There are a plethora of seasonal anomalies documented in academic research. For equities these include the Halloween effect (“Sell in May”), January effect, turn-of-the-month effect, weekend effect and holiday effect. For example, Bouman and Jacobsen (2002) and Jacobsen and Visaltanachoti (2009) provide empirical evidence on the Halloween effect, Haug and Hirschey (2006) on the January effect, Lakonishok and Smidt (1988) on the turn-of-the-month (TOM) effect, Cross (1973) on the weekend effect, and Ariel (1990) on the holiday effect.

An excellent paper entitled An Anatomy of Calendar Effects in the Journal of Asset Management (13(4), 2012, pp. 271-286) by Laurens Swinkels of Erasmus University Rotterdam and Pim van Vliet of Robeco Asset Management gives a very good account of the various phenomena and their relative importance. Using daily returns data on the US value-weighted equity market over the period from July 1963 to December 2008, the researchers find that Halloween and turn-of-the-month (TOM) are the strongest effects, fully diminishing the other three effects to zero. The equity premium over the sample 1963-2008 is 7.2% if there is a Halloween or TOM effect, and -2.8% in all other cases. These findings are robust with respect to transactions costs, across different samples, market segments, and international stock markets. Their empirical research narrows down the number of calendar effects from five to two, leading to a more powerful and puzzling summary of seasonal effects.

The two principal effects are illustrated here with reference to daily returns in the S&P 500 Index, using data from 1980-2016.

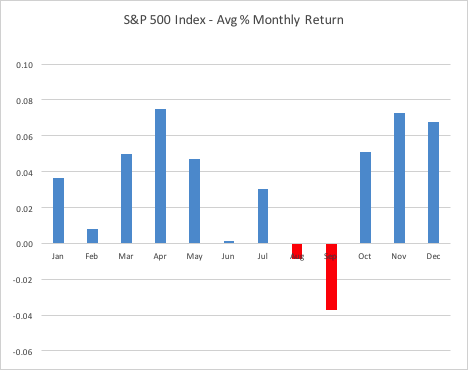

Halloween Effect

The Halloween effect refers to the tendency of markets to perform better in the six month period from November to April, compared to the half year from May to October. In fact, for the S&P 500 index itself, performance during the months of May and October has historically been above the monthly average, as you can see in the chart below. According to this analysis, the period to avoid spans the four months from June to September, with September being the “cruelest month”, by far. Note that, between them, the months of November, December and April account for over 50% of the average annual return in the index since 1980.

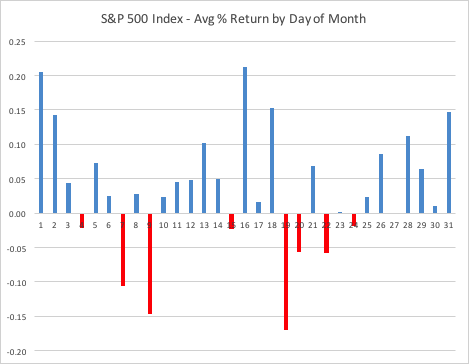

Turn-of-the-Month Effect

The TOM effect refers to the finding that above average returns tend to occur on the last trading day of the month and (up to) the first four trading days of the new calendar month. For the S&P 500 index the TOM effect spans a shorter period comprising the last trading day of the month and the first two trading days of the new month. It is worth noting also the anomalous positive returns arising on 16th – 18th of the month and negative returns around the 19th and 20th of the month. My speculative guess is that these mid-month effects arise from futures/option expiration.

