improvements in the performance of both the long and short components of the strategy. On the long side the percentage win rate is increased to 100% and the max % drawdown is reduced to 0%:

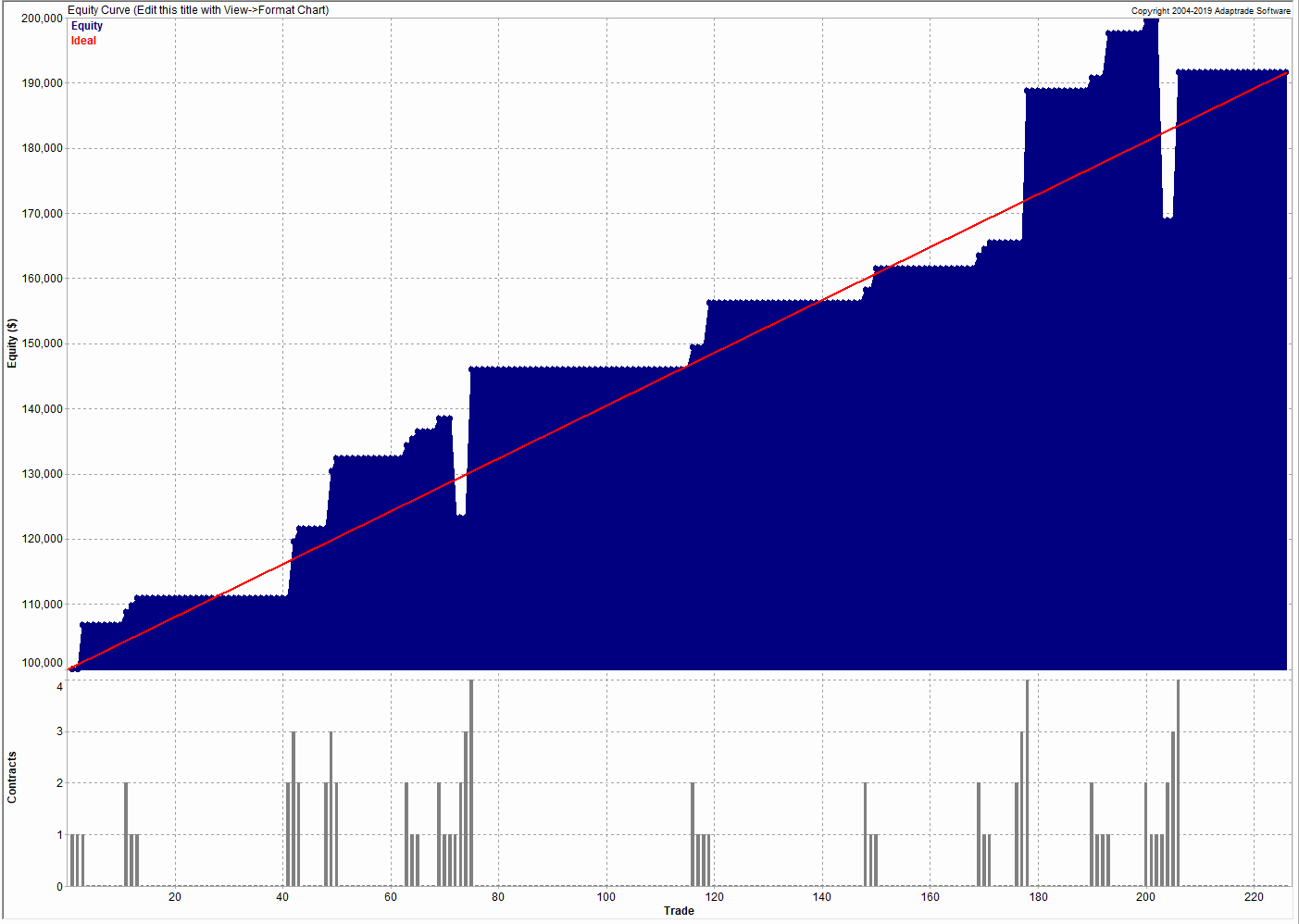

3.3 Short Trades with Meta-Strategy

Improvements to the strategy on the short side are even more significant, transforming a loss of -$59,000 into a profit of $91,600:

4. Conclusion

A meta-strategy is a simple, yet powerful technique that can transform the performance of an underlying strategy. The rules are often simple, although they can be challenging to implement. Meta strategies can be applied to almost any underlying strategy, whether in futures, equities, or forex. Worthwhile improvements in strategy performance are often achievable, although not often as spectacular as in this case.

If any reader is interested in designing a meta-strategy for their own use, please get in contact.