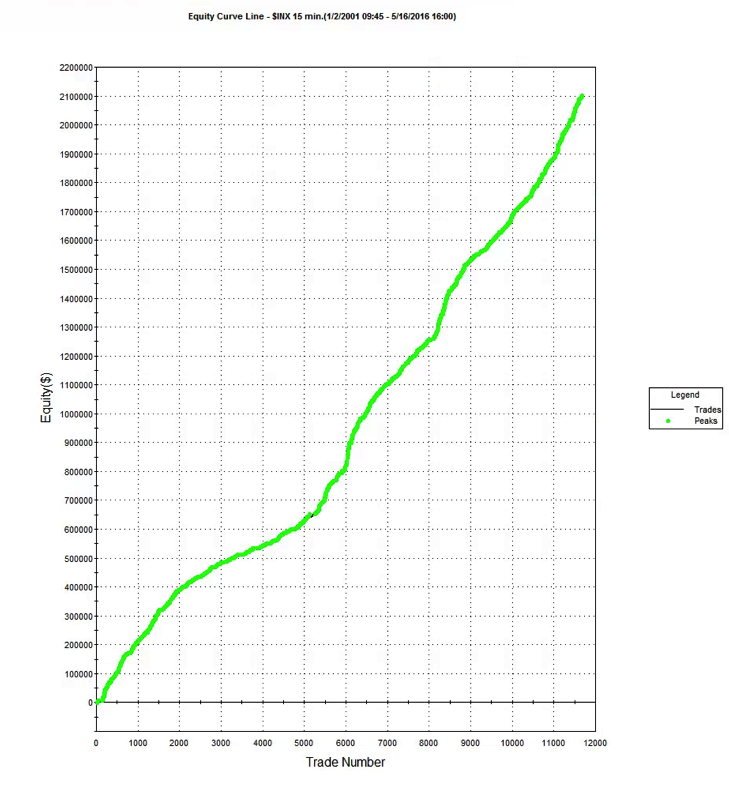

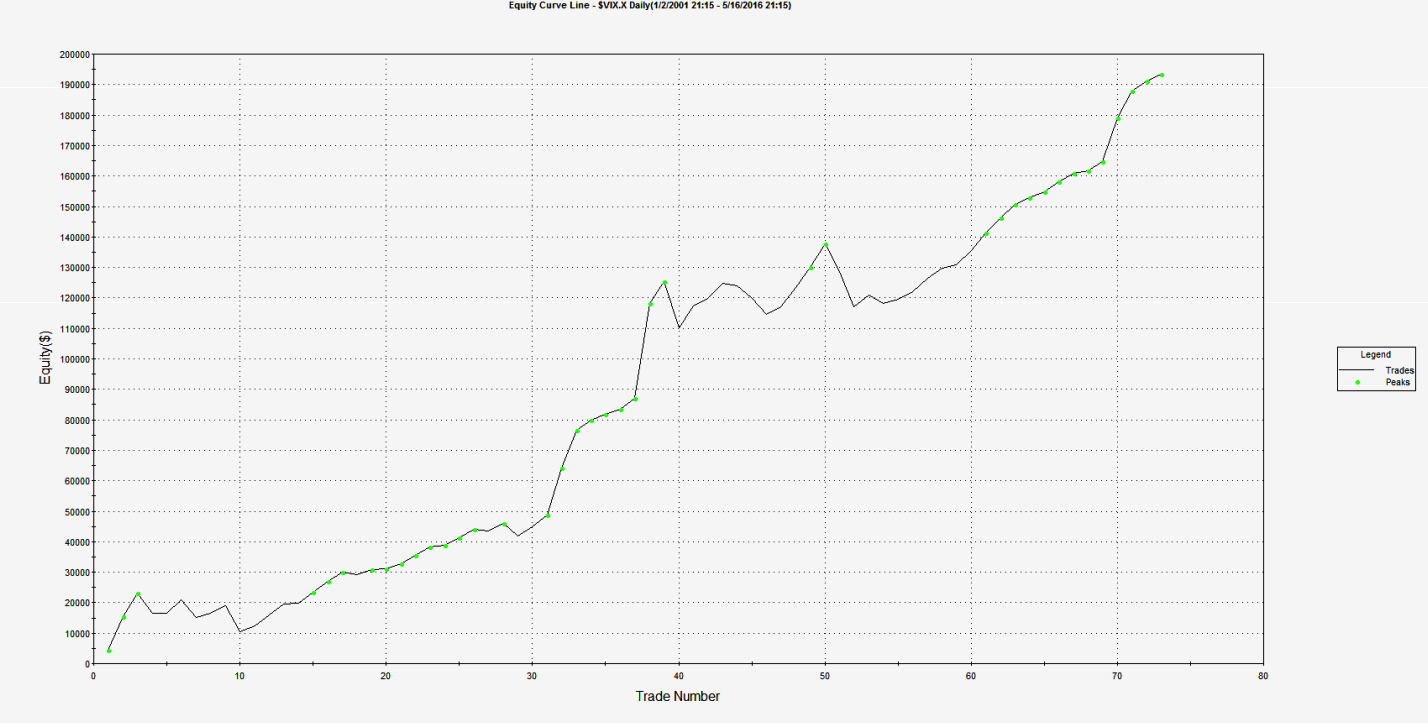

Seasonal Tactical Allocation

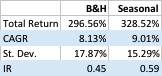

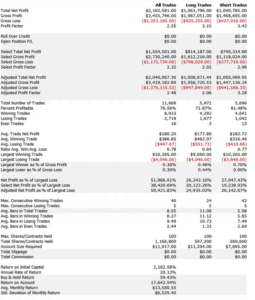

Let’s assume we allocate to equities (in the form of the S&P 500 Index) only during the period from October to May, or on the last or first two trading days of each month. How do the returns from that seasonal portfolio compare to the benchmark buy and hold portfolio? If we ignore transaction costs (and income from riskless Treasury investments when we are out of the market), the seasonal portfolio outperforms the buy and hold benchmark over the 36 year period since 1980 by around 88bp per annum (continuously compounded), and with an annual volatility that is 258bp lower. The outperformance of the seasonal portfolio becomes particularly noticeable after the 2000/2001 crash.

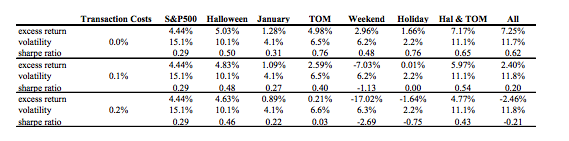

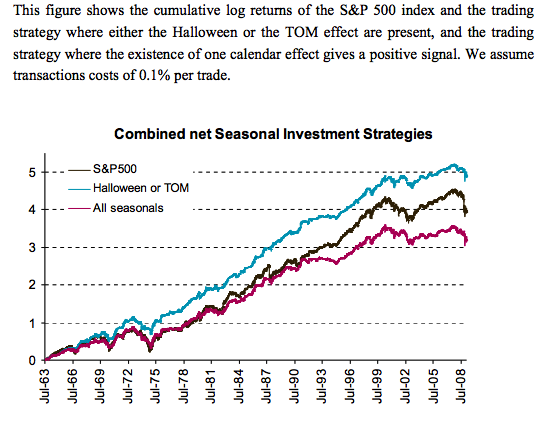

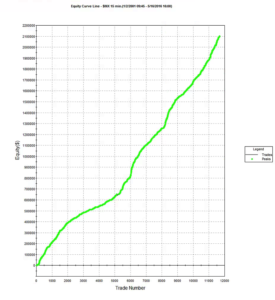

A much more rigorous analysis of the performance characteristics of the seasonal portfolio is given in the research paper, taking account of transaction costs, with summary results as follows:

Conclusion

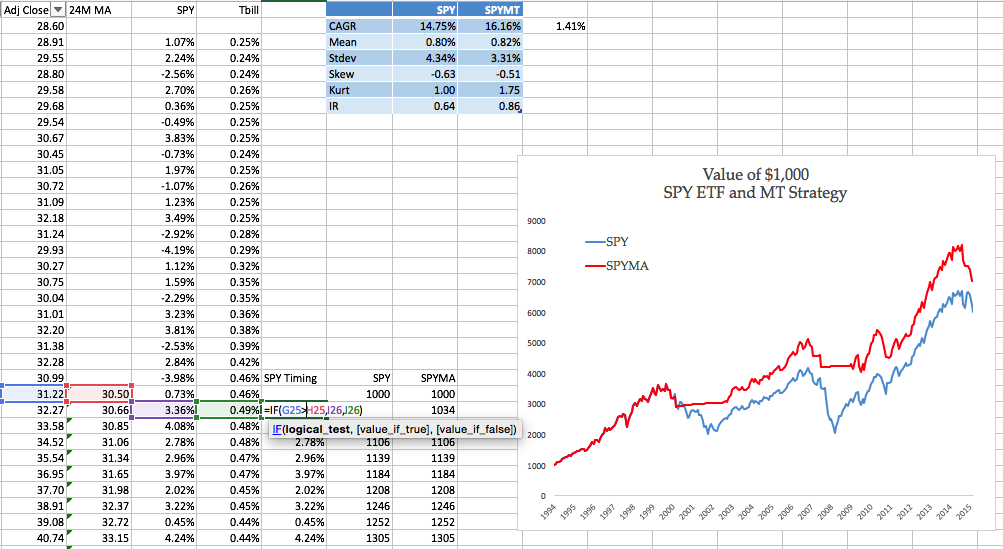

There is a sizable body of credible academic research demonstrating the importance of calendar effects and this paper suggests that investors’ focus should be on the Halloween and TOM effects in particular. A tactical allocation program that increases the allocation to equities towards the end of the month and first few trading days of the new month, and during the November to April calendar months is likely to significantly outperform a buy-and-hold portfolio, according to these findings.

There remain unaccounted-for seasonal effects in the mid-section of the month that may arise from the expiration of futures and option contracts. These are worthy of further investigation.

{kind=link}

{kind=link}

{kind=link}